In the last concall management guided that they will able save ~15cr of fixed expenses due to closure of Italy plant. This benefit will start accruing starting from FY26

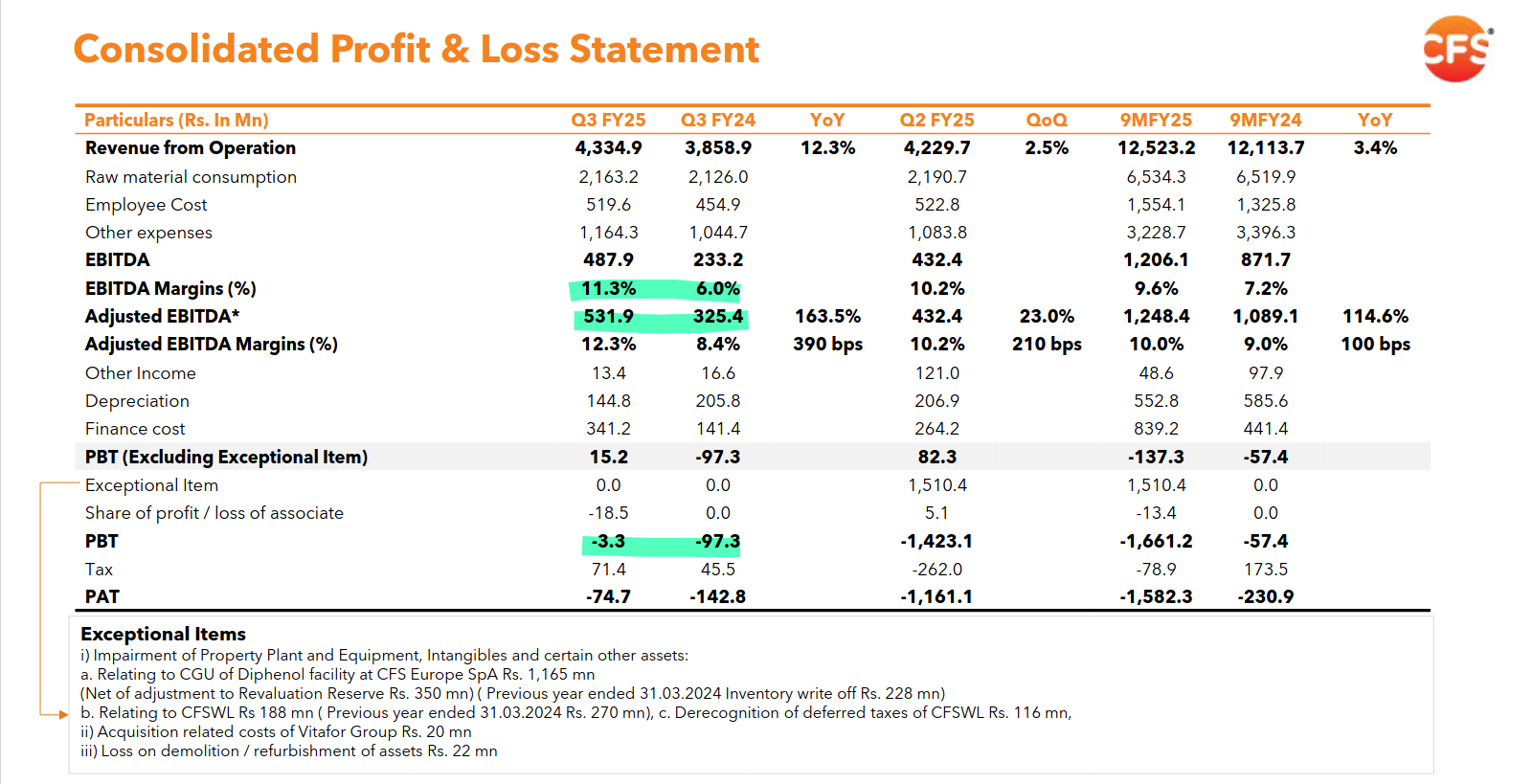

Since there is no more write off expected (as per the management in the last concall) , based on current steady state, Q2-FY25 clocked 10% margins with operating profits of 43cr, in FY26, we can expect ~228 Cr of operating profits ( 43cr x 4 + 14cr x 4). As blends commands better margins with increased scale and funds infusion of 225cr might help the company to improve working capital which might help in improving over all return ratios.

