If you have horizon of 2/3 years … This is right time to lock funds in long term Gilt funds ( > 10 years duration ) . The default risk is zero as they are Govt securities plus any future interest rate reduction will enhance your returns … 3 years will mean you will get indexation benefits

In debt funds for few extra % one should not take credit risk … It is better to be in Govt Securities

What does this mean - “if somebody bought a zero-coupon 30-year bond in 1981 and rolled in each year to another 30-year zero-coupon bond…”? I don’t quite follow the implications/how that works. Can you kindly explain? Thanks!

I suppose during the 80s interest rates were high in the US. Paul Volcker had jacked up rates to crush inflation, so if you bought bonds at that time, you could have made a killing.

Lets look at History – No body can predict what will happen next … Even Fed thought they might not be required to increase rates till 2023 , but in 2022 they already have increased rates in excess of 4% …

Yet history tell us something …

Interest rates have cycles .that last between 22 and 27 years … We have one long cycle when interest rates from 1982 dropped from 20% odd to near zero in 2020 /21 … This cycle has been longer than usual …

Are we entering a new interest rate cycle … If that happen we are are new regime … All recent bias of equity returns and bonds returns will have to be thrown into garbage and one need to observe what does new IR cycle mean …

First Lets try to understand why we had long interest down cycle … or low inflation from 1980s

Globalisation + Cheap manufacturing & service outsourcing to Asia driving down inflation …

Discovery of Shale gas - lowering energy cost for US and balancing OPEC power

Fall of Soviet Union thereby reducing overall cost to implement favourable policy for US …

Productivity driven initially by technology - computers , telecom and internet -

Adverse Demographics in Europe and Japan – which balanced high growth of Asia …

What is happening today ??

While 4 and 5 is still going strong … 1,2 and 3 points have turned for worse … so it is no longer one way street … Added to this post COVID … people work life balance priorities have changed leading to even smaller pool of labour force across world …

Hence zero interest might not return in a hurry … that means higher discount rates and lower multiples for equity earning and higher bond yields possibly ( also real yields to counter inflation expectations ) . Additionally this raises cost of capital and IRR threshold for project and lot of low returning projects may never see light of day - leading to lower revenue and earning growth

If this interest regime last for > 10 years then we may see possibly an even a decade of zero or low equity returns .

Equity return expectation has to be reset and asset allocation to other asset class need to be balanced …

Economics is not science, more so the economics that exists in the context of human behavior. So while I admit that I have zero knowledge about the things you have said, except for a vague, broad, basic understanding, I am of the opinion that the world we live in is not the world of 1982. Reagan’s era is gone, even Obama’s is gone.

I have no crystal ball to make any kind of forecast, I am of the opinion that what has happened, has happened in a different world, in a different society. India was Roti, Kapda, Makaan then, not anymore, we have Unicorns. We are consumers, be it content to the mind or an experience of a lifetime. So I think, to this extent, things may have changed.

While greed and ignorance will always exist in any century, some level of understanding is also happening, not a match to blind greed but some educated people are taking informed decisions, although these are less in number. So while doubling money in 6 months has vanished, 20% CAGR is gone, I think the participation to some extent is likely to continue.

Also, investors are from different age groups, an retired person who is drawing a pension has a different outlook compared to a young man who is in the stage of accumulation, so to this extent, I guess even market is subjective.

I for one have no rigid framework per se, so I also incorporate market’s movement in my decisions.

Good perspective, thanks. While I agree with you that the world of zero/low interest is not returning in a hurry, unlike in the US, I don’t think it will change equity returns in India so much. We seem to be at a stage when the flows to markets from domestic investors (retail and institutional) will only increase over the next decade, even if the pace of increase slows. Given that, equity returns should still continue to be strong even in a relatively high interest rate scenario. Of course, there will be ups and downs.

To me, it seems that the real risks for equity returns in India are geopolitical shocks (say, a war with China) and economic mismanagement leading to both economic and social problems (increasingly, a possibility).

The same can be said that 1920s was not same as 1850s or 1880s … etc …

200 year history tell us something … what it says this interest rate cycle exist and the can be pretty long one … so one needs to prepare asset allocation accordingly …

I am not saying Indian business will do very badly , what I am saying that as interest rate goes up … discount rates change – leading to PE derating …

As bond yields become attractive and equity returns remain flat or negative like it has been for last 15 months at index level … equity will start losing interest or get less priority …

I am not in any position to support or discard any economic thesis, recessions or depressions, I am an outsider to economics. There are a lot of moving parts that are beyond the scope of even economists, so retail young investors cannot get benefited by such events, perhaps choosing to invest in a staggered manner, as a fall can occur slowly. I do admit that such deep and broad economic historical events help in creating a perspective.

One cannot take these things for granted, I know that. One signature on a piece of paper can turn the fates, one word against the public consensus can create a panic. And we live in a very interconnected world, not just the economies, behaviors are also bundled together, so I am aware of the impact.

Also, it certainly helps to have experienced people in the forum, so thank you for posting all this.

