base formation in minda corp…

disclaimer… will plan trade on breakout and phase d entry on lps formation

base formation in minda corp…

disclaimer… will plan trade on breakout and phase d entry on lps formation

Bro consolidated loss is 1800 crore…also their standalone business has done well in Q1

It’s 1902.37cr loss attributable to the shareholders, not 1800cr. From which EPS is calculated (5.60)

3532cr, which I mentioned is Total Comprehensive Loss. I overlooked twice while posting the numbers last time. Should have read 1902cr.

continuation post…

bajaj corp supply absorption ongoing at last point of support

volume candle chart

disclaimer… invested and accumulating

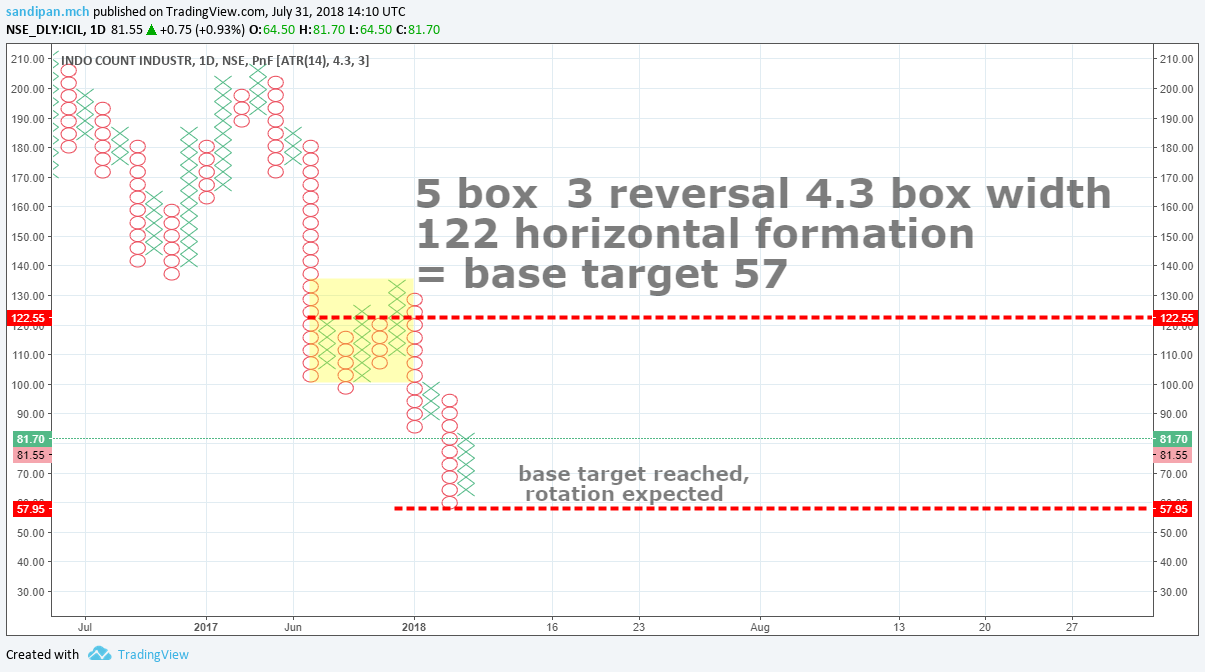

As of now, ICIL is following the chart. Seems like consolidating in the 80s (waiting for the next signal, the result… which will be announced on 3-Aug), would continue the upward move if the result is positive.

Also, if I’m not wrong, the 8 waves are done and the impulsive cycle is beginning. Pls correct me if wrong (I’m bit unsure about fitting the 1,2,3,4 waves as wave 1 & 4 are overlapping a little, but not more than 5%).

i have been tracking this since @PE_Ratio mentioned about it

and it does seem to be forming a base now…

@manivannan.g

this is the last redistribution , and the point and figure chart indicate a rotation up

78.6% retratecemnt of wave 3 and at the 100 month wilder moving avg seems to be some kind of terminal support from the price

