I don’t understand, BK sells is more that of westlife or atleast similar. Number of stores are somewhat similar. But still market cap is less than half of westlife. Depreciation for BK is twice that of westlife which is non cash expense and same will reduce once store mature. Operating margins also not that different.

I think this could be similar story like polycab vs havells if BK delivers consistent results once situation improve. Little premium could be justified but this is huge gap in valuation that exist currently

One major reason for lower valuation is the Indonesia business, which was in all probability imposed on RBA (my understanding) by Burger King (the US entity) and it has been underperforming since the acquisition.

Another factor is the Zomato/ Swiggy/ other online aggregators which have been narrated to be faster growing as compared to the QSR brands. I am not so sure about this in the long run (more than 5 years timeframe- my hunch). But for now, it is eating into the valuations of these QSRs.

I am truly hoping that the business turns PAT positive in the next 2 years, coinciding with the target of 700 stores, which will then potentially result in a Hockey stick growth for a few quarters, especially on the bottom line front!

I have just started to acquire the stocks

Avg price atm is 94 with 5% allocation to the portfolio.

Can add more n take it to 10% if the price fall further more.

Find the company to be at reasonable valuation compared to its peers.

“So we are advertising the Spicy Chicken BIC, which is missing from our menu, which has got a massive following. I think we expect that 50% of our chicken sales, BIC sales, will now be on this product. So we have introduced that product. We have just started marketing that product in all 360 degrees and digital channels, television and so forth. So we put that out there. So that big chunk of work is done. We have cleaned out the portfolio.

We are further looking at tightening up our G&A, which will be in the next 4 weeks. We will be working on further reducing our G&A and our overheads over there. Consolidating the total G&A down to a very minimal number. And then focusing on our restaurants and seeing if there are other restaurants that need to be closed or automized. But we have put a good team in place over there. We had the restaurants all refreshed. All the operations, equipment have been fixed.

The menu has been reorganized.

We have a fantastic CMO over there. Namita, who is doing a fantastic job, putting together a marketing program. She’s put a great menu together; she’s cleaned out menu items. So all that is in place. We’re just waiting for the headwinds to stop and the geopolitical issues to be behind us, and hopefully, some positive macros for us to turn around.”

I had been to Jakarta n Surabaya in June and could come across just 2 KFC outlets - in Kokas n Lulu malls if i recall correctly.

Didnt notice any standalone outlets.

Also there are many street food like outlets for chicken items. While in the malls there are manh Japanese outlets (have presence for a long time) along with America brands as well as upcoming Korean outlets (prefered by the younger gen)

So, the Indonesia biz will take a while to get going.

Yesterday, I was trying to understand this company after the stock prices fell drastically. My mindset was to look for reasons buy this share, thus, I wasn’t completely unbiased. Below are the Big Pictures things I found

Company did the IPO to raise money to open 700 outlets by the end of 2026. Issue price was 60 Rs. Also, if I am not misunderstood, I read that the promoters bought fresh issue at more than 60 Rs, One year prior to the IPO.

The stock doubled on the first day. On that day, the liquidity was suck in by many institutions, which again increased the stock price and it became 3.5 times at one point within the first 5-7 days.

With that, the promoters thought of getting out of the stock and they are still selling whenever they get the chance.

Looking at high valuations, the management did the QIP and raised money at 136 Rs. The stock price then fell.

In the company, the management wanting to expand aggressively to achieve their obligation to their masters(which actually is the promoter entity!!!), burned a lot of cash. And are still burning.

Their strategy is the “Barbel Strategy”. Lure people by value and also sell premium items. Their value pack also has a great Gross Margins apparently. They also started BN cafe to increase product lines and they also have better margins(Someone in the thread mentioned about Starbuck’s report on Coffee as beverage.)

They were, I believe, forced to acquire the Indonesian company by their parent. At one point they are also burning a lot of cash in the Indian market to grow. On the other hand, the Indonesia is also not doing well.

My observation in this thread is that, initially people said “No one goes to Burger King”. Later, said - “People now a days go to Burger King rather than Macdonalds or KFC, as Burger King offer both the foods that these Two guys offer”.

