Even if BKCafe is global, but aren’t they hurrying by opening it too soon. They had to strengthen their legs in India before going for new venture. They are closing BK Stores. Still loss making. In India situation is grim for them. Trying too much too soon IMO.

1 Like

If I remember correctly, its in their franchise agreement to open some predecided numbers of stores within a deadline. Not sure if the agreement was for BK stores only, or with BK Coffee stores included, and whether they have the discretion to delay the opening of stores given the pandemic.

1 Like

Thts the whole issue…target of opening up 750 stores by December 2026…thts means u r not allowing ur operations to stablize…just reckless kind of expansion to chase a target…which will ultimately put pressure on operational costs

4 Likes

Thanks, I didn’t know that.

Non-performance and Relocating, page 4, investor presentation. 5 new added also so maybe they are mainly relocating.

Total 11 closed this year plus 16 new added, 5 closed this Q4.

Nope, plus the trend was also mentioned in Tata consumer report that global shift is towards coffee, especially the millennials.

Does anyone know if planned / operational BK CAFEs have a higher margin ? or its already accounted for in the guidance of 68% GPM which Mgmt mentioned in the Q4 call as a tgt they will be able to achieve in the next fiscal ? I dont think this got discussed …i might have missed if it was …

Cafe’s are margin accretive and no 68% doesn’t include cafe margin

Industry report and initiating coverage

4 Likes

Initiating coverage reports from different research houses

6 Likes

Update

Request other investors or followers of this script to please comment. Otherwise, as per Valuepickr rules I can’t make many consecutive comments.

@Investor_No_1 @Chandragupta @Naveen_sharma and others please ![]()

3 Likes

Can you explain in simple language the holding structure of the company?

This is a surprising news…I do not know much about Indonesian market and how much loss making is BK Indonesia. Also what contracts in place not sure…

Indeed the holding structure is complex. Usually I had decided to avoid complex holding structure companies but here the Indian business is cleanly held by BK India…it’s only when one traces back to parent BK that things get complex…more so when you try to understand that why the promoter of BK India is into a contract with itself where it can penalize itself? (BK parent seems one of promoter of BK India as per holding structure in one of the article)

1 Like

I think not much information is there in this article, so it is difficult to conclude. However, in general I’m quite skeptical of these kind of diversifications. They not only take away resources but also valuable management time and energy which does not get reflected in the financial statements directly. Burger King is nowhere close to saturation in India and so I hope there have a really compelling case to get into this. That said, I was skeptical of the BK Café initiative as well but in the recent concall they have made a decent case for the same.

3 Likes

For details about Burger King Indonesia they have given a link in their announcement made on 27th which has all the details including margin

4 Likes

Some light thrown on this on Q1 FY22 concall, They did not speak about margin guidance but upto 20% of resturant sales can come from cafe . Atleast that is what Industry standard. From managemnet on concall .

add to what Raj mentioned so if you are successful in our café strategy it will drive

incremental ADS it will drive incremental gross margins because café are fundamentally

higher gross margins as a product and because our incremental capex that I was mentioning

is very low, ROI on this are massive means from Burger King restaurant business which has

between 5 and 6 years payback, cafe probably will have a three to six months kind of

payback scenario so across the board it is a great business to kind of being yes, we will have

to go and compete in the market to our sales and that is the effort that all of us are trying to

put in"

From one of the Research House:

Acquisition of BK Indonesia by BK India will be funded through Equity Dilution upto 20%.

Some correction might happen gong ahead

Tracking

1 Like

Although this post is not directly related to Burger King (it’s about Taco Bell), it gives the kind of insight into how the QSR chains are innovating!

Came to know about it through Neil Bahal’s newsletter. So, copying words from there:

Taco Bell has started a ‘Taco Subscription Service’ where customers can pay $10 per month on the Taco Bell APP and get 1 free Taco per day for an entire month.

.

But, why?

.

*Its just weird isnt it?

.

The ‘mini mission’ is to ‘lure’ customers with a free taco and hope they order some add ons and end up spending something extra.

.

But, the real mission starts now: This will help Taco Bell record customer ‘ordering habits’ so they can ‘customize’ deals on a personal level on their APP.

.

*So next time I go to Taco Bell, they will know I like a particular Taco and I could probably expect some deal on those lines.

Another link: Taco Bell's Subscription Service: We've Gone Too Far - The Atlantic

Before Taco Bell came along, all those subscriptions centered on coffee (or in BJ’s case, beer). But some white-tablecloth restaurants have gotten into the subscription game as well. When the pandemic prohibited sit-down dining last year and sent much of the industry’s workforce onto the unemployment rolls, places such as Republic, in Saint Paul, Minnesota, and Gado Gado, in Portland, Oregon, turned to subscriptions as an easy way for cash-flush regulars to help shore up their finances.