disclaimer… no current position, tracking…

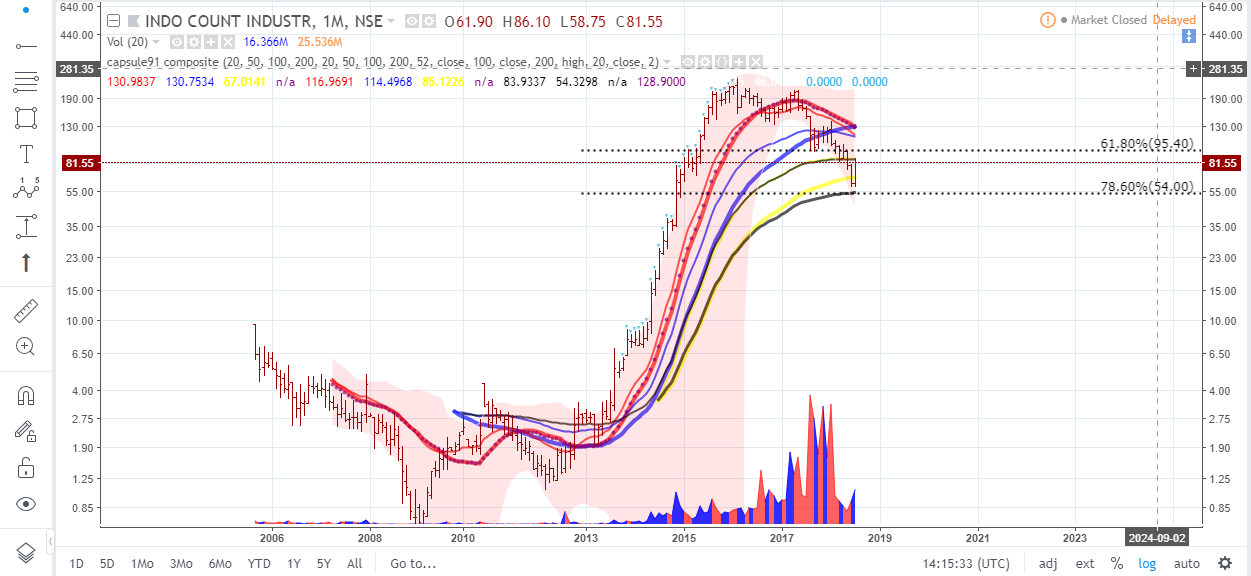

Nice !! I’m waiting for the result, if the margins are flat then the cyclical has hit the bottom and we definitely should see trend reversal. If the margins are at still bad, then the bottom is bit nearer. The reason is we had good Southwest monsoon and northeast monsoon will arrive later this year. So definitely the cotton prices would come down, so the margins will improve. For me ICIL management is better at corp governance than other textile cos like welspun, kitex etc.,

This is definitely interesting, waiting for the result to make a call.

Auto Corporation of Goa -

Made these charts few months ago.

Zooming in the above chart.

This pattern worked out pretty well. Predicted that it would go down to 725. But it bounced from 760. That may be the bottom. If not, there may be one last leg of correction that would take it to 725/700 level and bounce.

ACGL is jointly promoted by Tata Motors. This stock came into focus when Electric Vehicles came into focus. ACGL manufactures the body for EVs. ACGL is part of Tata Motors electric bus and hybrid bus programme.

Chaman lal setia might have a bounce back, but expected to correct to 60. Not sure how correct is this. Pls have a look.

