Garware Hi-Tech Films, Monthly - Looks all set to take out highs made in '21.

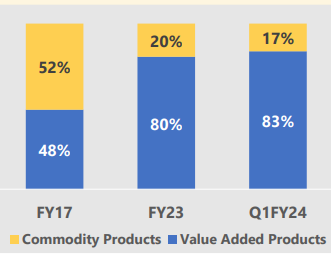

Fundamentally, this is a different business from the one that existed pre FY18 or so. The contribution from speciality films (Sun control in automotive and architectural, Paint protection and Shrink films) has increased consistently and as of Q1 is at 83%.

Market is still valuing this like it is a commodity packaging film manufacturer while a large portion now is speciality, margins are much higher at ~17% even in low cycle for the commodity business

There is significant growth prospects in the PPF segment with a total revenue contribution upto 400-450 Cr per year on full utilisation. As of current quarter, there is guidance for this line to be fully utilised from a utilisation of just 50% in FY23. So we can probably expect 100 Cr from PPF in Q2 which is phenomenal

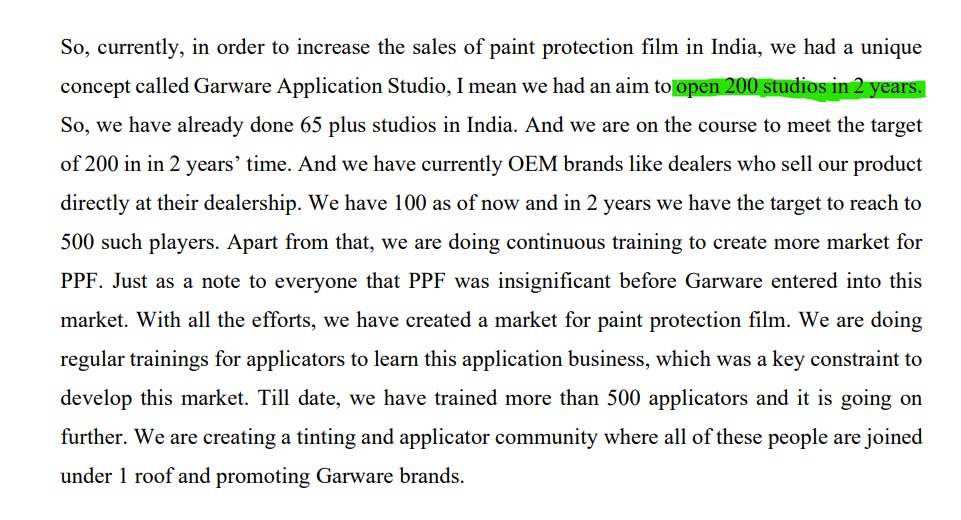

The company is also making a foray into B2C segment for its PPF films opening Garware Application Studios. Increasing awareness for the product and vfm pricing could help them do in PPF what they have done in sunfilms in the past in the Indian market

They are not however fully backward integrated for PPF like they are with SPF and seem to be buying certain things like self-healing films from XPEL.

Company aims for a 2000-2500 Cr topline with its installed capacity. I think there could be significant operating leverage and any turn in commodity business could add to the EBITDA margins and I believe it can go up above 20% when utilisation is full and cycle is in favour, earning an EBITDA of about 400-500 Cr in the next couple of years, which would be a double of earnings from current levels. There is also plan to sell Nashik land which could bring in 80-90 Cr.

I also believe this company can rerate considerably, considering its just at 14x P/E. The 15-20% earnings growth, coupled with an expansion of P/E to a 20-25x levels can probably make this a 3x from here

Risks:

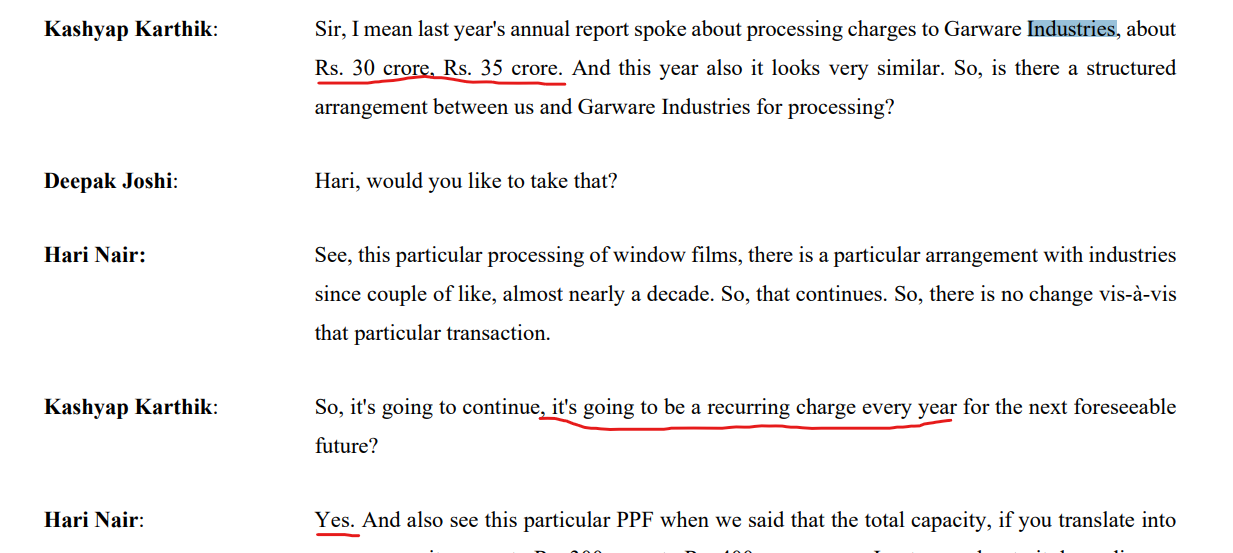

- There is a processing charge of 35 Cr paid out to Garware Industries every year which has been a thorny issue, along with other corp. gov. issues

In today’s call again this issue came up (50 Cr this year). Management says this is for some dyeing process that only two companies in the world do and this charge is lower than market rate. They will consider merging the company in the future perhaps

- Company very likely does contract manufacturing which contributes 30% of PPF revenues while 70% is brand driven. How they deal with conflict of interest remains to be seen

Disc: Invested from 1000 levels