Looking for a company to double their business and earnings within the next 2 to 3 years with reasonable value or A company available at 50 cent to a Dollar (Deep disount)

1 Like

***CA Bijo’s Portfolio and Investment discussion

I am a 33-year-old practicing Chartered Accountant from Kerala. Qualified as a Chartered Accountant in 2015 and started my own practice from the same year onwards. Also, a part-time faculty for CA students.

Even though qualified as a CA, I am a big zero in the investment field. However, the Lockdown period helped me to learn a little bit about the stock market. I have never learned about the valuation of a business or the power of compounding in my professional studies which is the irony of our curriculum. On a personal note, Our curriculum should have small coverage about personal finance and compounding effect because when one starts earning, they will make some investments and accordingly look for financial freedom in their life irrespective of the profession. I feel everyone needs to have some idea early in their life about personal finance and idea to generate passive income.

My spark on to know more on investments

A YouTube video of Damesh Ramani on the power of compounding was really an eye-opener for me. In Short, an investment of 10 lakhs in the present will become 100 core after 30 years when the investment can compound at 26%(CAGR) on an annual basis. I will be really happy even if I get 10% of that amount. So, it is good to know about the game of investing.

Core take away from reading and learning over last several months

My take away from reading and learning some good number of hours in the past. Sharing these points to get feedback and upgrade if necessary.

-

Reading books is very much important for an investor to create a framework. However, no one will make money if one reads only books. Reading books will help to create some investment framework or inspiration for our investment journey. Actual reading should be related to industry, company, economy etc.

-

There are so many ways in the stock market to create wealth such as intraday, momentum trading, cyclical investments, value investment, growth strategy, futures, options, etc. Don’t think anyone can master all these frameworks. The purpose of investment will be satisfied only when one could able to excel in any one of these strategies. Based on my taste or comfort I feel a long-term investment framework will be best suited for me. I prefer a peaceful investment process.

-

Direct investment in equities needs a good amount of research work if not possible then shift to mutual fund investing or other mechanisms than testing the heat of the water.

-

According to me, Patience is key to success in long-term investment. To hold the securities for years together let’s say 2 to 10 years really need some extra effort than reading and learning. How to develop so-called patience? Not sure but my efforts daily exercise of 1 hour and a 10-minute meditation. Also uninstalled all trading app such as Zerodha, Up stock etc. (time will tell whether all this work). I think I am not panicking now about what happens in the market. Will be worried when the fundamental estimates go against an invested company.

-

Invest during the correction period.

Why long-term investments

-

When you drill down Nitfy 50 chart on a daily framework and compare it with the same chart on the Monthly framework. We could see so many noises or ups and downs in daily or hourly charts when compared with monthly.

-

Real power of compounding will work only when the runway is big. Warrant buffet, the richest investor in all-time history has made more than 90% of his wealth after his 60th birthday.

-

In the investment fraternity, people are more worried or talked about inflation or sell-off by foreign Institutional investors, RBI moves or FED action or government stands, etc. So much of noise. Not interested to see so much of noise around me rather looking for a peaceful investment. 80 percent of talk or discussion goes on these topics. Have seen so many stocks recommendation or share analyses by many companies or brokers on a short-term basis. Very few instances have seen any research report or recommendation of a stock on a long period of basis. Are all these brokers creating our wealth or their wealth based on this short research or recommendation? Is all that the fundaments of stock performance. Have not seen many talks about fundamentals in the retail community about underlaying assets that is a particular company.

-

Theoretically, on a long-term basis when the company earnings increase its share price has to move up. Strongly believe the price has to move up when sustainable earnings increase in a long-term period.

-

Strongly believe the stock market in a yearly framework is always in a bull run. That may be in a particular sector or industry or a company, not all companies. Identifying such a company or share or market is more important than worrying about inflation, government, RBI, FED, etc.

-

Peaceful investment framework

-

Not possible to read and evaluate the impact of inflation, RBI policies, FED policies etc for a working person in an exhaustive manner. So, focusing on earnings and the value of a company. Today or tomorrow market has to realize company having strong earnings will upgrade its share price as well.

-

Have not seen shares are moved in a straight line from 1 to 100. It would have corrected many times when it moved from 1 to 100. That is part of the game.

-

One or two investments in a year is enough to create good wealth in a long period of time.

Purpose of writing

Too much of philosophy excuse me I thought of sharing my views on investments I have seen value picker form for the past several months and really amazed about some people’s analysis and deep study about companies, industry etc.

I am looking for

-

Your views or advice or critics about my investment thesis.