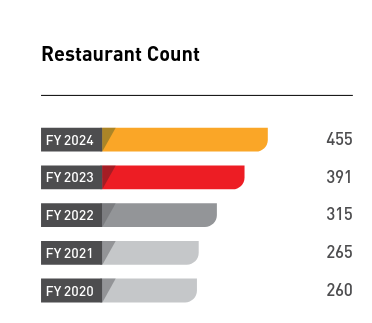

By September, 2024, they have 464 restaurants. And they are setting the target of 500 by this year. Which still requires them to open 200 restaurants within next Two years.

They are doing well technology wise, gross margin wise, SSSG wise and off course Sales growth wise(more restaurants). Still they are losing a lot of money

I might have missed a lot of things here. Let’s see the negatives:

Promoters selling

Loss making

Still a lot of forced expansion left.

Indonesia

Positives:

Lowest sales to market cap. Sale are likely to grow more.

They also have gained popularity for their products.

I have bought very very small amount out of FOMO(And now I tell my self that it’s for tracking purpose), and looking for good reasons to buy significant amount. I see no reason to do that, considering the uncertainty over the next Two years for this stock. I guess that is the reason why it is cheaper. Waiting for people to be more fearful before taking action.

(Just an FYI - Q Int/Sale meaning interest in latest quarter to sales in the latest quarter.)

Talking about other Food Brands:

I also like Barbeque Nation as it is a company owned brand(Not Franchise) which also is a leader Grilled Barbeque. Favoring BN because, it is not bound by their masters and thus can adjust their strategies. Sadly that too is a loss making, but I am optimistic(biased). I own less than 2 percent. In 2 percent profit.

I also own significant Sapphire foods because of (previously) its low valuation(Favorable P/B) compared to Devyani and others in category. (4-6 percent). In somewhat profit here as well.

One more thing that I noticed, and I hope someone can help me understand it better.

In Ahmedabad, in my area, Burger King is at the best location compared to all the other brands. It is also bigger than other Fast food chains.

KFC is a bit far, has Two floors and quite small.

Barbeque Nation is often seen up on the First floor. It’s because - BN is not a Fast food chain.

This could be one area thing. Couldn’t help but mention

Regarding RBA - Today, I am a little less interested to buy than yesterday(2nd November, 2024)

Tracking

Looking for go even further before buying again(this time significant). However, thinking of still holding what I had (out of FOMO) bought.

Let me know where I could be wrong. I would love it!!! Thank You

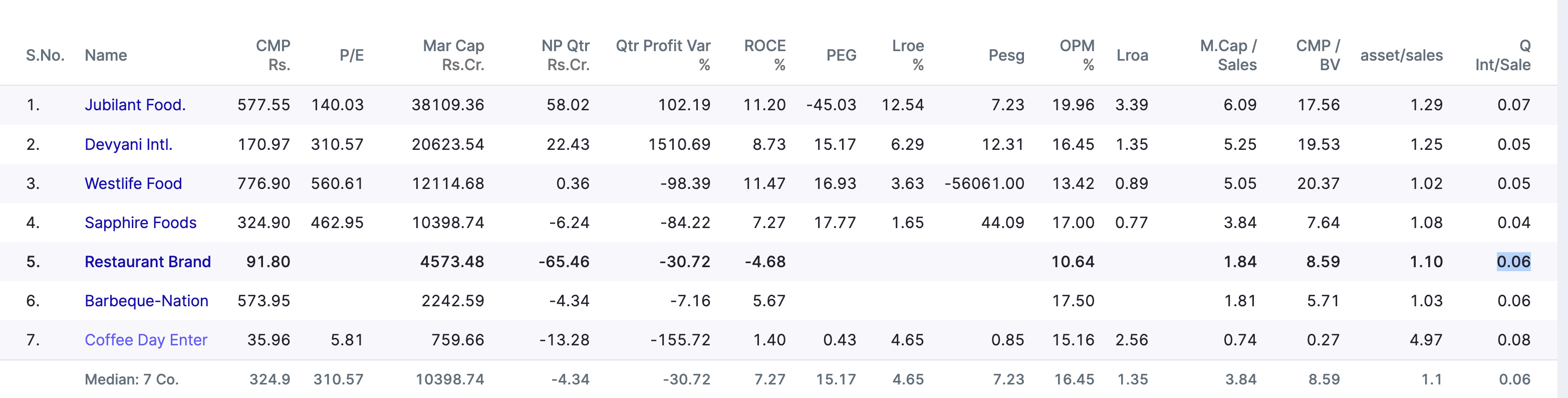

I agee from current quantitative valuation point of view. RBA is winning in every respect. (Can be observed in the Image I attached.)

