IT service/outsourcing company with focus on Cloud, Machine Learning, Big Data and Analytics.

Aashish kalra, an equity investor took over the company formally on the 1 January 2015. He has provided a two-year business plan to achieve USD 2 Million in revenue/month by March 2017.

It has got three divisions apart from main core service division:

1. Cambridge Innovations:

CTE launched Cambridge Innovations in Q3FY16 to partner with the most innovative new U.S. startups leveraging big data, cloud & IoT for transformative disruption. Provides capital and resources to reduce technology risk. It is targeting to invest in 50 start-ups by 2019. Accounts for approx. 10% of our consolidated revenues. www.c7e.io

2. Cambridge BizServe

Launched Cambridge BizServe in Q4FY16, a vertical focused to effectively manage business processes and provide business insights through analytics to our clients. Cambridge BizServe is a fast-growing vertical for CTE and accounts for approx. 5% of our consolidated revenues. http://www.c7b.co

3. Cambridge Datascience

To Launch Cambridge DataScience (CD) in Q3FY17 to assist CXOs make decisions by drawing substantial strengths in AI/Machine Learning, insights and data analytics. Focus will be to build infrastructure and team for CD over the next six months. Hired Dr. Rajan Lukose as Chief Scientist, CD. He has over 25 patents registered in his name and has several laurels including an IBM award in Computational Finance. He has over 20 publications like ‘Learning User Purchase Intent From User-Centric Data’, ‘Local Search in Unstructured Networks’, ‘An Economic Approach to Hard Computational Problems’.

Cambridge Innovations:

At present, CI has invested in the below 11 start-ups

http://enerallies.com/ - Cambridge Innovations announces focus on IoT with EnerAllies as its first investment

http://www.roadzen.in/

a. http://www.strandd.in/ - StrandD is India’s largest on-demand roadside assistance service. We’re available 24/7, pan-India and you only pay-per-use.

b. InspectD App - India and China have a combined market of 400 million vehicles. We are the first technology enabled service to provide inspection and assign warranty to these cars.

http://www.anthillventures.com/

a. CI has also invested in Hyderabad-based startup accelerator, Anthill Ventures. Anthill in-turn invests in the Indian startup community, with prominent Indian incubator 91Springboard one of the companies under their wing.

Company is focused only on niche cloud and big data where opportunity size is very big ~ $300 billion by 2020. Even a very small pie can be a big potential for CTE. Company with market cap of just ~Rs.200 Crores and revenue of 70 crores/year, has lots of potential to grow quickly.

Clear business plan. Once CTE achieves minimum scale of USD 2 Million in revenue/month by March 2017, the company will announce its growth plans for Mar ‘19.

It is targeting to invest in 50 start-ups by 2019 through Cambridge Innovations. Even with 5% success rate, payoffs can be big.

Reaching the level Oracle Platinum Partner shows that company has executed many successful Oracle projects.

Ashish Kalra is a successful equity investor in technology, infrastructure, real estate, energy, logistics and hospitality. Prior to Cambridge Technology Enterprises, he was the Founder and Managing Director of Trikona Capital.

Other notable investors:

a. Raymond J Lane still holds 2.55% of the company. He was former President and Chief Operating Officer of Oracle. Currently serves as Partner Emeritus at Kleiner Perkins Caufield & Byers. http://www.kpcb.com/partner/ray-lane I’m not able to find out at when Ray Lane has entered Cambridge. .

b. Kanchan Sunil Singhania has entered in FY16 and holds 1.45%

Promoter (46.91%) and other major public shareholders (28.55%) constitute 75% of shareholding.

Negatives:

Absolutely no moat. It is yet another IT service company.

No financial details on startup investments. So very difficult to gauge the ROI.

No dividends yet as I believe profits are used for further growth like CI investments in startups.

Currently stock is in hands of operators and huge price fluctuations happening. Exchanges have put 2% circuit limit.