-

Main purpose, I shall share my long-term investment bet from the next message onwards so expecting valuable feedback.

-

Really interested to know about any company which may double their earnings in 2 to 3 years’ time so I can study about it or a company which available 50 cents to a Dollar (Deep Discount).

Thank you so much for reading this

5 Likes

Satia Industries Limited (SIL)

Date of writing: 08/03/2022

Source/Disclaimer: I have collected the information’s from Annual reports, quarterly reports Concalls, News, Research Reports, investment forums, etc. I am not a SEBI registered adviser. Kindly consider this discussion for knowledge purposes.

Investment thesis

I am looking for

- a company which could able to double their business and earnings in next 2 to 3 years with a reasonable valuation.

- Company to get benefits on reopening of schools

- Government ban on plastics from July 2022

Why invested in Satia Industries (SIL)

- Current turnover around 750 crores and company has already put up huge expansion plan. They expect to reach 1500 Crore turnover within 2 years. Expansion is already done

- Currently SIL available at 10 P/E (08/03/2022)

- Current PAT is 90 crore (could see the same margin for past years) with a turnover of about 750 crores. Management expects 250 crores PAT within 2 years with turnover doubling to 1500 crore.

- Current Market Cap is 923 Crore. Share value Rs 93 per share.

- So, if it can increase earnings to 250 crores with the current valuation SIL should trade at a Market Value of Rs 2500 Crore. i.e Rs 250 per share.

- Seems enough room for Margin of safety with current vale. Bullish and added in long-term investment portfolio.