2 Likes

Burger King India Ltd – Operating Parameters

(a) Store count

Burger King crossed the number of 200 restaurants in just first five years. The company is aggressively working on its expansion strategy. The company has total 265 stores as on Mar-21 of which 55% are in malls, 35% in high street and 15% are drive thru and transit locations. In FY21 the company opened 16 new stores and closed 11 existing stores. The reason behind closing the store was Non performing stores and reallocation.

Moreover the company has a target to open 700 restaurants in India by Dec 2026.

(b) Presence across India

Burger King India Ltd is present across different cities in the country. The company has wide presence across north and west region. However its peer, Westlife Development does not have much presence in North region. Moreover by CY26 the company has a target to open 300 stores in north, 165 stores in west, 70 stores in east and 165 stores in south.

c) Burger King – Same store sales growth

Same-store sales refers to the difference in revenue generated by a retail chain’s existing outlets over a certain period, compared to an identical period in the past, usually in the previous year.*

The SSSG ( Same store sales growth) of Burger King in 2021 remained at -35%. This is because of effect of Covid-19 and other lockdown restrictions by the Government of India. Moreover the company has 60% of the company’s stores are in North and out of them 55% of them are in Malls. These got effected because of farmers’ protest in Delhi, due to which stores were not opened in weekend and high street roads were also affected in Punjab and Delhi. Thus, this effected the SSSG of some of the stores of the company which in North area. However by FY 2022-23 onwards, it expects SSSG growth at 5-7%

d) Sales Mix

Various restrictions for Dine-in in different states during lockdowns by Government of India had adverse affect on the company sales. Thus the sales mix of the company varied as by the time.

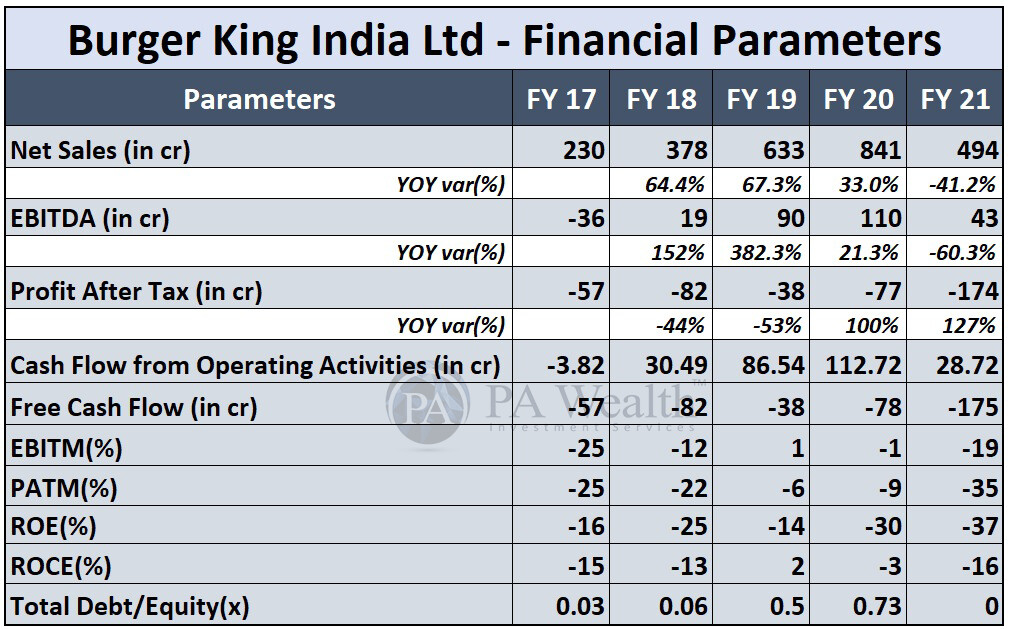

Financial Parameters

The company reported operating profit growth till FY20 but in FY21, the growth of operating profit was negative. Also, the company incurred net loss of 174 crores which was higher than previous year’s net loss. Moreover the interest and depreciation expenses of the company has also been increasing from last five years.

The main reason for Increase in Interest and Depreciation cost is the adoption of Ind AS116. Because of this, operating lease expenses (fixed part) will be replaced by Interest and depreciation cost. Thus, impacting EBITDA, EBIT, PBT and PAT.

Source: PA Wealth

Thanks

5 Likes

Do you think BK is facing head on competition with McD. There might be some product differentiation, but both are competing for the same market.

According to management guidance and current short story, I feel Indian chain is also moving on the same lines. Looks good if the execution is siimilar.