Uncertainty in US H1B visa process. May or may not impact this company.

Disclosure: Invested. This is not a recommendation. Please do your own research before you buy/sell any stock.

Congrats for your decently lengthy post (most of which can be obtained by google search). You have made sure that your post/thread wont be killed because you have nicely copy-pasted the required info to it

I like and is invested in CTE. I like the management’s walking the talk and superb growth (Unlike the crazy management Talk of Kellton).

The risk being risk associated with their PE type investments. Also because of 2% circuit limit, it runs like a caged train, you wont get entry and exit at your wished price/time. I will also keep a watch on their receivables and their next growth forecast.

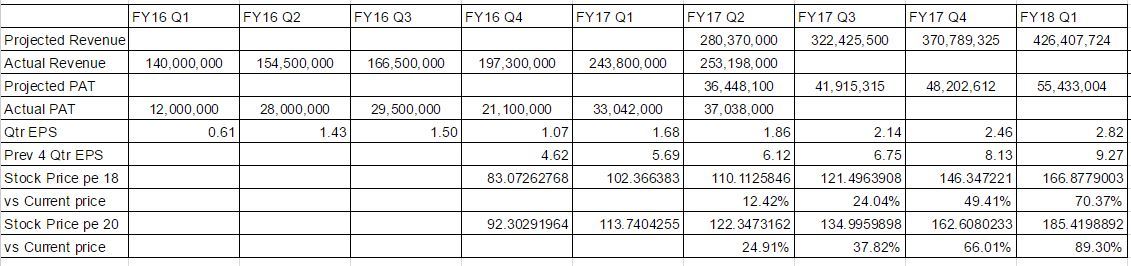

Ha ha …learning from your Kellton post. Below is the simple projection considering if they meet their promise of $2m/month revenue. If they walk-the-talk and continue their amazing growth numbers + if 2019 target business plan is good, then this may get re-rated.

I was interested in understanding the reason for continuous lower circuits in stock but could not find any strong information. I did a little scuttlebutt and hence posting my findings.

The stock has gone from Rs. 3 in February 2014 to 145 in October 2015. Its currently trading at 97. It is most of the time either in lower or upper circuits. The real change has happened after Aashish Kalra took over this company. So it becomes important to understand Kalra’s vision for this company.

He is a Venture Capitalist and been investing in technology, infrastructure, real estate, energy, logistics and hospitality. I found one case filed against him from ARC Capital. Though the case could not prove charges against him but one can still go through the background section of this webpage. http://www.leagle.com/decision/In%20NYCO%2020130626653/ARC%20CAPITAL,%20LLC%20v.%20KALRA

What is his vision for the company?

As far as I could understand he wants to use the money generated from cloud and big data division to invest in startups, preferably US.

Based on the idea that big data is a transformational use of technology, CI looks for companies that have an innovative idea, and need assistance with the marketing and sales, financing, and hiring tech teams. Partnering with a company means CI will provide up to 25% of seed capital, a two-year technology plan and the product development team to execute it.

If the company is in starting stages it makes it easier to bring it to India to build and then scale it globally – the path CI has taken with Pittsburgh-launched roadside assistance provider RoadZen. Bringing them to India to start up in a market that doesn’t have a functional road assistance service means was geared towards giving them a launchpad to the rest of the world.

Source: http://www.forbes.com/sites/abehal/2015/12/29/big-datas-cambridge-technology-enterprises-creates-a-new-kind-of-india-accelerator/#5b30a4542c0f

So, the ideal metric to judge this company should be the past track record of Ashish Kalra, since he is venture capitalist for more than a decade. Like how many successful companies he has mentored? What were the relationships with management? Views of different companies on working with him?

In short term, the company will keep on increasing its sales and profits and can reward shareholders handsomely but in the long term, his vision to foray into the startup space will be key to the future plans. He has also affirmed his commitment to invest in startup space in one of his interviews on Youtube. He also mentioned that he never liked the idea of working for a big organization.