About the Company

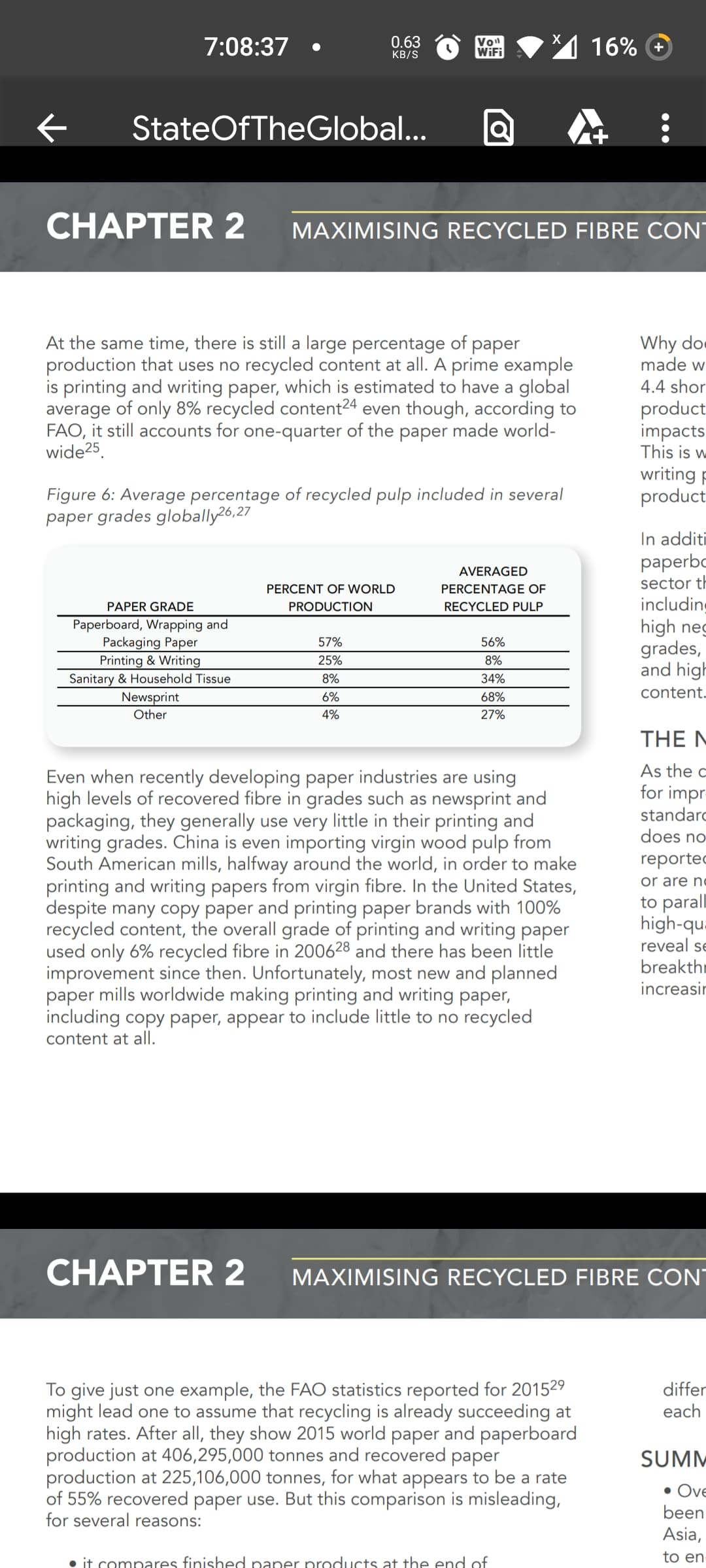

Incorporated in 1980, Satia Industries Limited (SIL), is one of the biggest and completely integrated Wood and Agro-based paper manufacturers. Its products are extensively used in the printing of books, directories, envelopes, diaries, calendars, computer stationery, copy manufacture annual reports, etc.

Journey & Key Milestone

Current Status

Market Cap: 923 Crore (08/03/2022)

Market Price: 92.3

52 week high/low: 119/73

Stock P/E: 10 (look reasonably valued)

Sales avg: 700 to 800 Crore

Operating Profit Margin: 22%

Capex Program

SIL currently has a paper manufacturing capacity of 105,000 TPA and a total in-house pulp processing capacity of 400TPD (50% agro-based, 30% wood pulp processing, and 20% waste paper processing). It is currently undertaking a capacity expansion of 100,000TPA (80% wood pulp-based) at a cost of Rs 500 cr. This fourth paper machine is expected to be operational by Q4FY22 and has the potential to contribute INR 620 cr per annum to the revenues.

Key factors that are driving the growth of the Indian Paper Industry

a) Underpenetrated or underdeveloped market

13 Average per capita consumption of paper in India (in kg).

China’s per capita Consumption of paper is 65 kgs

USA’s per capital Consumption of paper is 312 Kgs

The global average for per capita consumptions of paper 57 kgs

Hope there is a huge opportunity in India for large players to acquire the market share

b) Growing Online Food Delivery & E-Commerce business in India

SIL has entered into a manufacturing contract with Zume Inc. for the supply of patented paper cutlery products. These sustainable products will be manufactured by SIL from compostable plant-based fiber and technology provided by Zume. SIL also has a buy back arrangement with Zume for the purchase of its entire surplus manufacturing.

c) National Education Policy (NEP) to boost the demand for textbook paper

d) Increasing no. of Schools, Colleges, and Literacy rate in India.

e) Government plan to ban on plastics from July 2022

Reasonable debt after Capex program

Current debt ratio .62

From Research Report

The current total debt stands at Rs 344 cr (Rs 228 cr long term and Rs 67 cr working capital and Rs 49 cr current maturity of long-term debt). The ongoing CAPEX worth 500 cr is being financed through fresh debt of Rs 325 cr and internal accruals of Rs 175 cr. Despite the CAPEX, the total debt is expected to come down to Rs 275 cr by FY24 (Rs 120 cr long-term debt and Rs 96 cr working capital and Rs 55 cr current maturities of long-term debt). We expect SIL to repay the remaining debt over the next 5 years and the company is expected to be net debt-free by FY24.

4 Likes

Just to be clear the paper they produce and real growth market is offering might be quite different.

When we see india vs China vs usa paper consumption the main take away is our packaging consumption of paper is tremendously low in comparison.

Link to check :-

Also we also see that the tend of writting and main paper that it mentioned might be in a decline and is shrinking.

Also can see shrink in these paper overtime by many analysist.

Link:- Top countries for Paperboard and Packaging Paper Production

If you really want to see how Industry is changing do also study over jk paper they are getting huge on packaging paper does this company also support that and also to add jk paper is also one of the lowest cost producer advantage.

If you can skip many things in itc concalls and search what you are looking for then can also read that.

I personally have some info about stationary industry and in term of textbook and paper that atleast you mentioned are in a decline both in retail and wholesale as many of my family members have buisness in this sector.

Also do note in paper you are just selling a comodity and right now you might be stuck at worst spot many times.

Have personally left paper industry long ago by 2-3x in jk paper and after reading and looking forward untill there is a huge downfall it’s not something I personally will invest on.

Do check will there margin are at top or not and if industry is hurt bad after huge influx of raw product from China, Indonesia and others.

Also do check the industry margin these 20%+ margins never sustainable even for big players like jk paper they fall very easily and your 250 cr pat might not be possible as more often margins are in range of 15 and even sometimes less then teens.

