Sri Kalahasthi Pipes, Monthly - Broke out of monthly close trendline last month but still at resistance levels around 200. Business announced flat EBITDA numbers YoY today (with ~20% topline growth and ~20% bottomline decline). There isn’t much in the price since its trading at around ~4x times EV/EBITDA and a discount to book value (about 2/3rd of book value). Market Cap currently is at 900 Cr.

This discount probably made sense as of last year when it had a large portion of its assets in Account Receivables (541 Cr as of March '20 but down to 225 Cr as of March '21 as of recent balance sheet). The CFO reported is a whopping 549 Cr as a consequence of the working capital changes which isn’t bad for something trading at 900 Cr Market cap. With 520 Cr cash on the books (cash + bank balances + current investments), it perhaps shouldn’t trade at a big discount to book value anymore. The company has paid consistent dividend of about 30 Cr last 3 years and so is trading at about 3.5% div yield.

Disc: Have a position around 190 levels

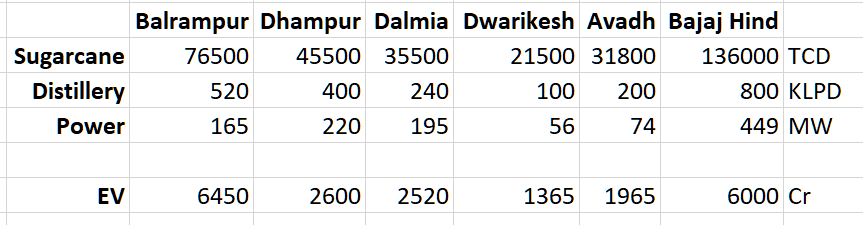

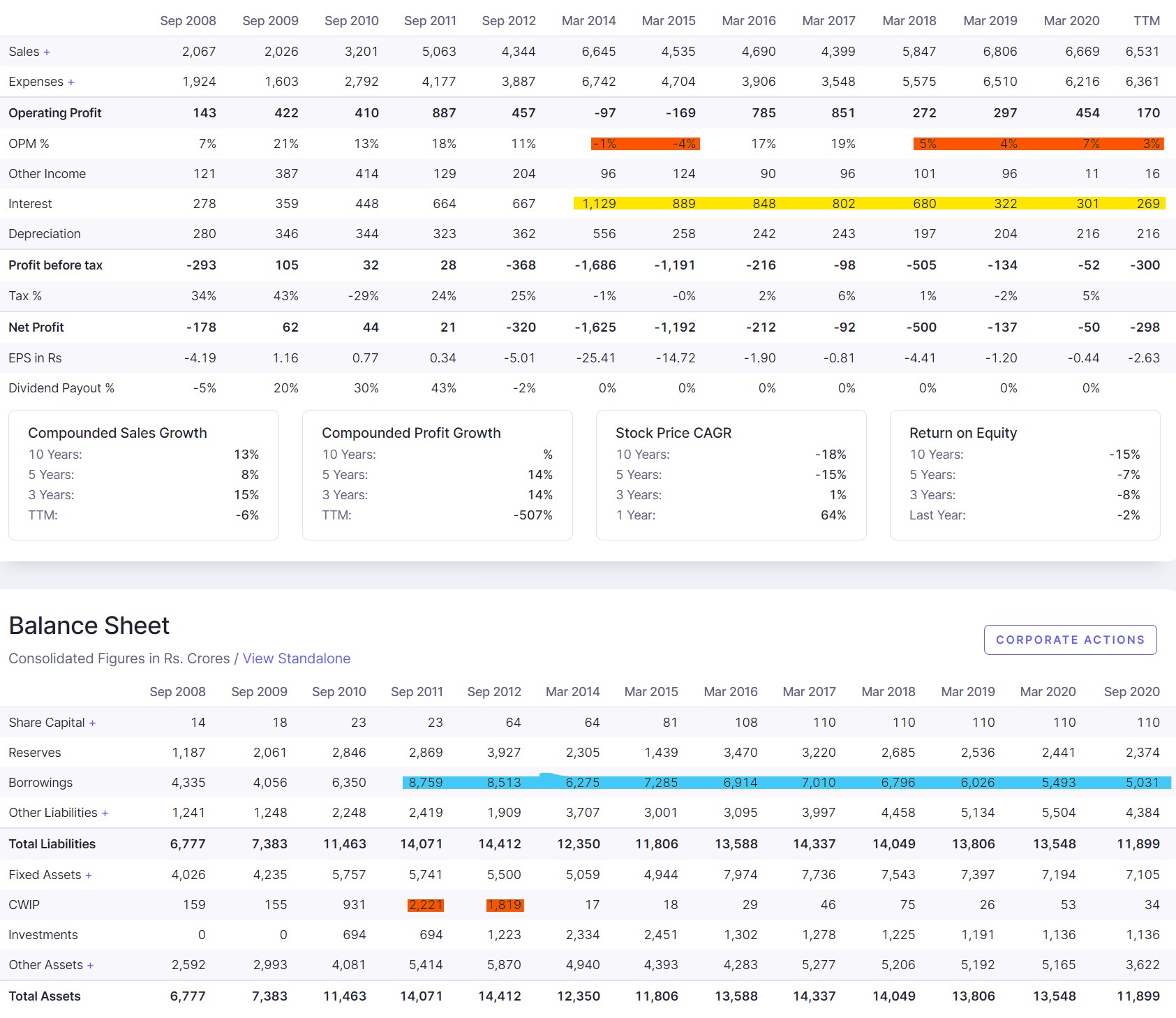

Bajaj Hindustan, Monthly - If Sugar is a bad sector, this is probably the worst stock in the sector. It has the highest debt levels and has taken a massive beating by the market for years. Promoter holding is only 15% and the entire thing is pledged. Most of the public holding is with banks which probably lent it money at some point and are now holding the bag (40% SHP with banks & financial institutions and can be assumed to be sort-of promoter holding). So needless to say, this is very high risk-high reward trade (so position sizing should be appropriate, if at all it looks interesting). It has broken out of a 6 year downtrend few months back and is now showing some life along with the rest of the sector. Today has seen lifetime high volumes and a reasonable 40% delivery (which is good for the volumes)

Valuation is what is even making this trade worth taking for me. From a replacement cost perspective, compared to its peers, it is trading somewhere around 30-50% discount. But this is normal when survival itself is in question and one look at the PnL will tell you this is a horrible business to own.

The PnL has taken a big hit from Interest cost + Depreciation ever since they have undertaken that large capex in FY11-FY12 and has suffered for almost 10 years now for that sin.

However, the silver-lining if there is any is that the debt and consequently the interest cost has gone down over the last few years. Now the Interest Cost + Depreciation is around 500 Cr. EBITDA levels like FY16 in the previous sugar cycle of 750 Cr hence can this time turn into a 250 Cr profit. And a business that is wallowing in debt and poor perception like this stands to gain the most from a cyclical turnaround than the others.

Tata Steel BSL is a classic recent example which played out well for me when the steel cycle turned (If only it wasn’t going to be merged with Tata Steel, the runup would have been even more dramatic with the turnaround).

Disc: Have a position around 9 levels