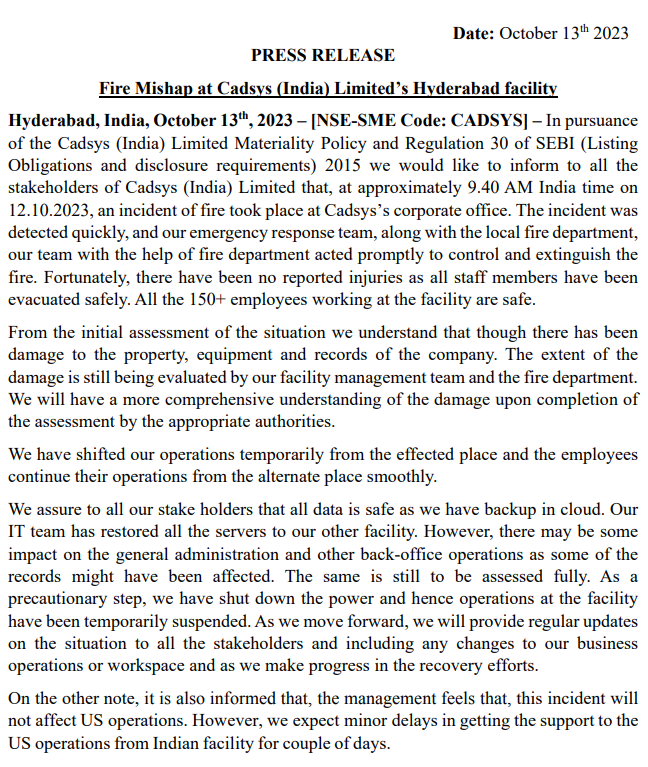

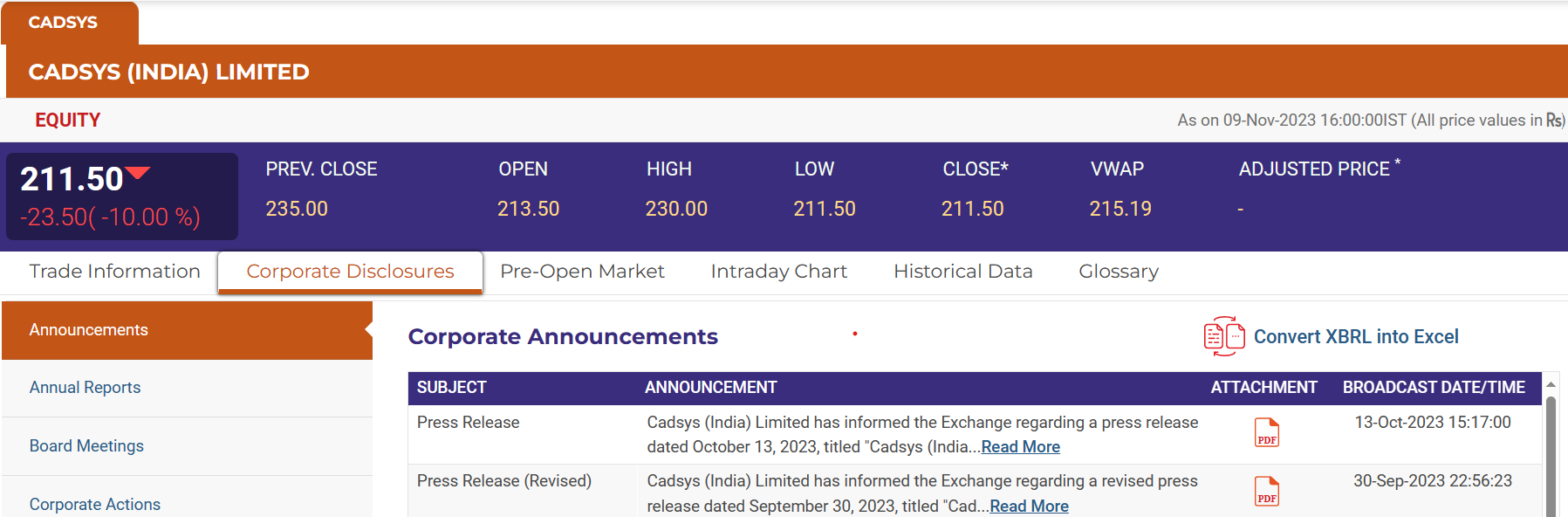

Cadsys (India) Limited.

Market Cap: 136 crores.

Incorporated in 1989, Cadsys Ltd undertakes GIS (Geographic information system) Mapping, engineering design, CAD services and project management support in the fields of telecommunications, gas, and electric and software development.

Company listed back in 2017 on NSE Emerge.

