When one buys an Index fund, the fund is allotted at Net Asset Value (NAV). Net asset value is basically computed by determining the value of the underlying assets as of close of business day. As a rough example, if the fund holds shares who’s market value is worth 100,000 INR and the number of units of the fund is 100, then the NAV is computed as 100,000 / 100 = 1000 INR per unit. Thus when someone tries to buy this index fund through the AMC, they are allotted units at 1000 INR per unit. The mutual fund creates new units to accommodate your request.

On the other hand, when you are buying an ETF (of a fund with the same underlying assets as the earlier example), you are really buying the unit from another holder of this ETF, new units are not created. Now, this holder of the unit need not necessarily sell his holdings for 1000 INR per unit. He may want more or less and could quote accordingly. That is why you can purchase (or sell) units in an ETF for a price that is different from the NAV. When buying or selling through ETFs, it is necessary to make sure that you are aware of the NAV of the previous closing day, and have some sense of how the underlying assets have moved today so that you are able to buy / sell at a “fair” price.

Tracking error is different. Tracking error is the difference between the return that that fund provides and the returns that are determined by the index. Example the Nifty 50 as computed by NSE may have given 15% CAGR, but the mutual fund that offers a Nifty 50 index fund may have given a returns of 14.5% - this difference is tracking error. Why it occurs is a topic for a different day.

Other items you need to be aware of when choosing between ETF vs Mutual Fund

a. Mutual Fund purchases have the direct vs regular option. Direct plans offer comparatively more return because of lower cost. ETF - you need to pay brokerage of every buy/sell transaction and a fixed charge by the AMC.

b. You need to be aware that liquidity of certain ETF index funds may be low. When you want to buy or sell there may not be enough people selling or buying. This is not an issue in a non-ETF investment as the mutual fund simply sells the underlying assets and returns the money to you. Of course, ETFs do have a process wherein if the ask price is way off the NAV you can approach the mutual fund to buy your units at the NAV.

@shivramrca Shivam explained it beautifully. Just to add; this won’t happen usually. Further to that MF is a no-brainer activity, you, me or the expert gets at the same cost. Where as ETF price depends on market volatility. Said so both largely depend on underlying assets say NIFTY 50 in our example.

@Deven Could you please suggest some ETF’s which are stable and you have personally invested in those. in current environment, really confused to pick stocks. So looking for stable ETF with less tracking error and minimal divergence to NAV.

I am invested in SBI-ETF Nifty 50 and Nippon India ETF Junior BeES - both ETF and Index funds of SBI & Nippon. Besides that, I have Motilal Oswal NASDAQ 100 ETF & Index fund. However please stay away from MON100 as due to restrictions from RBI it’s not giving true index matching. Recently I invested in Kotak Nasdaq 100 fund instead of adding in MON100.

@anekmmm Further to my above response, am invested in CPSE ETF from Nippon MF. Am not invested in any individual PSU stock hence am participating PSU via CPSE ETF.

We don’t need to invest from different fund houses, these are all subjective decisions, entirely personal, we can make our choices.

It depends on the accumulation of units, if you think you will be buying a lot over the course of time, then I think it is better to invest in different AMCs, if the corpus is going to be big. Also, the AMC may increase the TER, the tracking error may increase, so I guess, you can invest in more than one.

Depending upon the tenure of the investment, amount invested, tracking error, history of the fund etc, we can choose a fund, or go by fund house or fund AUM.

Invest in funds despite low AUM from a reputed fund house like HDFC, or invest in funds with big AUM from a relatively lesser known fund house like UTI. And as time progresses, bigger AMCs may get more share in index funds surpassing UTI like fund houses, so may be we can invest in only bigger AMCs but in more than one.

Thanks for the reply…Just one correction…You have said UTI as “lesser known AMC” But actually UTI is the Grandfather of Indian Mutual Fund Industry.It is the first AMC to launch mutual funds in India. You might rmember US 64 Scam of UTI…It was the biggest AMC in India for decades.

Currently I am accumulating units in UTI Nifty Index fund and UTI nifty Next 50 Index…May be as suggested after it reaches to some significant level…I will put in HDFC Nifty index and ICICI Nifty next 50 index

Yes, UTI in public and Kothari in private. I said UTI is a relatively lesser known fund house, when compared with well known bigger fund houses like HDFC, ICICI, SBI, Birla etc, but it has got big AUM in index funds.

We can choose more than one fund house even with index, because we never know when the TER will increase, and I think TER gets increased by almost all the fund houses, if one increases, others will increase too. I am not sure if tracking error can be directly linked to the management of the fund, but if it is, then the change in manager may bring a change in tracking error. So it I think, not just w.r.t the units accumulated over years, considering TER and tracking error too, investing in more than one fund house sounds good.

Psychologically too, looking at a big corpus in a single fund may not feel better to some, so diversification among fund houses can be looked at.

Read the whole thread and what I understand is that Index fund is better for longer horizon of 20 years as compare to ETF.

I was planning to open demat account for my daughter so that I can buy nifty bees monthly for her. But now I think Index fund + Small cap in 40:60 ratio monthly sip will serve the purpose.

