I would like to start a SIP in some indexes. I have done some initial checking but I was not able to get clear answers.

Some articles said that you may find that index funds are not liquid; that there may be a big spread in the buy and sell price; they may not track the index fully and that they may sometimes take a decision to keep cash etc… which I found not appropriate as the whole point of an index fund is to not take a judgement call but just track the index.

There is also the issue of charges which seem quite varied by fund to fund and should actually be the lowest as they have no cost of making decisions.

I am quite confused

What exactly is the right way to look at index funds? Which are the good index funds with least tracking error and have the desired liquidity?

I am primarily interested in our main indexes the Nifty, the Sensex and also maybe the Nifty 500. Other ideas and opinions welcome.

This is totally new to me so any advise that can help is most welcome and also might help other readers.

sector specific ETF’s are also available. Ex: Banking.

Regarding liquidity, from my experience it’s hard to get large volumes at the same price at times. ETF’s are just traded like stocks. Note: The Fund house will charge the Fees for running the ETF’s and ensuring liquidity, usually the charges are very less for ETF’s when compared to mutual funds, few ETF’s pay dividend’s as well.

While ETFs can be bought and sold on the NSE/BSE, they suffer from liquidity constraints, which can also lead to higher spreads in case one wants to quickly get out of the ETFs.

My recommendation would be a low cost MF which invests in the NSE/BSE component stocks rather than a MF which in itself holds an ETF. The problem with the MF holding an ETF as the underlying asset is that you get charged twice for the expense ratios (once by the ETF and secondly by the MF).

To the question where MF’s keeps cash with them: MFs would have to keep some cash with them to service the redemption requests that they may face as a business as usual practice. To address the concern on the MF taking cash call, i would suggest that the Beta of the MFs may be looked at, For eg. you can have a look at UTI Nifty Index Fund which has a beta of 0.99 and an alpha of 0.86, meaning its not getting an head start with respect to the index and is closely tracking the index itself.

Another such fund is IDFC Nifty with beta of 1 and alpha of 0.79.