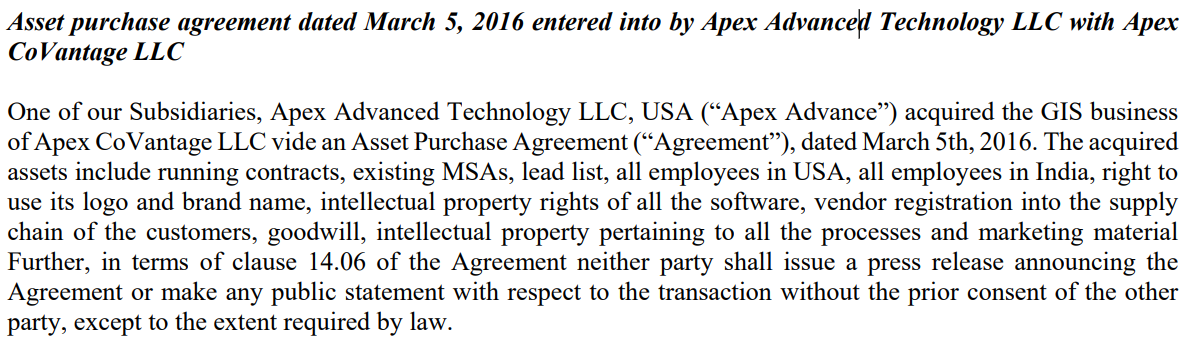

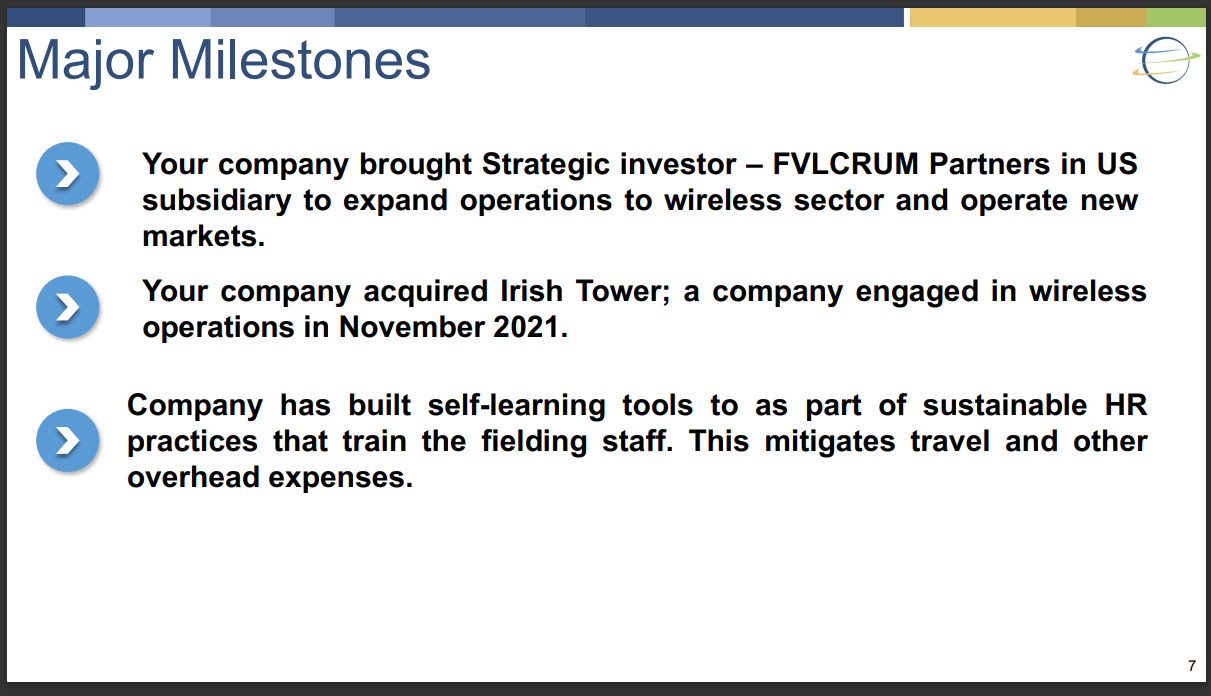

Company incorporated Apex Advanced Technology LLC in 2016 to cater the US market (100% Subsidiary). They acquired the GIS business of Apex CoVantage LLC and their total investment stood at US$19 million.