All views are invited. Disclaimer: Already started Sip in Axis mutual fund in 40:60 ratio in Nifty 50 index fund and Axis small cap fund.

How does this work? Does the child need a PAN number of his/her own? If there are capital gains who will be taxed - parent, source of income, or child?

Let me know if this is off topic and I’ll remove it.

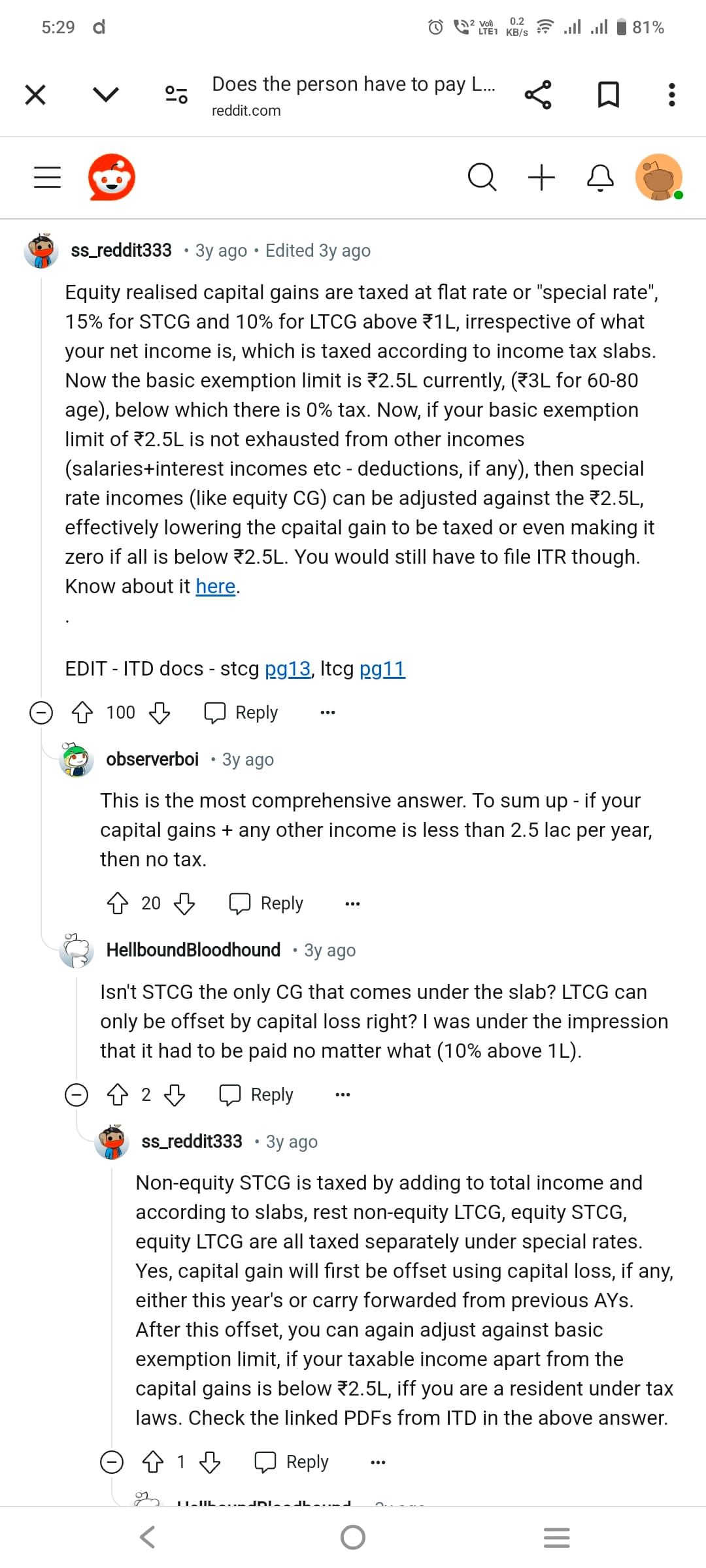

I have one silly question to ask for which I am not getting the answer. Are Long term capital gain or short term capital gain on equity is taxed at 12.5 % and 20% irrespective of your income slab?

I’m glad you asked this. I have seen you commenting in many threads and felt surprised that you asked this seemingly silly question. I felt that the LTCG (beyond 1.25L) and STCG were applicable irrespective of the tax slab. However I was wrong. There’s a basic exemption limit of 2.5L (3L for senior citizens) until which there is no special rate taxes as well.

Respected senior members, I have one query which is not matching with thread subject.

How to avoid clubbing of income in case of HUF?

HUF is good in the sense that it decreases tax liability, but to introduce corpus into HUF for individual professional only rely on monthly salary is difficult task.

Without any ancestral income…this seems to be difficult to gain any tax advantage from it.

I am looking for opinion of community about investing in Nifty 50 and Nifty Next 50 Index Funds. How is the experience ? Many articles claim that, Next 50 is volatile similar to Mid caps though those are part of large caps.

I am currently invested in Nifty Low Vol 30 Fund and experience is average since market sentiments are not so positive in the past 1 year. But my position is small.