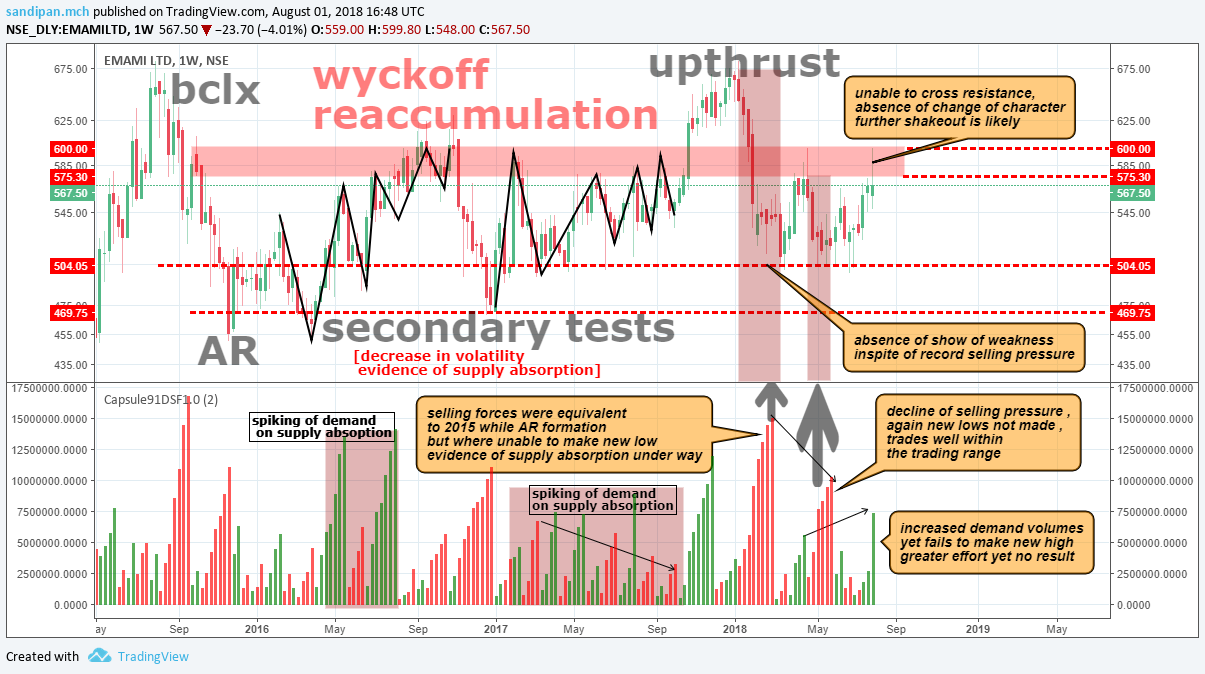

mahanagar gas confirms selling climax…

well, i have a different stance on this and i feel there is accumulation going on here…

and this is primary wave 2 of cycle wave 5, which has retraced to 88.6% level almost, thats pretty deep…

let me know ur views…

disclaimer… no positions, not tracking

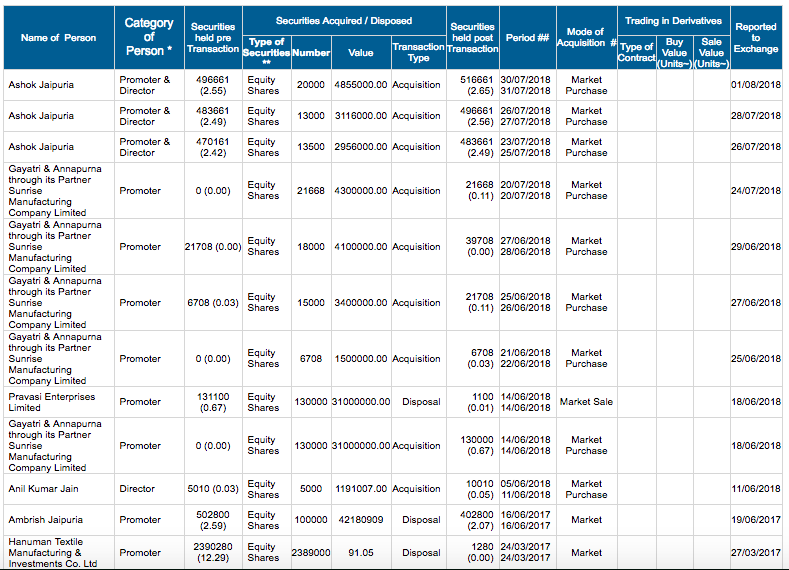

Cosmofilms is the second cyclical stock which I’m tracking next to ICIL. Cosmofilms margins were under pressure for a long time, this seems to be hitting the bottom. Just in time, promoters started buying (bought around Rs.5.64Crs worth shares), may be good indication that things are gonna improve.

SAST:

Shouldn’t we consider the retracement from (B), instead of second wave next to 5 ? I mean, the B->C should be 61.8%, 78.6%, 88.6% Fibs right ? I’m just beginner, trying to learn the elliot wave ![]() pardon the ignorance.

pardon the ignorance.

2 cases of excellent accumulation worth tracking…

emami and greaves cotton…

both i believe are at the exact same position in their accumulation phase, which is the phase d

the ultimate phase of the schematics…

and both faces the same challenge in their trading range…

none have shown the ultimate breakout change of character…

I track the fundamentals of greaves cotton,

management discussed Greaves 2.0 strategy, a 5 year plan to de-risk engine business by becoming fuel agnostic and reduce the share of engine business to 40% in overall revenue by growing aftermarket and other segments. In an effort to de-risk engine portfolio, Greaves is transforming itself into a fuel agnostic player. For this, Greaves has partnered with Pinnacle Engines of US for launch of CNG & Petrol variants and for Hybrid and Electric variants it has partnered with Altigreen Technologies of Bangalore.

Greaves has indicated that technology demo for Hybrid and Electric variants are

complete and further evolving of specs for the final phase of development is under

progress.

With Pinnacle it is planning to launch two engines one for 2 wheelers with

range between 110-115 cc and for 3 wheeler Greaves is planning to launch product

in the range of 200-240 cc which it believes would take about 2-3 years to bring it to

mass production level.

Greaves has signed with major OEMs for BSVI diesel 3W engine which is coming to

force from April 1, 2020.

the company launched two new powertrain solutions at the Auto Expo 2018 one of which

is a new family to multi-cylinder turbo-charged intercooled engines which are BSVI compliant and a lithium ion battery based ev powertrain for 3 wheeler

Engine business accounts for 51% of revenue,

Aftermarket accounts for 25% and rest all account for 24%.