My concern is more from qualitative perspective. 200 restaurants in 2 years is a huge liability. Plus, Indonesia!! Although, Indonesia wont take 2 years to resolve. Yet, high uncertainty is what I can observe in India alone.

It could work out. But, my fear is from a safety perspective.

Anything can happen in the next Two years. e.g. High QIP flow which it will definitely need. stock prices might remain the same, yet market cap would go up!!!

You mentioned operating cash flow. There are about the same number of stores of RBA as Sapphire. Thus, they generate same cash flows. RBA is burning cash intensely to do that right now. If you checkout cash reserves, RBA’s reducing quite drastically. In September too, it increased by borrowing. Its commitment requires it to burn further money.

My estimate is, it will do a QIP, people would panic. I might be wrong.

Disc. Invested insignificant amount. Terrified to buy at this price, waiting for further correction(Could take eternity), or change of circumstances.

We are getting these valuations cuz of uncertainty only.

I think in the next 10 years time frame RBA will do better than other QSR in stock price CAGR

My rational: with per capita income increasing(with 7% we will double in 10 years)

QSR sale will go up n RBA will benefit.

At current valuation we get better margin of safety compared to other QSR.

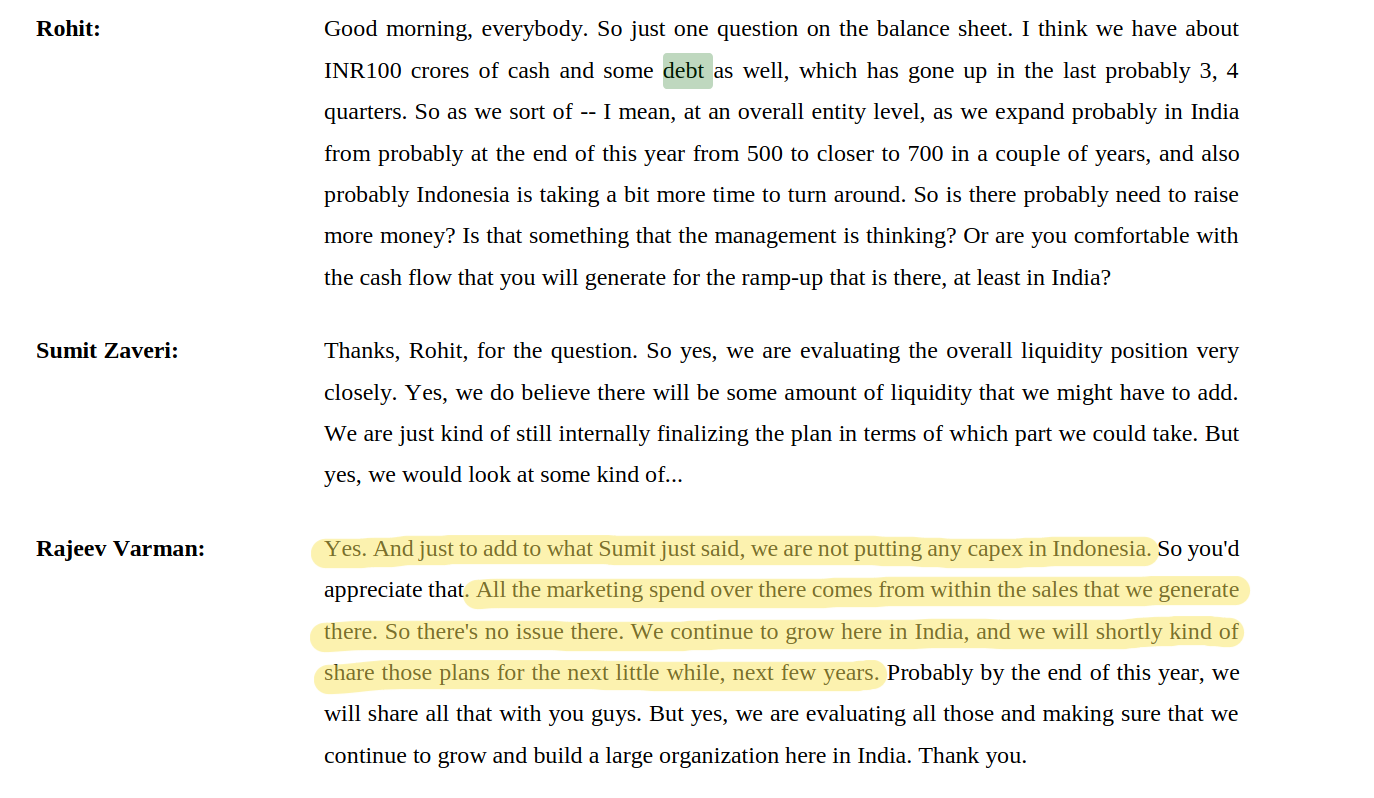

Debt wise in the con-cal they said they will update in the coming quarters regarding how they will raise money.

With 700 restaurants after 2 years they will try n get profitable next.

I think it a bet worth taking n if u do want to bet on this QSR thing RBA at current value is a good buy

Ps- i have a lot to say but im not very good at expressing myself

Regarding Indonesia side they have stop opening new restaurants there till situation improves (they said they can do 15% ebita over there)

Lets hope in the next few quarters they do

