Axiscades, Monthly - After a runup in Jan '24 which was undone in Feb '24, it spent the rest of the year wallowing between 500-650. So this upper end of the range (650) is strong resistance. A breakout above this level should help hit ATH

Fundamentally the company is into Defence, Aerospace, ER&D (Auto), Heavy Engineering, Semi-conductor and Energy verticals. Auto ER&D is currently a drag due to Volkswagen not doing well as we all know. Heavy Engineering (partnership with Caterpillar) is a low margin business so both ER&D and Heavy Engineering are somewhat of a drag currently on overall performance of the company.

What excites me is the Defence vertical under Mistral and ACAT. This is where the company is guiding for high growth and restructuring and synergies. The semi-conductor business as well under the C2P (Chip-to-product) approach can show good growth going forward.

The company held a call to discuss restructuriung the defence vertical and also discuss prospects of defence, aerospace and semi-con. I think the first 12 pages of this transcript are worth several re-reads to understand what is being planned under the mentorship of Dr.SRN. There’s a lot of management shake-up as well at the top and there’s lot of intension and hunger to do well (Very similar to what Ceinsys went through last 2 years).

Key highlights

-

The company has a large foothold in anti-drone warfare having supplied 100+ of these systems. There’s value-add to these systems to make them portable, vehicle-mounted etc. This could be a big driver for the company going forward. Additionally, spoofers, directed energy weapons, RF detectors and 3D radars are also being planned which can be a huge value-add for the company.

-

They also have a good presence in defence logistics (30-80 kg payloads using drones)

-

Capability in drone controller which is used in an American company already (plans to get it NATO certified). It can sell this across the world to various OEMs

-

Preferred offset partner for weapons package for new Marine Rafale. OEMs are higher margin so company is focusing on weapon package, submarine and avionics to sell to OEMs. Already has foothold in 1 company and is trying to engage two more for these.

-

Missile capability in new missile program post Russia and Israel war. They are also participating in upgradation of existing missile systems.

-

Focus on products - Direction finder, direct RF (eliminates few stages in radar signal processing making equipment light-weight), X band radar used in submarine and marine systems

-

Expand foothold with Airbus programs running in India - like MRTT

-

Space - in launch vehicles in partnership with AgniKul (NGLV and Bharatiya Space Station)

-

Semi-conductor C2P - Chip-to-product strategy across 6 verticals - defence and aerospace (drone controllers), automotive (autonomous driving), healthcare (protein synthesizer), consumer (product to teach age 5+ kids using AI), industrial and hyperscalers

The company has 5000 Cr of approved design wins which can go into production. Bulk of these (~60%) is for LCA Tejas (130) and Sukhoi (250) aircraft programs which are currently delayed. While these play out perhaps in FY27, there’s still enough in the pipeline for Anti-drone systems, new missile program, Akash Mark-II and QRSAM meanwhile which will contribute in the near-term.

There’s definitely lot of technical capability across the company and it seems to be keyed into the direction MoD is going in with AI and IOBT (Internet of Battle Things), swarm drones etc.