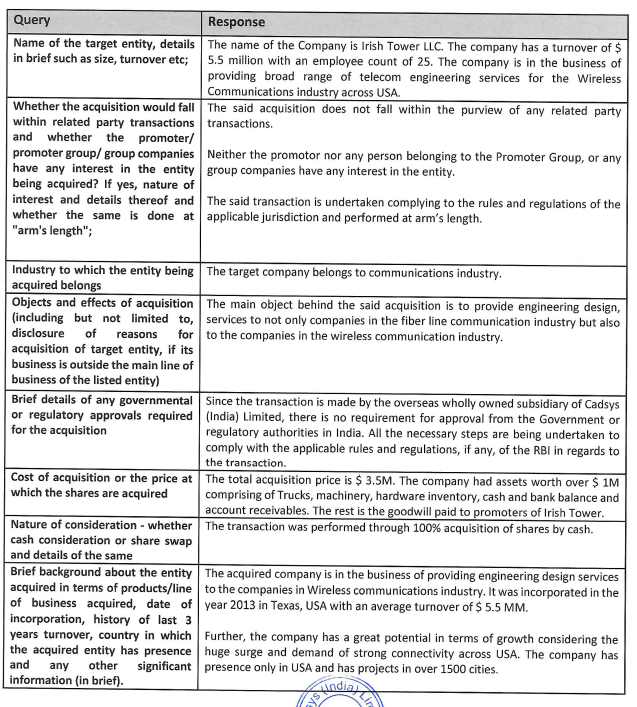

Subsequently in October 2021, they diluted their stake in Apex subsidiary to 64% by raising equity to FVLCRUM an US based PE fund, for 2.85 Million $. (Giving valuation to Apex of approx. 60 cr INR at $1=INR 75) With these funds they acquired IRISH Towers. (attached Screenshot)

.

On Friday’s board meeting, Cadsys further diluted their stake to 52%, raising almost 12% equity for Rs. 29.27 cr. giving Apex LLC the valuation of 250 cr INR. (60 cr to 250 cr valuation in 2 Years) to the same PE Fund.

On Consolidated level, Apex contributes to more than 95% of their revenues.

Investor Presentation 2022:

Investor Presentation 2023:

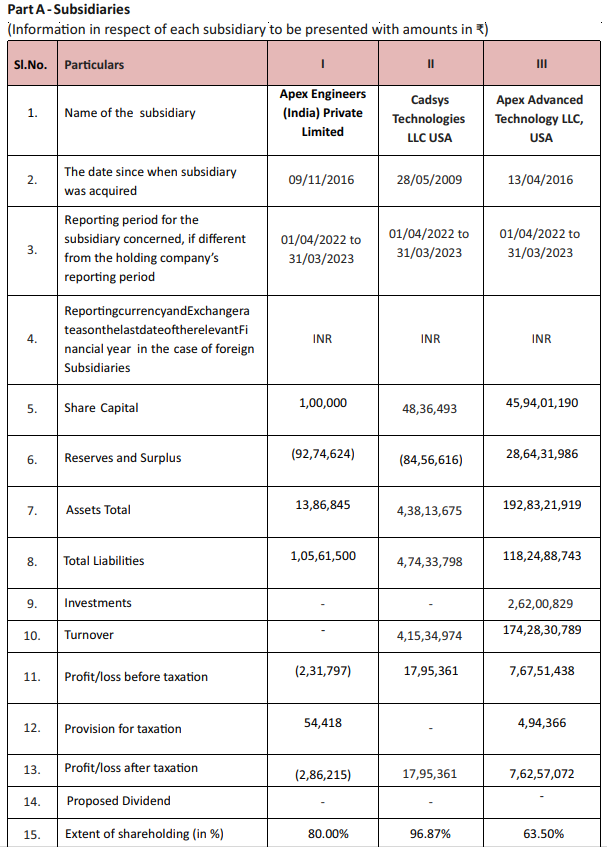

Company also have other Subsidiaries which do not impact consolidated level much.

Clientele:

Comcast, Bowker, AT&T, NBN co, Google Fiber, Verizon, Silcar, Century Link, BGE, Allegheny Power, Mid American Energy, Conective.

Other Points:

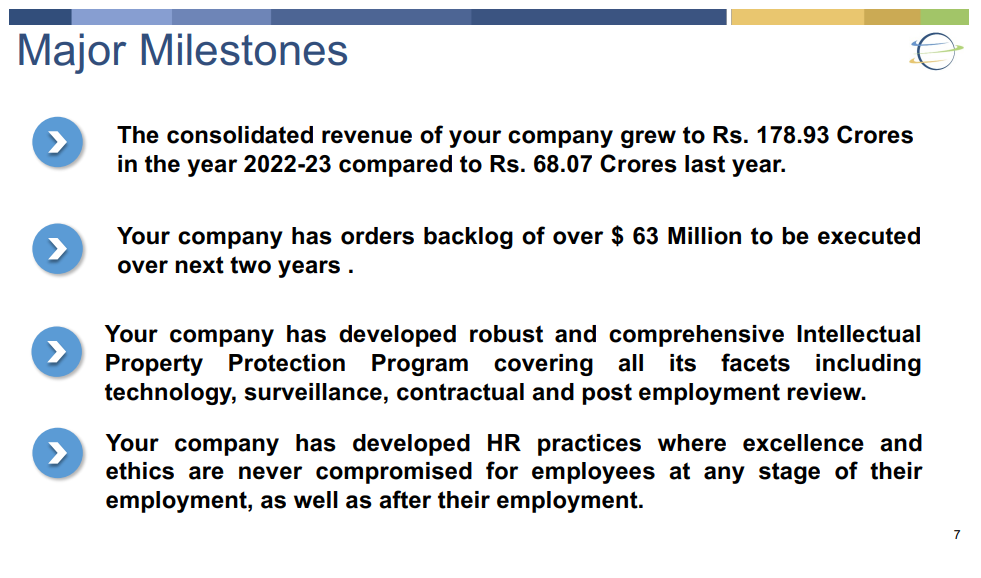

As per AR company has 63 Million $ orders still pending to complete.