So with more average of 17% opm we can get around 210-220 profit before all other like tax or interest you can cut and get according and if it fall in comodity down turn to 8-9% then is around 100cr-140cr also.

If you are taking a estimate don’t take more then 15% margin as they will not be there on 22% type margin for very long.

You might still get decent returns but if comodity cycle Play it’s game badly and they reck up debt to expand then investment could be in real problem.

3 Likes

Thanks Bijo , nice wirteup indeed.

May also refer @kalpesh4430 portfolio thread, he has done good analysis on Satia.

1 Like

KITEX GARMENT LIMITED

About the Company

Established in 1992, Kitex Garments Ltd (KGL) is into exports of cotton and organic cotton garments especially infants wear located in Kizhakkambalam, Kerala.

World 2nd largest infants wear manufacturer

Per day production 4.5 Lakhs units with 4600 employees in payroll

Kitex also supplies to Jockey International. Most of their sales are export to US market.

Recorded highest turnover of 730 crore in March 2020.

Touched Market capitalisation of 5000 crore in 2015

Company enjoys EBITA margin of around 20% in past several years.

Infant wear is a specialised product.

Figures (based on 18/01/2022)

Market capitalization 1732 crore

Debt-free company

P/E – 22

Future Plan (Based on MD comment, report, MOU, Director’s discussion)

Kitex have a CAPEX plan of 2406 Crore and on the political issue, they have decided to move out from Kerala (Not an investor-friendly state) and invest in Telangana State(Number 1 state for ease of doing business in India).

MOU with Telangana Government has signed by the company for Capex plan of 2406 Crore. Kitex will be investing in 2 textile parks in Telangana state.

• Kakatiya Mega Textile Park, Warangal – 1113 Crore

• Sitarampur – 1293 Crore

Kitex has formed a subsidiary company in Telangana called Kitex Apparel Parks

On completion of the above to project company expects target sales of 4,000 crores. (Current sales of the company is 700 crore). Which is 4 to 5 time upside growth

Kitex will become world largest kids wear manufacturer. Current production is 4.5 Lakh units per day (largest player is from china having 5.5 Lakh units’ capacity per day).

Kitex capacity will become 18 Lakh units post expansion of above mentioned 2 units.

Capex has already stated in Kakatiya Mega Textile Park, Warangal project and expected to commission from December 2022. Project in Sitarampur will kick start from December 2023. So expecting full capacity from the company in 2024 onwards.

Telangana state is 3rd largest cotton manufacturing state in the country. So kitex can easily get these cotton which is the principal raw material for the company.

Offer from Telangana

The government will give an interest subsidy of 8%. So, the company can run the business with 1% or less interest for 5 to 10 years.

Income tax exemption

PF/ESI Exemption

Income Tax 8% Saving u/s 115 and 1% save 80JJA

Easy procurement of cotton from the state because Telangana is the 3rd largest cotton producer in the country.

Cheap labor, water, land cost etc.

Top of that Company will benefit from Central Government PLI scheme of 10,000 Crore.

MD says over 6 to 7 years company is going to get 70 to 80% return from the government in the form of various subsidies.

Management

The success of every business lies in the hands of its management.

No wealth will be made if operator is not capable enough. In other words, a good management can make wealth even if they run bad business.

Kitex group has made nationally recognized brands over last 2 decades that too from not an investor friendly state in India. Their major brands Chakson pressure cooker, Sara’s curry powder (Sister concern of kitex run by MD’s brother) and kitex infant wear.

Many companies failed to manufacture When NASA needs some special dress which will adjust based on climate change including Aravind mill and later the same has manufactured by kitex group for jockey who supply said items to NASA in USA.

My bet on Kitex (Why I invested)

Proven management

• 3 well-recognized brands created by the group.

• Run the textile business for the last 2 decades with above industry average EBITA margin.

• Moving out from Kerala to the best investor-friendly state.

• Infant wear manufacturing is not easy to start so many are not involved.

Business perspective

• Expansion is 4 to 5 times more of the existing plant (Expecting to hit 18 lakh units per day against current capacity of 4.5 Lakh units).

• Incentives from the Telangana government. (Tax exemption under income tax and interest subsidy of 6 to 7% which will result in 75% of investment of 2500 crore over a period of time).

Some calculation corners

My entry was when share was trading at 170/-

Share price - 170

Share Capital – 7 Crore Shares

Market capitalization (170*7=1190 Crore).