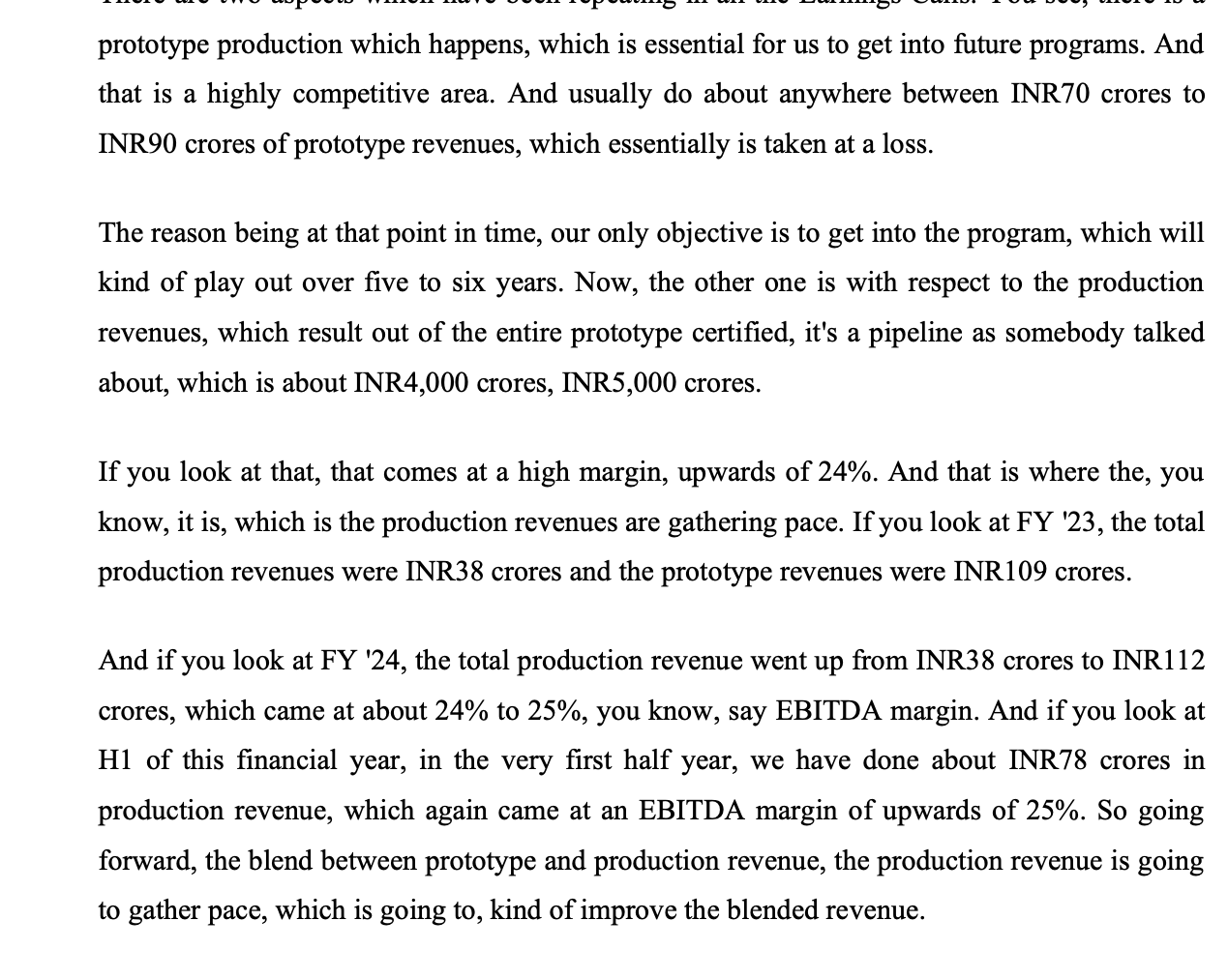

Margins will trend up because the contribution from production revenues will trend up here on. The prototypes are barely breakeven or loss-making as its very competetive but production margins can be 25%

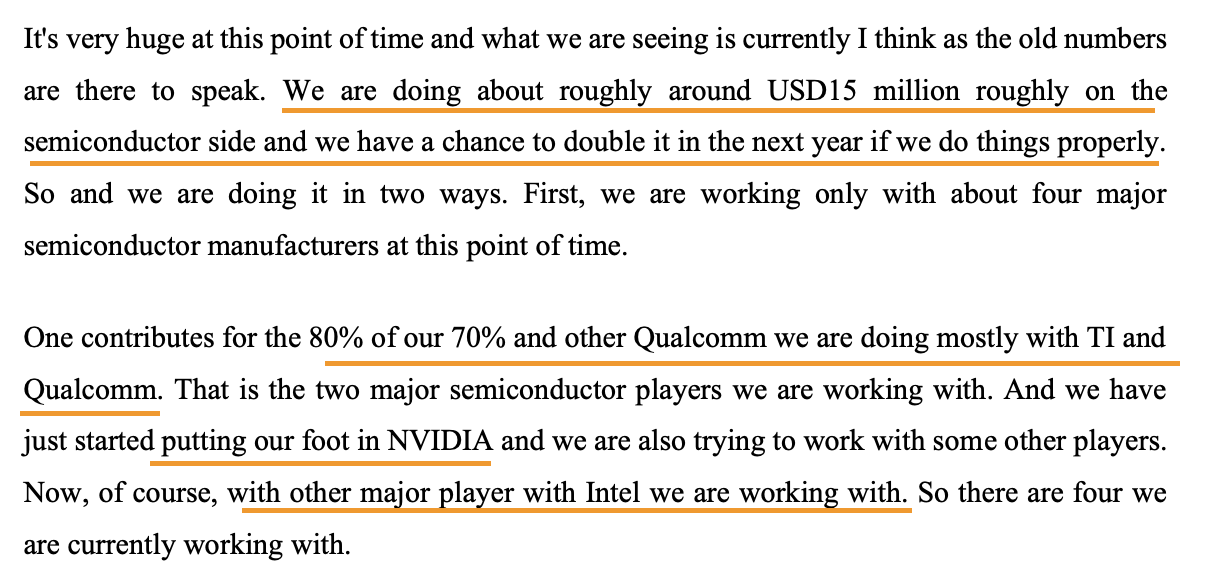

On the semi-con business - they currently work with TI, Qualcomm, Nvidia and Intel (this business is based out of US currently but some part of work will be done in India going forward)

Interest cost in FY '24 was 58 Cr. This will reduce to 20-30 Cr.

So overall for this level of capability, 2500 Cr market cap seems cheap though P/E basis it looks expensive. Profitability should continue to trend up from here.

Risks

- Auto ER&D will continue to be a drag this year

- Execution risk with so much management overhaul

- Capex and WC requirement might be high for fulfilling all these aspirations

- Politically connected promoter (Rajeev Chandrashekar’s PE firm owns bulk of the company)

Disc: Have positions between 620-650

Credits to @rupeshtatiya thread on Axiscades and to @nirvana_laha and @Sanjay_Kumar_E for helping me in understanding the story better