.Auxiliary Power segment market share has increased

from 3.5% to 6.5% and has increased the range from 500KvA to 1250KvA.

In the farm equipment segment it has 45% market share in the Petrol/Kerosene pumps

and is planning for electric & solar pumps in near future.

Aftermarket accounts for 25% of revenues and the

portfolio can address 80% of 3W ecosystem with Greaves own parts and multi

brand spare parts as well. Greaves Care an asset-light service model aimed at

addressing complete service needs 3W & 4W. Currently 51 outlets are functional

and Greaves is planning to launch the service across India in a phased manner.

Management quantified the annual opportunity size for this segment at ~Rs. 25 bn.

AS of FY18, greaves has EBITDA margin of 14.2% , PAT margin of 11.3% , long term debt free, ROE-21.4% and RocE-18% , 916cr reserves and surplus, 238.4cr operating cash flow , and present market cap of 3571cr…

attached here the lastest investor ppt

the biggest concern to me is , any upgrade by customers to 4W LCVs might disrupt 3W LCV volumes which is the stronghold of GCL.

disclaimer… no position, tracking

@manivannan.g

i guess no, this correction should find support within the length of the previous impulse right?

so u draw the retracement level along the length of the impulse wave only…

that gives u one support…

another rule of thumb is generally a=b[most commonly] or 1.27A=B or 1.618A=B and so on in the fibonacci series [in percentage terms]…

that gives u another level of support…

but by far the best way is to count the internal waves of c and see where it can lead to, this is a corrective wave 3 , so it sud be a 5 wave structure down…

i guess 5 waves are done already of c…

Continuation post…

beautiful back up action in the phase d of wyckoff reaccumaultion…

dislcaimer… trading position

Philip carbon black…

wyckoff reaccumualtion…

well this is a discovered story already…

so whats new…

i think 3 things which can make the market give a little bit more valuations to the company

are…

1.improving revenue mix wherein the specialty carbon black has been steadily increasing, with better margins than the commodity …

2.raw material prices a pass through to the customers plus price hike done for the tyre industry

3.capacity expansion- a.brownfield- expanding its Mundra capacity by 56k

tonnes by Q3FY19 and increasing specialty carbon black capacity at Palej

plant by 32k tonnes by Q2FY20[ the 32k tonnes expansion of specialty carbon black is likely to come online in 2 phases with the first line of 12,000 MT to come online by end of Q4FY19 and another line of 20,000 MT to come online by Q2FY20]

Also the company incremented its capacity by 43k tonnes by debottlenecking exercise which has been completed already in fy18.

Now, this incremental capacity[43+56+32KT] has a higher share of speciality grade CB lines (44 KT out of 127KT) with overall share of speciality grade CB increasing from 4% in

FY18 to ~8% in FY20. Speciality grade carbon black EBITDA margins are to the tune of ~4-5x normal grade CB that will aid improvement in EBITDA margin and structural uptick in earnings, going forward.

capex for brownfield expansion- 450cr

b.greenfield- 1.5lakh tonnes pA is planned , for which land acquisition location is yet tobe finalized… no time line mentioned on this, and a estimated capex of 600cr for this …

talking with yoy Q1 numbers, 26.4% inflation of expenditure , 1% volume growth , 33% sales growth , 68% ebitda growth and improvement of ebitda margin to 21.2% by 439bps, PAT growth was at 102%…

everything was a compounded effect of better margin revenue mix, pass through of raw material prices to the customer and additional annual price hike , and ofcourse incremental demand form the indian tyre industry , after imposition of anti dumping duty on tyres …

the demand grown continues to be at the same pace in india and globally and is expected to grow at a rate of 8.3cagr annually [globally] …

what adds pricing power to this segment of the industry is the fact that, the chinese are losing their cost controlled production edge…Majority of chinese manufacturers use the carbon black oil route to manufacture carbon black and reduction in chinese steel production has led to shortage of Coal Tar which used to derive CBO, thereby increasing CBO prices…

in case of the already high margin nature of the speciality CB, the growth is expected to be accelerated from 2.7% to 3.5% over the next few years, mainly headed by plastic industry consumption…

domestic and global demand supply gap is intact and imo is going to be widened till 2020…

No new capacity expansion of any other CB players i noted at the moment…

hence i believe, the company is poised for the next leg of growth in fy20 , and a wyckoff reaccuualtion in fy19 makes a lot of sense in the charts…

disclaimer… not invested, yet, tracking, waiting for a phase c change of character of a final shakeout if conducted, to enter…