P/E – 15/-

IN 2016 Company’s market cap touched 5,000 crores with a turnover of 700 crore. Management says 2022 will have the highest turnover in the company)

On future (perspective)

When they complete plants in Telangana top-line touch 4000 crore

Keeping same profit margin – 10% = PAT = 400 Crore against current year 100 crore PAT)

Multiplying with current P/E = 400+100 = 50015 = 7500 crore market cap

If market is crazy about valuation in 2016 when p/e was 40 then valuation will be 50040 = 20,000 crore.

So share price may hit = 20,000/7 = 2875/- (Oh my god). Forget even if it touches 1000 great return (fingers are crossed. Time will tell).

Assume when they get 8% tax exemption and 8% interest subsidiary the profit can double or triple. No, I don’t want that calculation.

Summary “Heads I win; Tails I don’t lose much” borrowed from Mohnish Pabrai whose thoughts have influenced me a lot

Concern

Management runs a non-listed sister concern of similar business

No idea about company funding plan for new CAPEX of 2400 crore.

The market is all-time high and any correction can have an impact of all shares irrespective of the performance of the company

Highly labour and CAPEX intensive industry. Scaling up with such huge labor can be a concern

All figures are based on comments from management. Need to wait and see how demands pick up

Highly dependant on 3 to 4 suppliers.

Vietnam and Bangladesh are more competing companies in the sector when china plus move starts.

These return will be expecting 4 to 5-year time frame.

My entry was at 170 range and now share trade at 265 Range (30/01/2022) Seems bit priced based on current earnings.

My view can change and I will exit based on future developments so keep it as only a discussion for education purposes.

4 Likes

Thanks. Good write up

Disclaimer: This writing is intended solely for educational purposes and to foster an understanding of differing perspectives.

Updating on my thesis shareholding

Some style which suite for me

I look for a peaceful framework basically long term investments

In the long term, I seek a value-plus-growth style. This entails identifying companies poised to double their business and profits over a three-year period and entering positions only when shares are underpriced. Theoretically, this approach should result in shares doubling over an extended period

Another style a turnaround story

another a future trend

*Exited positions

- Swaraj suiting’s - Value plus Growth

Brought when company market cap was 40 t0 50 crore and share price was Rs 25 and book value of share was Rs 50.

and saw company putting capex of 70 Crore.

Brought at 25 and exited around 90

- Zee and Rajesh Exports (Swing trading)

Made 20% profit in zee and Rajesh export a loss of 35% and cumulative loss was 15%. Realised Swing trading may not work for me.

Holding/Partial Exit

- ITC - Dividend plus value buy

Brought at 205 by looking at dividend yeild and cheap valuation.

Expectation - No exit or expectation plan

- Max India (Future theme)

senior care may be a growing business

Brought Max India around Rs 80 Range.

Expectation - No much because i see this model should go for a long period of time may be many decades in India due to migration and nucleus families.

- NTPC (Value plus Growth)

Brought by looking dividend, future plans, value. Purchased at 90

Future - No plan on exit wait and see how power business gear up in India

- Satia Industries (Value plus growth)

When I brought Satia it was almost doubling the business and my calculations was right and the sales from 890 crore went to 1800 crore and PAT also doubled from 100 cr to 200 cr. And paper companies were trading at 10 PE. And thought Satia will also trade at 10 PE. If then Satia should trade at 200 to 250 range.

Not disappointed because share went from 80 to 160 and back to 120 range. Will hold for few more years seems it is a marginal bet at 80. Let’s see how things goes in the future.

- Supriya Life science - Growth story

too much impressed on management integrity and their future road map over 3 years. They are planning 500 crore capex (current + future) in next 3 years so normally pharma may have 3 time assets turnaround. so expecting sales around 1000 to 1500 crore and PAT of 300 to 400. and valued at 30 P/E. so market value should be b/w 6000 crore to 10,000. So market should be valued at Rs 1000 to 1500 per share. would be happy if share goes over 600. ( I brought around 290/-)

- Gulshan Poloys - Growth - Ethanole business

Brought at 200. company is expanding ethanol business. already having sale of 600 crore (doubling the business). Risk i see Raw material price.

- Kitex - Value + Growth + Turnaround story

Existing unit in kerala near my home. Market punished this company from 5000 crore valuation to 1000 crore value. Major reason MD’s entry into polities + few corporate issues.

what interest - Company is 2nd largest kids wear manufacture in the world. Company putting 3x business expansion and exited from kerala and moved to telegana (received many incentives almost 60% of their investments comes from govt as subsidy etc.)

Company has already put one factory which is world largest manufacturing unit

when company is expanding its business into 3 times in a investor friendly state. expecting share should trade above its peak value in 2017.

6 Likes