Restaurant Brands Asia (RBA), which operates the Burger King brand in India, faces some challenges in maintaining a strong, competitive position within the Indian fast-food market. Based on my experiences as a regular customer of both Burger King and McDonald’s in Mumbai, there are evident discrepancies in the ambiance and customer service provided by Burger King. Over several visits, I observed that Burger King outlets often keep their air conditioning off, even during peak summer, citing “repair work” as the reason. Additionally, the staffing is noticeably limited, which affects service quality and speed, further detracting from the customer experience. In contrast, McDonald’s consistently offers a pleasant atmosphere and attentive service, suggesting that they prioritize customer comfort and a welcoming environment. Burger King’s approach to cost-cutting by reducing essential aspects of customer service, such as air conditioning and staffing, may harm its brand image, risking a downgrade in consumer perception. This approach could lead Burger King to be seen as less of a premium fast-food option and more comparable to local, lower-cost eateries. Additionally, Burger King’s strategy of opening outlets near McDonald’s locations in hopes of sharing foot traffic does not seem sufficient to build a strong brand identity. Without significant product differentiation, customers might regard Burger King as merely a follower rather than a distinct option. While RBA may benefit in the short term from cost reductions, the long-term risks include eroded brand value, dwindling customer loyalty, and stagnated growth. If Burger King continues without improvements in service quality and distinct brand positioning, it risks losing its edge and, potentially, its market share in India’s highly competitive fast-food industry.

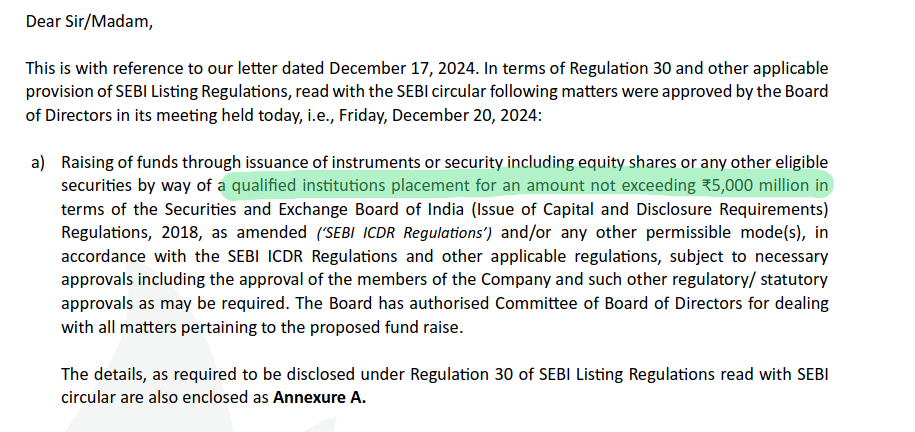

Is the 500cr QIP primarily for India expansion or for Indonesia? My fear is money will need to be diverted to Indonesia as well.