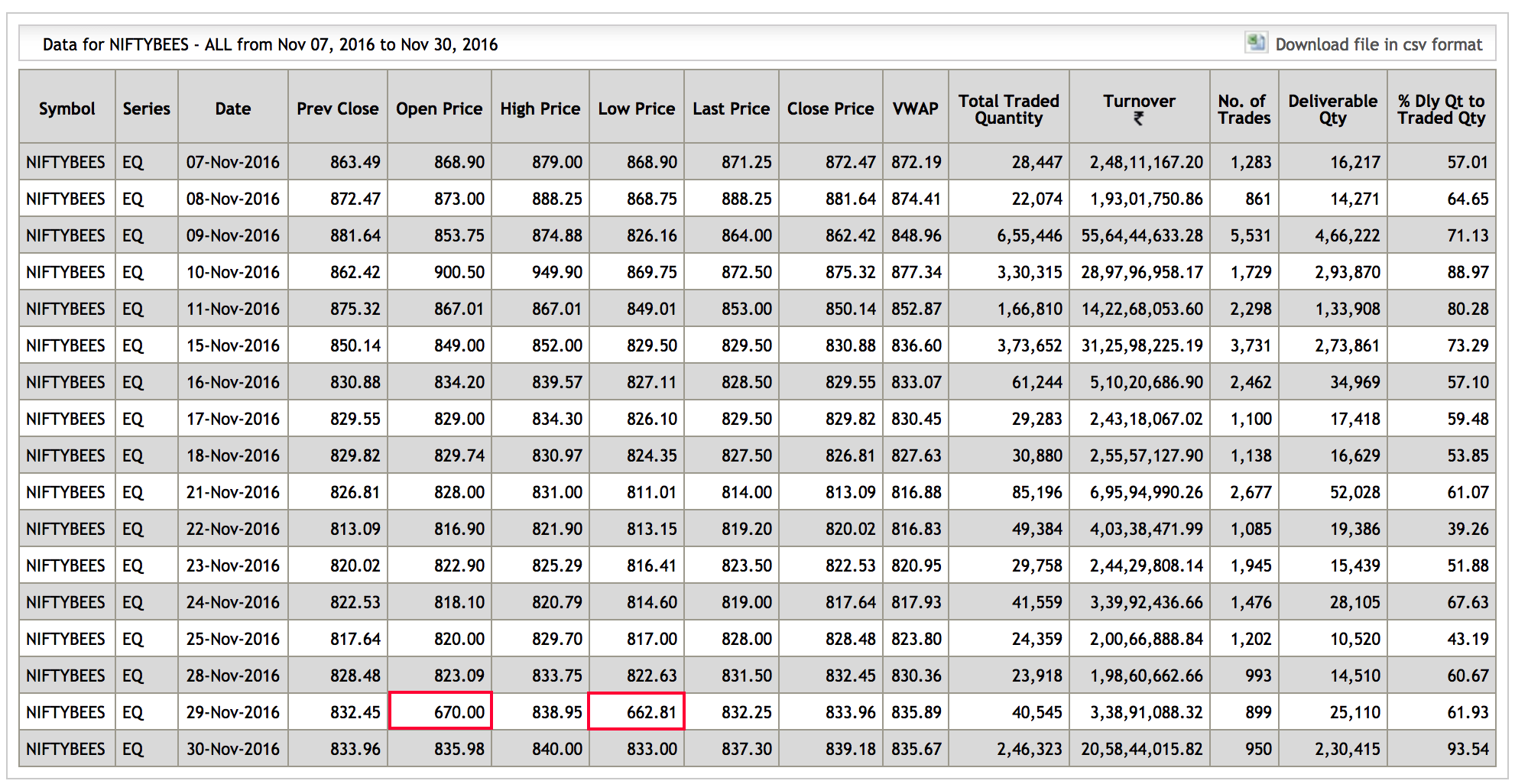

I was looking at some data for a generally more liquid index tracker and found that NIFTYBEES seems to be fairly popular.

I am attaching a chart for an anomaly I found… yes, the above comments seem to indicate the vulnerability of parking cash in these index funds… I am really wondering how to go about it…

The mutual fund route is quite expensive if all I am looking to do is track the index

You can directly transact through AMC… In nifty bees case it’s min 5000 nifty bees that you need to purchase if you want to transact directly with AMC.

Hi @Ameya_Dharmadhikari My friend is an NRI and unfortunately can only invest via ETF’s via the DEMAT if he wanted to, since then the profits when sold are not taxed (income tax, not capital gains which are taxed). That’s my friends dilemma as it adds a big boost to returns when there is no income tax. What’s the friend to do then Seeking this answer too… sorry I did not clarify this earlier.

Thanks Ameya. Is PIS the same as PINS? If not, great tip, if yes PIS and PINS is same, then the issue is only liquidity when trying to sell. My friend does use his PINS account to buy equity. Some further good advise please if you have some solution.

Read it… The PIS is what we call PINS

I will ask my broker tomorrow. It might help my friend.

Thank you so much Ameya. You are so helpful. Much appreciated.

If it is worth the effort, an investor focused only on Nifty-50, can himself run a personal ETF. I mean, he could download the weightage distribution sheet from NSE website and buy those 50 scrips in exact proportion.

This has two advantages

saves the known expenses and fine print ones too

allows flexibility. For ex. I do not want to buy the telecom space ever or the cyclicals when they are high or buy more of hero honda when its cheap or tcs at lows… point being, one can be a selective when an opportunity is clear.

there is a draw-back too…

The retail investor is a step behind on information. He would be last to know of scams, news and quarterlies. He would adjust only when NSE website gets updated, which happens at month end. Unless, he chooses to take decision on his own.

I remember when Yes bank news was getting circulated, I too was unsure what is right. Some on VP were buying, some were selling, and both sounded right.

If I owned an etf, I would do nothing, but if i were personally running an ETF I would be terribly confused.

It is a lot of work, and would require enough experience.

When many ETFs are available covering equal weight, strategies, quality, international markets, why take the pain of running a personalized ETF when so many unknowns exist? Regarding the expenses, the expense ratio is lowest of all the available options, it is less than actively managed funds, less than index funds. One thing that is true is the difference between price and NAV.

Some ETFs are traded close to the price of their NAVs, others not so, they usually trade at a premium (the price you pay per unit is more than the NAV) or at a discount (price is less than the NAV). Premium indicates demand for the ETF. Case in point Motilal’s NASDAQ ETF, it always trades at a premium, many want it, understandably so as it has allocations to all the giant names. Juniorbees more or less trades close to its NAV.

One of the reasons why index funds are suggested compared to their counterpart ETFs, along with the liquidity issue if the buyers are asking for a low price and we are stuck with a few thousands of units which we cant sell to fund house either, so we have to wait. Hence index funds are suggested for serious investment not ETFs.

In Nifty 50 ETFs there is liquidity issue in most. But, there are a couple of Nifty ETfs that are always liquid enough. Most liquid is SBI ETF Nifty, it has over 40000 cr in Aum.

Buying, large cap funds instead of ETFs is dicey. Most underform the index and have expenses as high as 2%. Whereas ETFs hv zero expenses.

In this link, what u said about the premium and discount is evident. Latest price and Nav are different. Does that mean there are two ways to buy an ETF, from the exchange NSE or from SBI website?

What are the advantages & disadvantages of Index ETFs as compared to Index Mutual Funds?

If I wanted to buy the Nifty Index, is it better to buy something like UTI Nifty Fund or an Index ETF like Reliance Nifty Bees?

One advantage of a Mutual Fund over an ETF is you don’t need worry about liquidity. OTOH, ETFs have the advantage that they don’t need to do transactions every time someone purchases or redeems the fund, so they probably have lesser transactions & transaction cost. What else?

Nifty value 20 is good, but it shouldn’t be your core portfolio. maybe a 10/15% of it.

core portfolio should be broad market indices like nifty 50, nifty next 50.

Seeking this answer too… sorry I did not clarify this earlier.

Seeking this answer too… sorry I did not clarify this earlier.