Cambridge Technology Enterprises, a leading IT services leader focused on big data and cloud convergence, has posted 86 per cent growth in net profit during the third quarter of 2016-17, ended on December 31.

The net profit in Q3 was Rs 5.49 crore as against Rs 2.95 million during the same period last fiscal.

The company, which announced its results on Tuesday, said its revenues increased by 54 per cent.

The revenue during the quarter was Rs 25.31 crore against Rs 16.65 crore during the corresponding period of 2015-16.

EBITDA at Rs 5.56 crore grew 139 per cent year-on-year. The Earning Per Share (EPS) also increased by 86 percent.

Couple of fine print notes in the result presentation

The Hon’ble High Court of Judicature at Hyderabad has approved the Scheme of Reduction of Capital and a certified copy of Order dated 5th October, 2016 has been received by the Company. The Company continued to provide amortization of Goodwill for the Financial Year 2015-16 and for the quarter ended 30th June, 2016 amounting to INR 30.5 Mn pending to High Court Order. During the quarter, INR 15.2 Mn is reversed which is equivalent amortized to fifty percent of the amount amortized. This amount is an exceptional item in the above Flnancial Results. The balance amount of INR 15.2 Mn will be adjusted in the next quarter i.e., March 2017.

At CTE, we have less than two percent employees with H1B Visas and the change in US Visa policy has not impacted our business.

Revenue up 28% (25.2 cr vs 19.7 cr)

EBITDA up 27% (4.9 cr vs 3.8 cr)

Net Profit up 107% (4.4 cr vs 2.1 cr), There is an one time goodwill exceptional item of 91 lacs. Without that, it will be 64% up (3.5 cr vs 2.1 cr)

Management keeps shifting goal posts for the targets. In Q1 FY16 they had guided 2 million USD per MONTH at the end of FY 17. So ostensibly, FY18 should have had 48 million USD in revenue. Now this has been shifted to 2020. They have done USD 3.8 million in the entire quarter, which means 1.2-1.3 million USD per month.

Secondly, I am fairly concerned how they will raise 50 million USD (there is a proposal for this), which is almost double the market cap of the company as it stands today? No person will take equity worth 50 million because that essentially means buying the entire company at current prices. Placement at higher prices I think may be unlikely considering the share price cannot really go anywhere because of the circuit filters. A large equity stake would also trigger a host of requirements under the take over code (mandatory open offer, etc). Therefore, equity investment is unlikely and so is QIP.

That leaves FCCBs, which I think is very convenient for everyone involved till the retailers are left holding an empty plastic bag. Again, I do not understand what kind of independent entity will loan you 250% of your market capital and 20 times your annual profits. 350 crore of debt at even 5% interest rate means more than the net profit of the company. It is possible they will not raise 50 million, but maybe 10 million, but even that is 50% of the market cap of the company.

Also, the investor presentations are getting more and more useless. There is absolutely no information except two slides providing financial information. Other than this there are only fancy pictures and text. Till 1 quarter ago they were highlighting their start up investments in the US and naming the companies and further stating their goal of investing in 50 companies by Mar 2019. This has also completely disappeared - neither do the investments appear in the presentation nor are the targets relating thereto mentioned. Considering most companies rehash their presentations, why have they specifically chosen to exclude this?

I wonder if the start up investments ever happened at all and what happened to them now. Considering companies investing into start ups typically have shareholders agreements and access to all information, they do not even give a status update on their investments, which is quite strange.

There are dozens and dozens of red flags in this company, not least starting from the history of the promoters. Be careful.

Above link is the latest update on the business front of CTE. I could not relate this update to their previous businesses, they were doing and some new words Like Artificial Intelligence have been added to it. Please someone put lights on this new update can we also interpret that the Management is still struggling to find the business they wanted to be in???