In less than 5 years, this is the 3rd time they are raising equity now. This shows the high capex intensity of business.

No real pricing power with QSRs, and I don’t really see this as a business with very high operating leverage.

See the major cost heads below GMs - Rents (will have variable rents for most attractive locations), Continued increase in minimum wages, Swiggy/Zomato are big revenue sources and their commissions are variable, Royalty - 5% variable, A&P - 5%

Some room for op leverage on Corporate expenses.

Attraction here is only because of high valuations of McD and Jubilant (for Jubilant it’s due to superb execution by Dominoes in India) - not everyone should or will get same multiple.

As per the management commentary, looks like the bulk money that be being raised will be for India only. Also we need to see that BK is the expansion mode and they are planning to add +200 stores in next 3 years of time. Total 700 stores by Dec-2027.

In Q2FY25 concall, management stated that they are not going to invest in Indonesia (atleast I feel the bulk of capital will be deployed in India only).

Consumer slowdown and Indonesia business hurting them. Also the fact that they need to now aggressively open new stores i.e. 70 stores a year to reach 700 store target by eoy 2027 will play a role in results for foreseeable future

Things that seem to be in favour

Pan India franchise so TAM is much larger compared to westlife. Include indonesia and whenever the turnaround happens it will be an added advantage. Popeye probably could be a game changer in Indonesia.

Cheap valuation vis a vis other comparitive franchise. Especially around value to sales ratios

Revenue will continue to grow due to aggresive store addition

Consumer spending being cyclical will eventually rebound and with store addition significant operating leverage can happen

So I think once the current pain is withstood there could be significant gains that might get realised once all factors start playing a role.

Part that I am not getting my head around is the ownership and with owners reducing stake am little unsure on how the company would run or will it lead to significant inefficiencies. I guess time will tell.

The whole premise of investing in burger king India (now restaurants Brand Asia) was based upon unique value for money offering from an Internationally famous brand. However since 2020-2021( post covid) the QSR lanscape has drastically changed and every small town tom,dick and harry is opening Burger/ Sub offering with little or no price difference and little quality checks. Also some of them are offering franchises at such rapid rate and geographical proximity that it will make profitability difficult for Burger King. I am invested since the IPO listing at 110, for more than 3 years now and would most probably exit at loss in this financial year. Case in point is Jumbo king–there are 4 outlets of Jumbo king in Kasmiri Gate metro station itself. I am attaching photographs of a single lane in the metro station where there are more than 10-12 QSR outlets offering burgers only between 39-49. The rent at this place is very high and still these outlets are opening every month. All in all I see no profitablity for Burger king in near future. Please pardon me for using this, as aditya puri used to say" baki sab to theek hai par ladoo(cash profit) kahan hai??. Costly lesson I learnt the hard way.

Its true that the local competition is coming with many startups emerging in this space. The emergence of online aggregators - Zomato and Swiggy has also helped these players to reach the customers easily. But one important factor that we need to consider is scalability. RBA with ~500 stores is still struggling to make profits at P&L level. I doubt these small companies with less numbers of stores making any money for the next couple of years. RBA is 10+ years now in India. Hope if you have any numbers wrt Jumbo King / Burger Singh - will be help to understand more.

Below are the pics from few QSR brands taken from Lulu mall Bengaluru in October (on Sunday :))

Also found a recent video of Samir Arora where is talks about the franchise players like WestLife (But he was more interested new age businesses like Zomato and Swiggy)

Please check from 23:30

I happened to visit a Burger King few months back. When I checked with staff about store timings - I was told they open from 8:30AM to 1 AM and online delivery runs till 5AM.

Do all the other QSRs follow similar store timings ?

I feel most of the stores closes by 11PM and only stores at prime locations may operate till 1 AM. Below snapshot from the website of RBA.