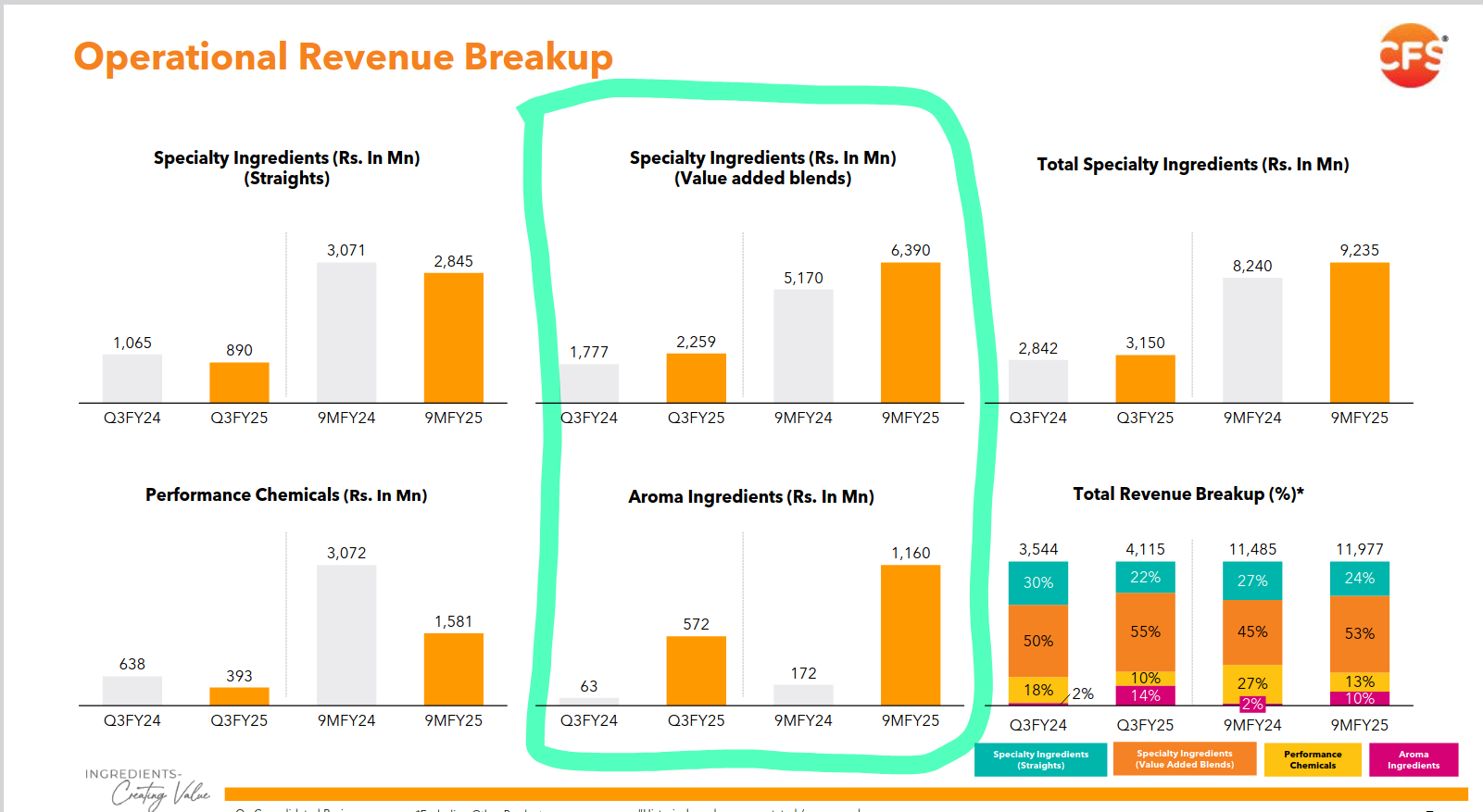

Good set of numbers from Camlin. As management commentary Blends and Aroma business doing well. Venillin prices are firming up (from Management commentary in concall).

With the losses from discontinuation of business of around ~17cr going away significantly from Q2FY26 and increased in capacity utilization, hope margins will improve going forward.

The chinese competitors sell vanillin at $ 10 / kg (excluding tariffs). With the BCD, CVD and ADD (total amounting to greater than 200% tax), the theoretical vanillin price in USA comes upto $ 30 / kg for the Chinese companies.

Basis the above, Camlin should be able to sell vanillin at atleast $ 20 / kg (Considering they want to continue to maintain customer relationships). This is excluding Trump tariffs which are not predictable.

Keep in mind that this is only in the USA, China can continue dumping in other countries thereby affecting Camlin’s sales there resulting on higher dependence on USA.

Any reason behind the stocks latest run up?

All I could find was that European Commission has imposed provisional 131% anti-dumping duties on vanillin imports from China, but can’t find any official source. Is this news legit?

Any reason for the company’s price action to be so erratic?

Considering the tailwind the business has, it’s quite extreme to see the price been in continous lower circuits.

Is there something that will come out or market doesnt know?

Price went up assuming tariff on China on Venillin in US and China will be a huge tailwind. Looks like it has not playing out as expected until now. So price is mirroring performance.