Management may be slipping targets but I don’t see reason for the stock to correct so much given that they have given such great results even in such tough times of IT

Their last 4 quarters have been flat with nil growth both at revenue and operating profit level. Also, the only thing they seem to be doing is opening up subsidiaries in the last 4 quarters (with no results getting reflected in the financials).

And suddenly there is talk of $ 50 mn fund raise (for a company with < $30 mn market cap). Does anybody know the use of proceeds in this case (if at all the fund raise happens) ? -

a) In-Organic Growth: I recall Mr. Kalra mentioning in one of his interviews earlier that he doesn’t believe in growing in-organically.

b) WC: Also, doesn’t look like a working capital requirement for a company with ~$ 4 mn quarterly revenues.

c) Apart from this, if he intends to utilize the $ 50 mn for further investments in start-up, then technically the company is nothing but a VC fund which will not get valuations at multiples of earnings.

I have attended Cambridge Tech 2017 AGM, my notes are below

AGM started 15 min late as one director was struck in traffic

Ashish Kalra didnt attend. this is 3rd successive AGM that he didnt.

Investors were angry on why he didnt attend. Chairman couldnt give satisfactory

answer except saying he is travelling in Mumbai

If you see the directors on the dias, looks like they are all non-it guys and

dont inspire any confidense. They couldnt answer any question on business, technology.

Finally Chairman requested a corporate finance consultant who answered all questions.

One of the main resolutions is an enabling resolution to raise 50 mln usd as debt. Chairman didnt give any reason for raising funds inspite of angry investors refusing this resolution

When asked about 2 mln usd per month exit revenue by fy17 end, consultant replied in sept16 they revised that guidance to 100 cr inr which they met. Now they are not talking about this, they are sticking to 2020 vision statement of 50 mln usd

When asked why they need 50 mln usd debt when their 2020 target is only 50 mln usd, chairman couldnt amswer convinsingly , they kept saying its only a enabling resolution

They sold part of their stake in RoadZen at 250000 usd, their total investment in this startupis 1.3 mln usd, they sold 20% now.

Cambridge Investments has invested in total 12 start ups so far. they give investment and get some equity in that company and also revenue commtment for offering their services using AI, ML, BigData solutions

It takes 3-5 years to get any liquidy from these investments

regarding dividend, standard answer. need cash to grow. they told same thing last year also

regarding 2% circuit limit, the company cs met the stock exchanges twice. apart from this no more explanation is offered

they would give consol querterly numbers from next qtr

they have recently launched a new offering AI as a service and got one customer.

14.after the agm, one investor friend noted stock price came down to 60 and they came out with announcement on AI as a service and it went up to 90. again coming down as they didnt announce consol results, they gave only standalone results

my observations : The company needs to raise funds to fuel growth in their legacy services business which still accounts for 70% of the revenue. the new technologies AI, ML, BigData, Cloud Services account only 20%. raising funds, acquisions led growth cant be sustained. key is to survive this mode till their investments in start ups start yielding some liquidiy. it takes 3 years to get liquidy, till then they need funding. regarding 50 mln usd funding they are still working on modalities. my guess is they may raise debt in usa. Also there is no management bandwidth and board is very thin, this is completely one man show (Ashish Kalra) and he doesnt come to AGMs

Disc: Just bought 10 shares to attend agm. after the agm i removed it from my watch list, there are better stories to invest. i learnt my lessons in kellton tech, i dont want a repeat. also i mixed both official discussion on the dias discussions and off the dias discussions with the management. please do yr own dd before taking any decision.

Thanks a lot for sharing. Though I am not invested in this stock but the learning is great.

As all experienced - successful investors say- it is primarily the management that really matters - balance sheet, PE etc are all secondary.

One development in this company which could change the fortunes of the company. The development is in its USA subsidiary company - Cambridge Technology Financial Services Inc (CTFSI)

Background of team at CTFSI - https://www.ctfsi.com/about-us/#people

All the people from Goldman Sachs, Citi Bank, JP Morgan, MasterCard, Accenture, etc.