Company started serving orders in its subsidiary a year ago and now has impressive sales with the order book expected to be completed within 2 years.

Promoters holding is 47.7%.

Company issued warrants at 50 Rs. per share and in a ratio where their current holding remains the same.

CRISIL Rating on standalone business upgraded from BB+/Stable to BB+/Positive for short term instruments.

Related Party includes remuneration/professional services of approx 2 cr in FY 23.

EPFO search for employees:

Apr 21 - 165

Apr 22 - 215

Apr 23 - 361

Aug 23 - 403

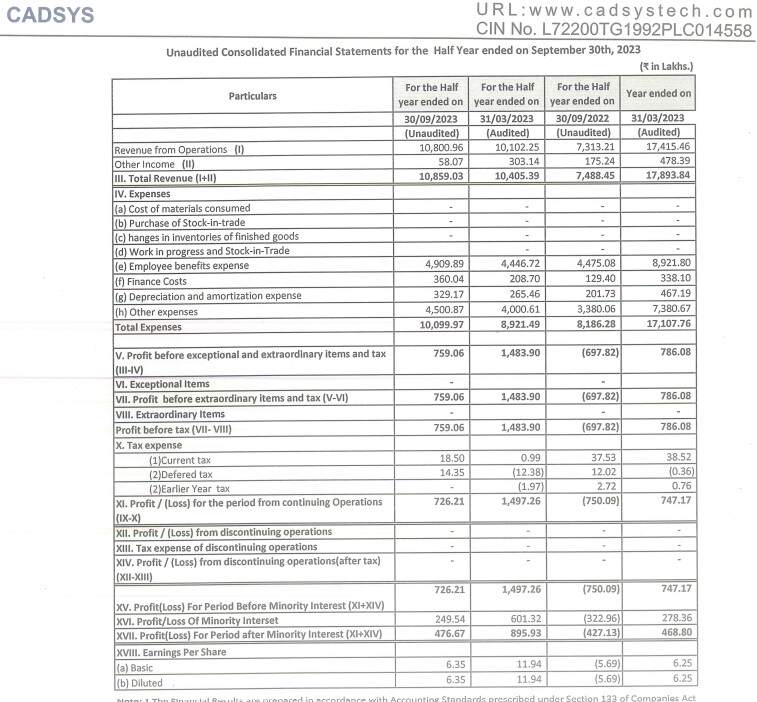

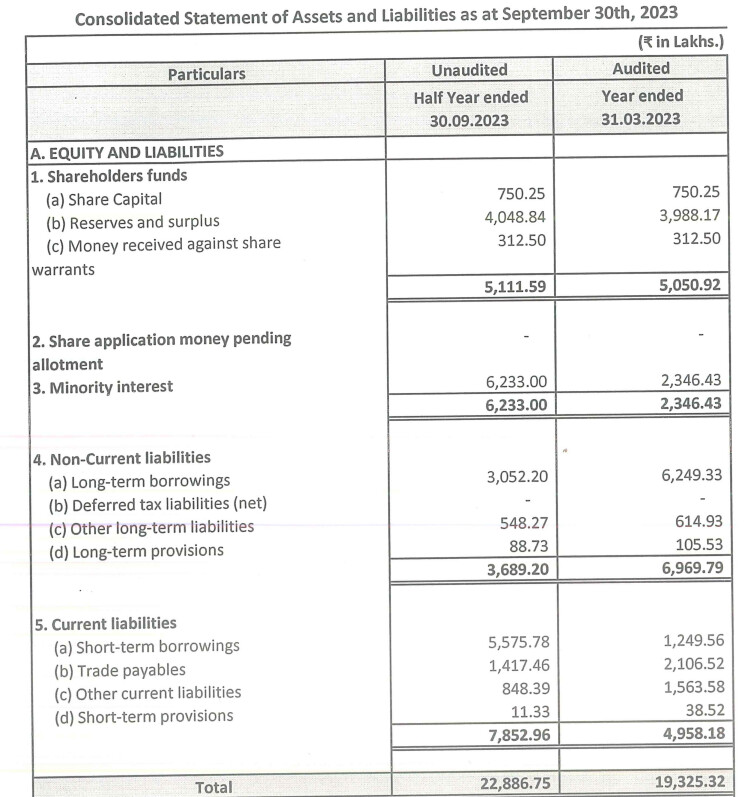

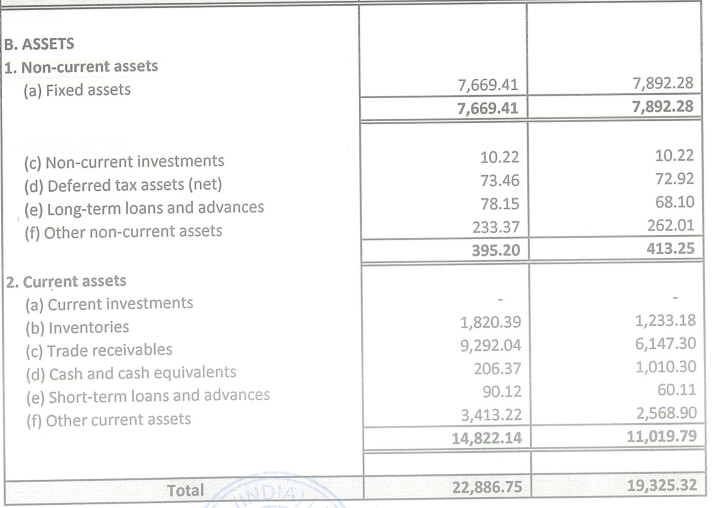

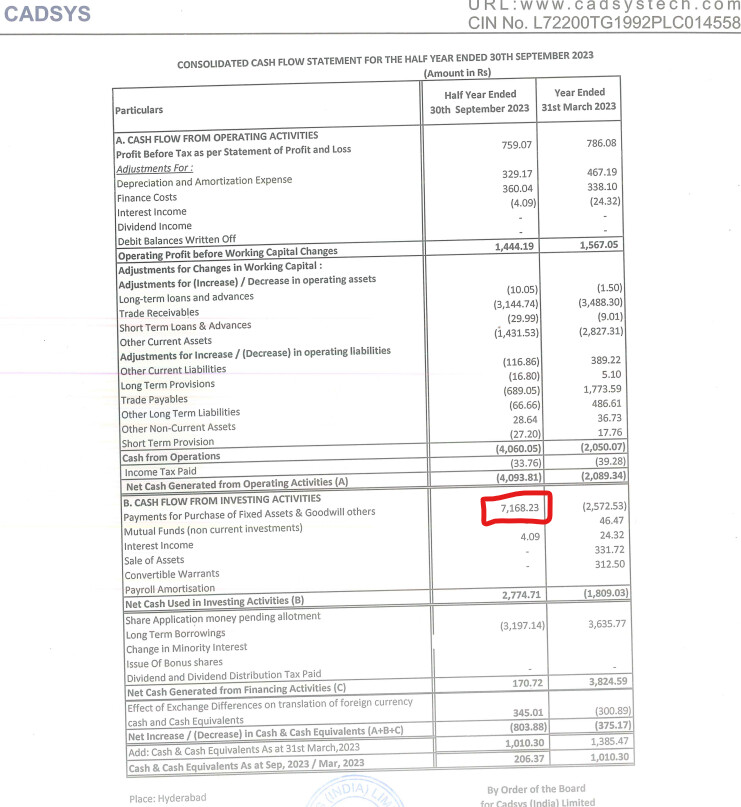

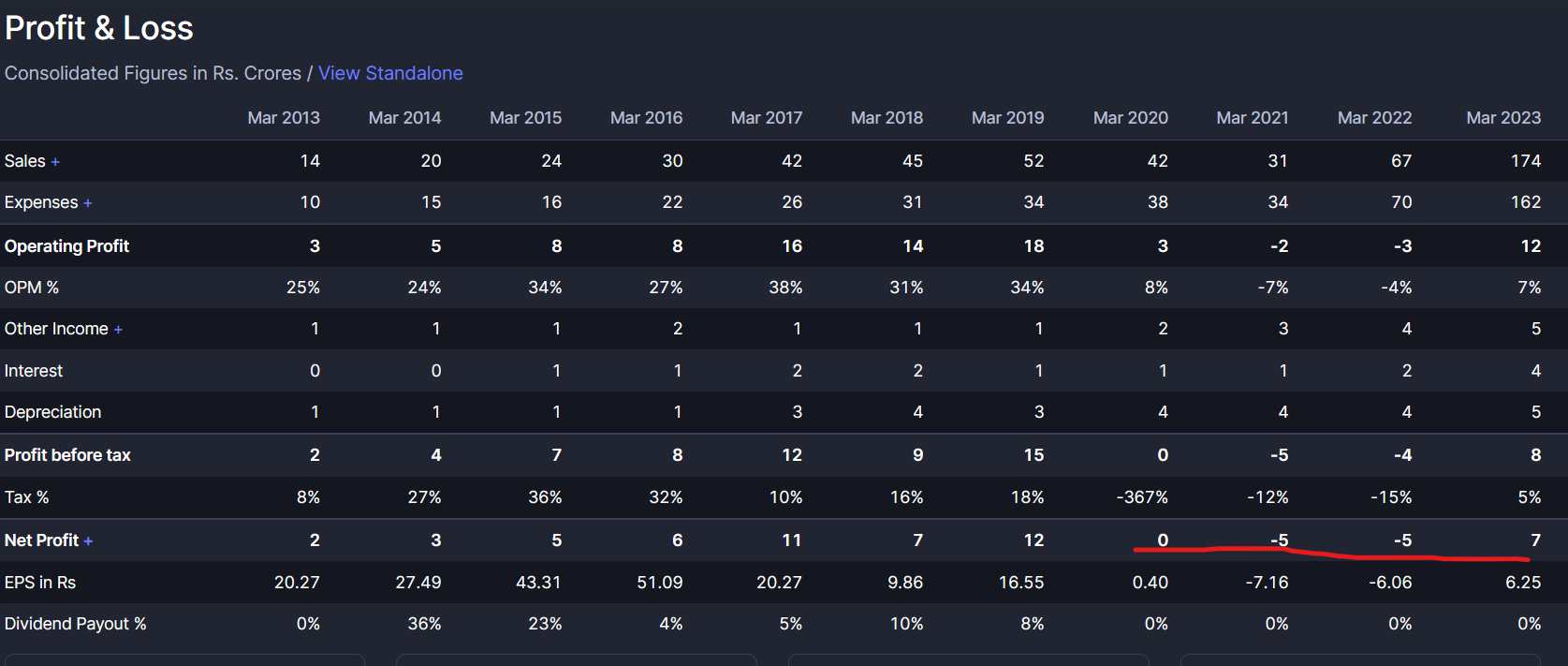

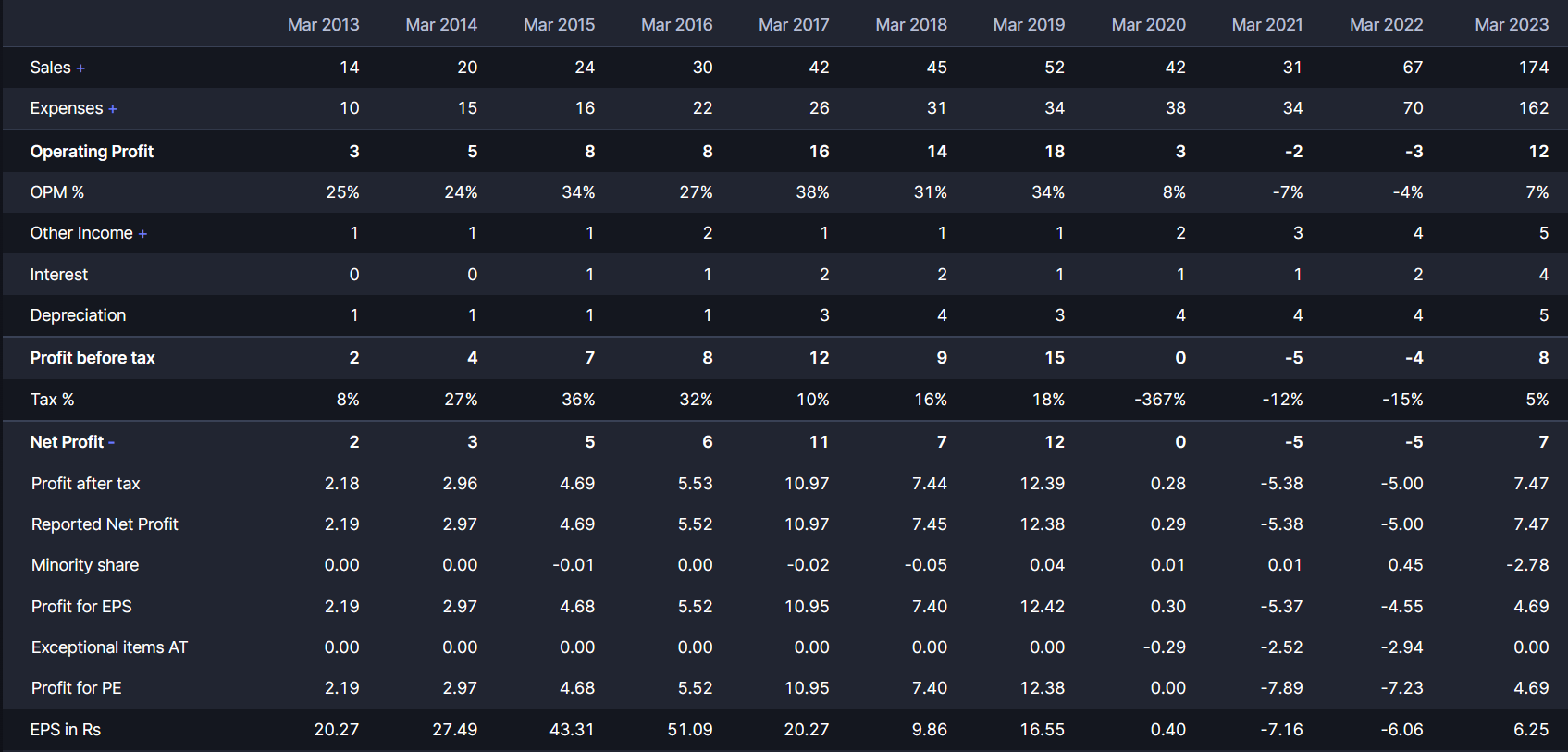

Financials:

Risks:

-

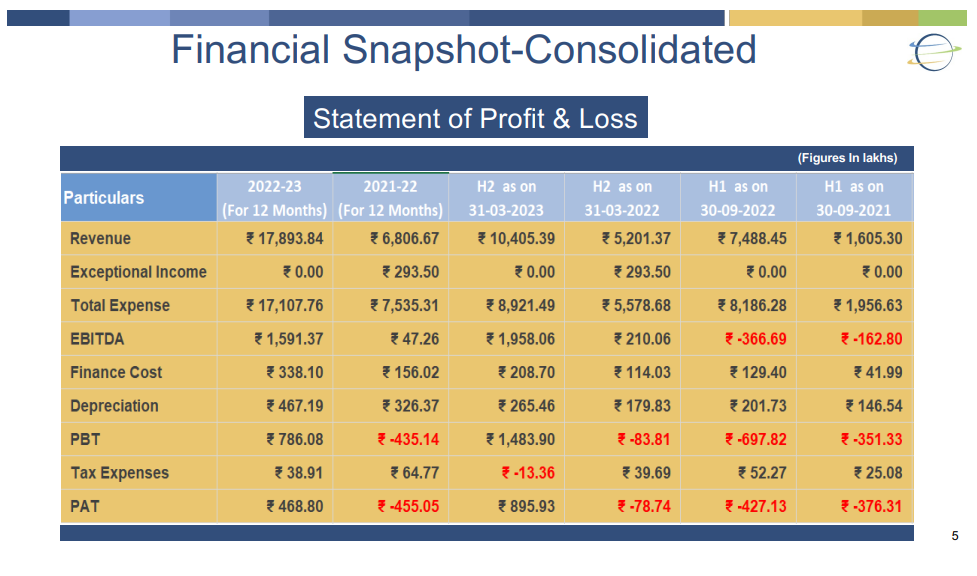

Company started seeing stress in FY 2019-20 amidst sales focusing purely in Apex Tech LLC and following Covid H2 FY 23 was the first half year of profits for the company.

-

Company’s Operating Cash Flows are negative to a big extent with major contribution of increase in Trade Receivables for both previous FYs.

