National Peroxide Ltd. - A company of Wadia Group. NPL is the largest producer of hydrogen peroxide in India with an installed capacity of 150,000MTPA (50% w/w) at its fully integrated manufacturing site in Kalyan, Maharashtra. The company has a share of 40%-45% in the domestic market.

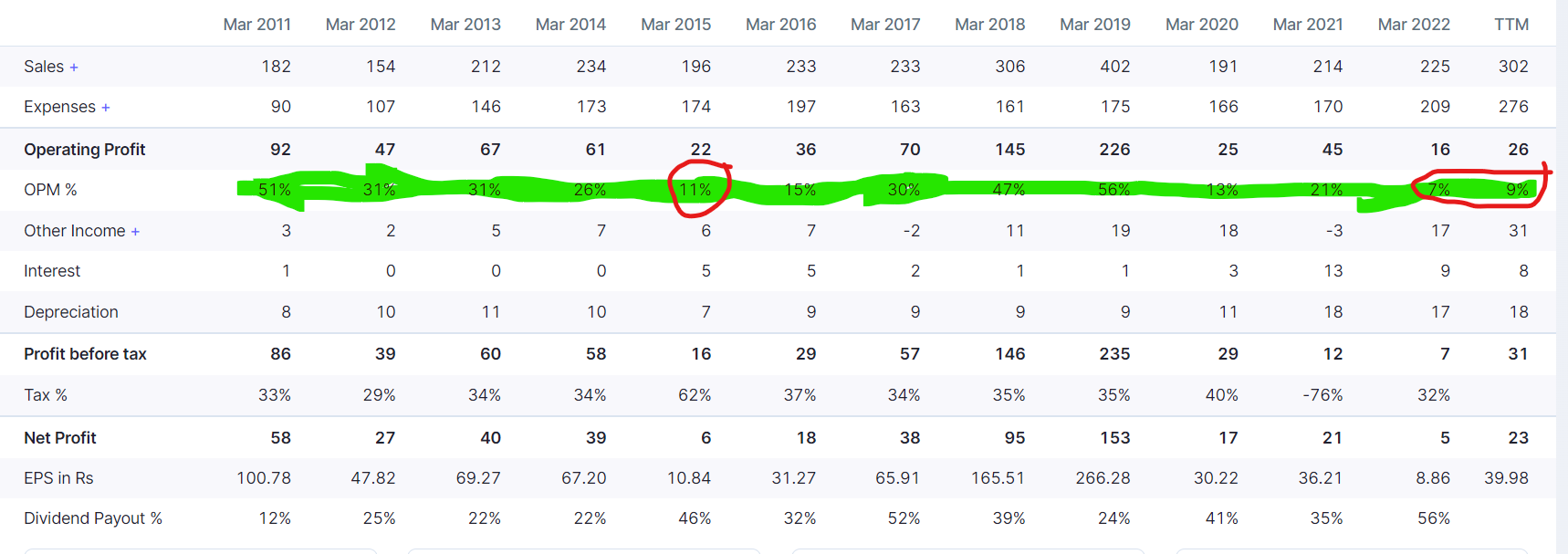

The capacity expansion was completed pre covid in 2020, unfortunately things went south after that. There was excess supply and no demand. The company had to shut down plants for couple of quarters.

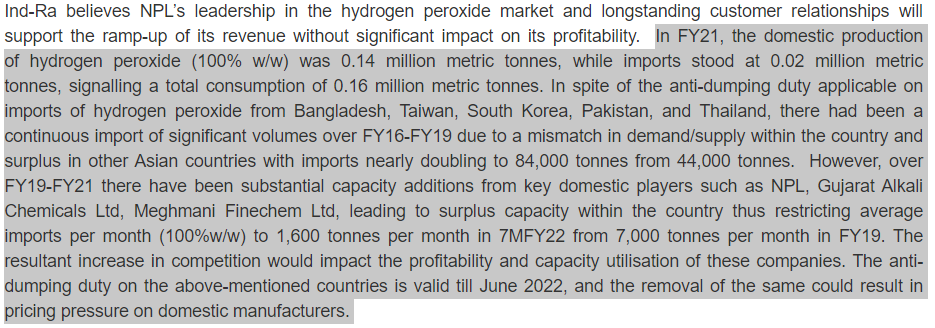

Source: Credit Rating report

However as far as I could find the anti dumping duty has been removed in as per the hearing in September 2022

Source: Directorate general of trade remedies>> Anti dumping cases>>Hydrogen Peroxide originating in or exported from Bangladesh, Taiwan, Korea, Indonesia, Pakistan and Thailand

Apart from that the major raw material is hydrogen, which in turn is a derivative of natural gas, which in turn is a derivative of crude oil. With natural gas prices soaring through the roof post covid. The margins were hit terribly going through the all time low. But things are cyclical and as of today you can see the price is less than $4/mmtbu both in USA as well as MCX, they have almost halved. So I am hoping margins would improve further. With the same rationale I find MGL also interesting.

Talking about the debt, the company has reduced its debt substantially

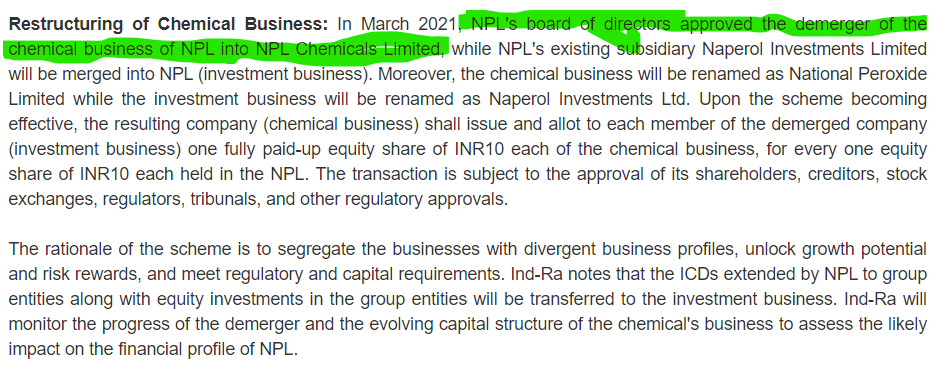

The company is also planning to demerge its chemical business and investment business.

Source: credit rating

Lets see what has happened to the stock price:

Will the same cycle repeat? I dont know but I feel there is a reversion to mean that is pending here. The worst as much as I can see is behind. Downside looks limited. Lets see what is the upside.

Disclosure: Invested