Well thanks for sharing this interesting piece of graph on interest rates spanning 2 centuries. In the history of United states, one of worst period for equities (and industry) has been 1929-1941 Great depression period…when GDP fell by nearly 15% as compared to less than 1% during the Great recession of 2008-09.

What is interesting is that, as per the graph, during this worst extended period for equities in US history the regime has been of falling interest rates (and not rising!)…something to think upon…probably the connection is not that simple…but probably investing can be…or not

Yes, I understand what you are saying. I just think that the equity train is only picking up steam in India, and while it may slow down in a rising interest scenario, flows will continue to rise/stay strong. Therefore, it seems unlikely that it will slow down enough to keep returns low over a period of 5-10 years, unless the kind of events/scenarios that I fear play out.

Anyway, that is my perspective. You may well be right that equity interest can go down in a sustained high interest environment leading to lower liquidity in the market and therefore lower returns.

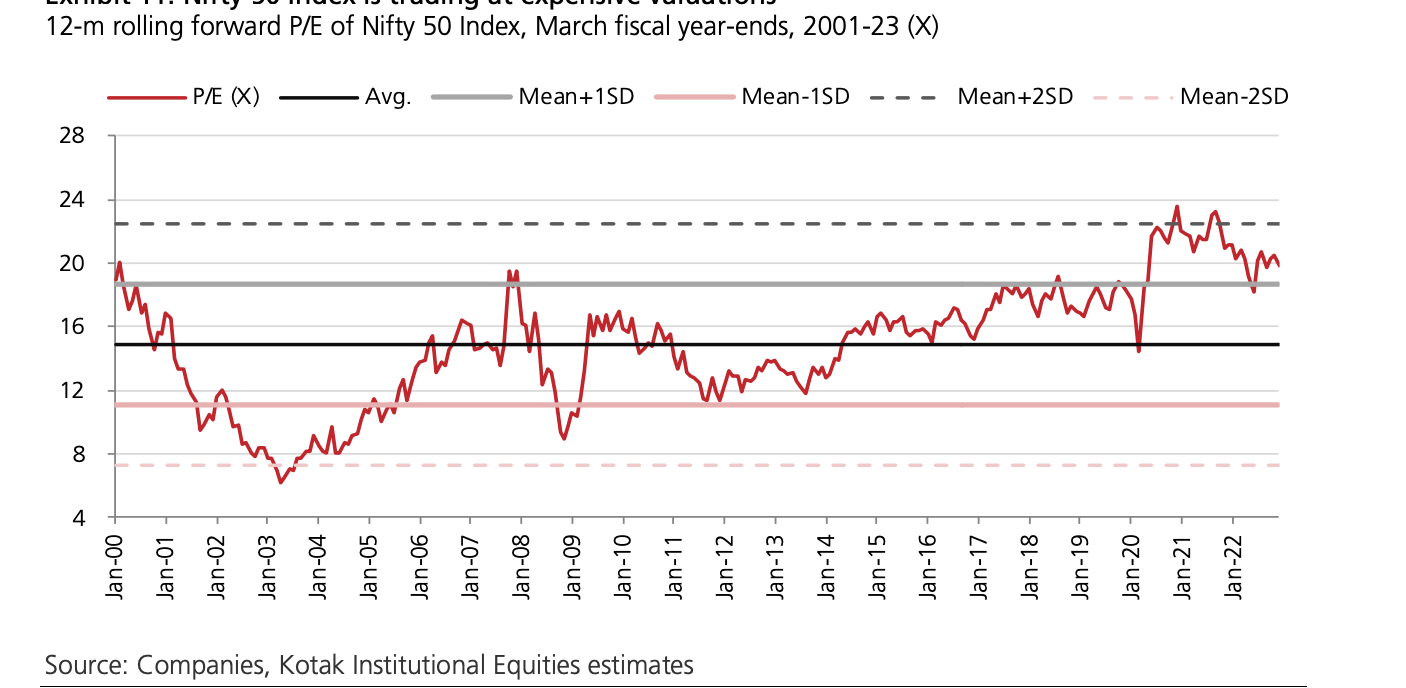

The problem with India is valuation …

If you own stocks with stable earning Gr > 10% , low debt and PE < 15 it is still ok …

Avoid High Growth and debt stocks … Also if you own any stocks that has history of < 13 years ie listed post 2009 , double check sustainability of earning …

We are closer to end of Interest hike cycle … but we may have bad economic growth ( at global level ) for year or two … so Long duration bonds are good choice in this environment

Big Shifts in last 6 months → Shift allocation of funds from fully valued equity and Quasi bonds to Gsec ETF and Gilt Funds .

Plan From April 2023 - Sept 2023 - Move to Mid and small cap equity ETF and stocks from Liquid fund as we may see EPS downgrades and bad commentary across many sectors …

Both US and India are moving into election year in 2024 . They don’t want high inflation so Rate cuts will be delayed and even if they happen it will very minimal unless

Economy collapses and Unemployment explodes

Both above are not so good for bull market but some sectors will still shine as compared to others