-

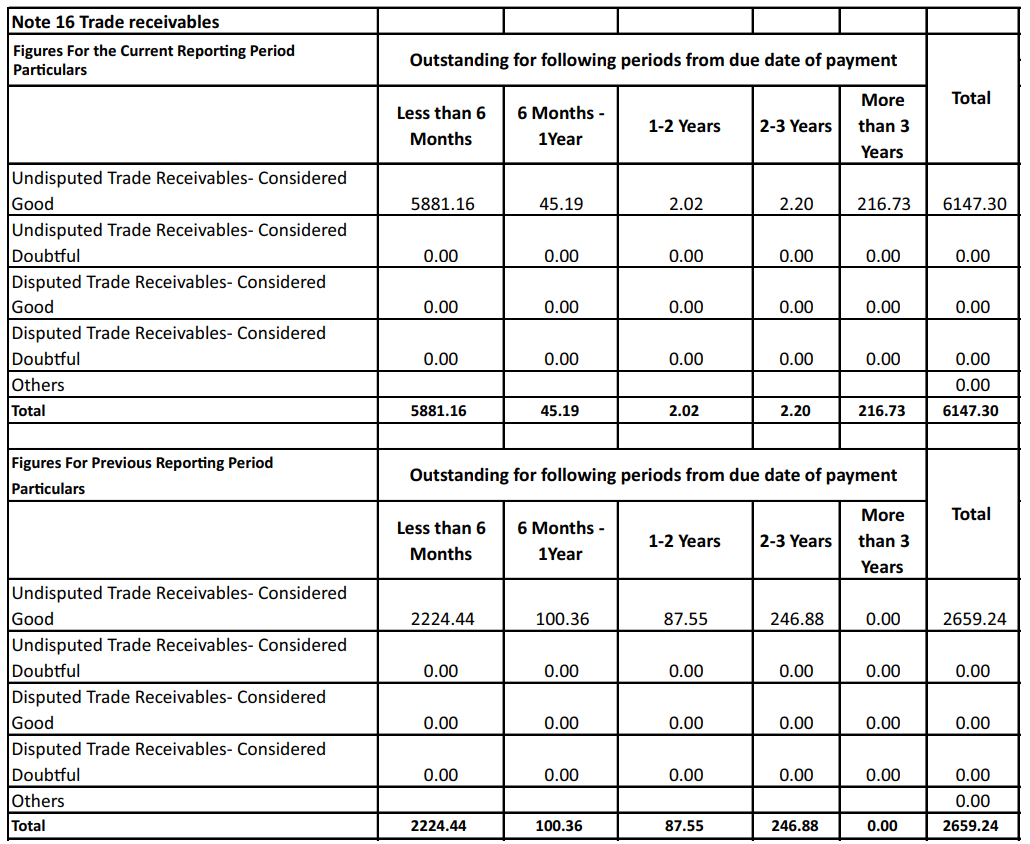

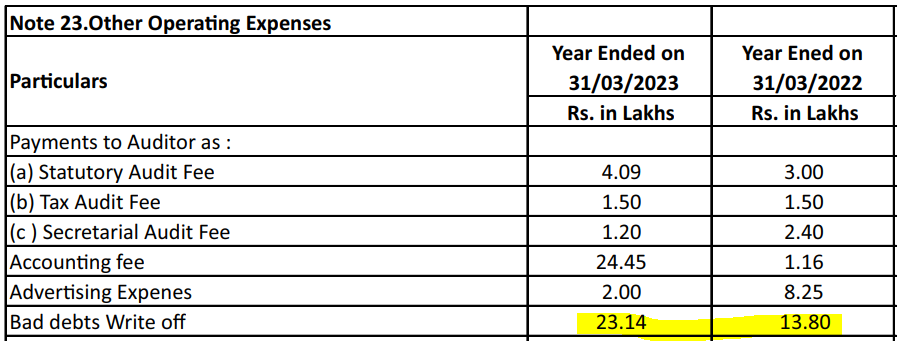

The company has 2.2 cr worth of receivables due for more than 3 years and they are also writing it off little by little every year.

- Debt:

The most troublesome part.

The company’s debt is in a ballooning stage.

From financials it can be seen that Company raises Long Term loans for servicing Capex as well as Working Capital. Almost all Long-Term loans are unsecured and all of those unsecured are raised from outside India’s financial Institutions. Current maturity is only 9% of long term debt indicating recently acquired debt/moratorium period or 8-10 years tenure loans.

- The books also show Goodwill payable to extent of 7.1 cr and a goodwill of 53 Crores (Irish Towers acquisition).

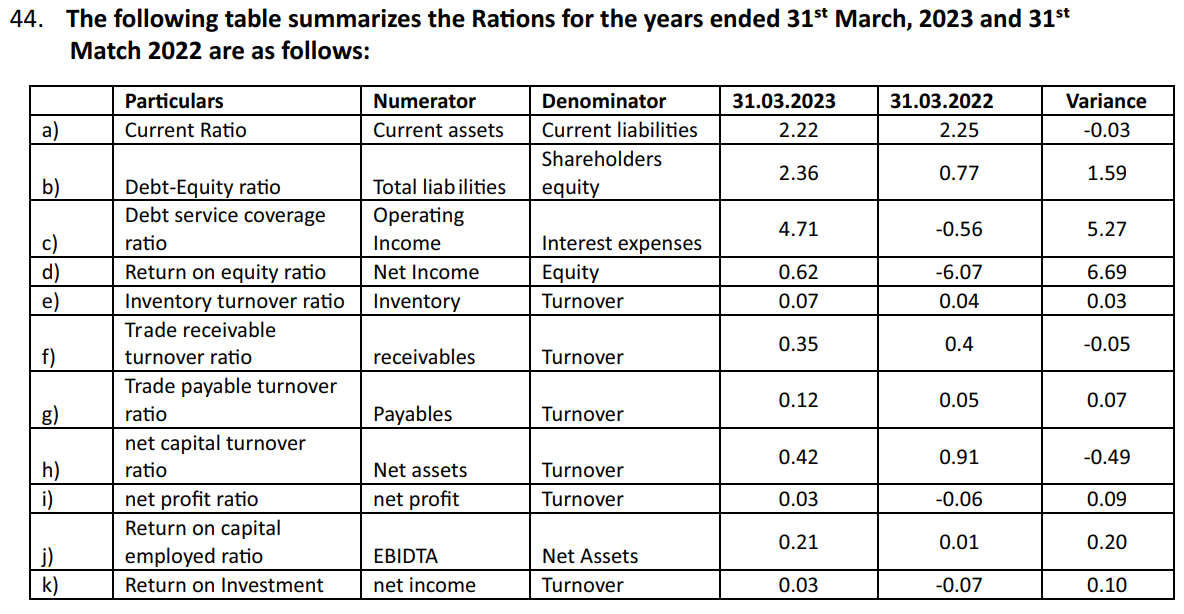

Ratios:

This thread seems to be discussing more on Apex Advance Technologies LLC rather than Cadsys itself, but their standalone Domestic business is quite miniscule on consolidated basis.

Disc: Current exposure is 3.96% in the Equity Portfolio.