I’m 24 years old and starting to invest from now on. Well, I have prior investing experience, but now I’m doing it more seriously and professionally. First I will start to invest in mutual funds, then will try to find out some good stocks and will share here.

6 Likes

- First, I’ll start with small caps; I’m allocating 60% of my investments (long duration, less risk).

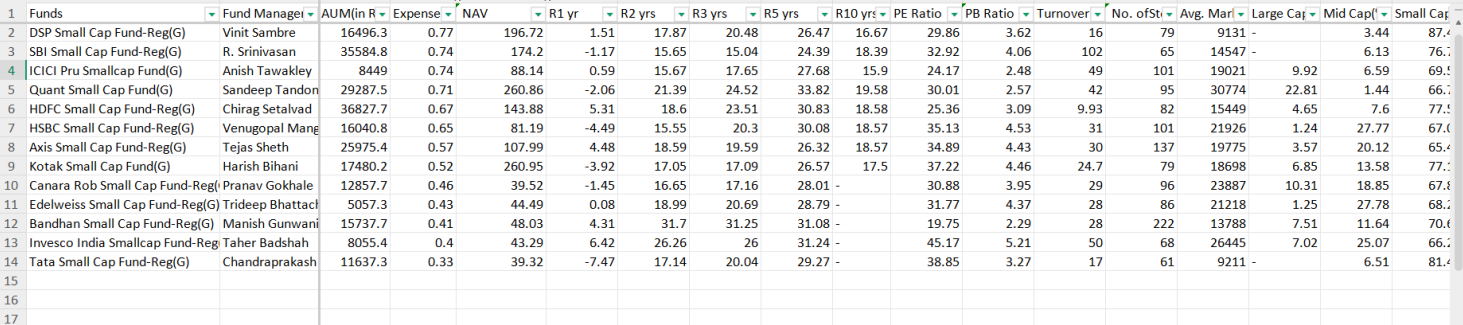

- So I have data of a total of 32 small-cap funds. downloaded from Mutual Fund Screener | RupeeVest.

- Now we will try to filter out a few good MFs.

Finding good fund

-

Removing Quantum and JM, as their AUM is in 3 digits (too small).

-

The average ER is 0.67 and the median is 0.63, so I’m removing all funds with ER >= 0.8.

-

For the ER issue, I’m filtering out Aditya Birla, LIC, Union, Franklin, Baroda, and Sundaram.

-

removing all the funds with AUM <= 5k cr; removed Bajaj reluctantly as they are accumulating their AUM pretty fast.

-

removing Motilal Oswal, as they are in their initial phase, but they are performing pretty well.

-

after filtering ER , AUM, and inception date

We have this.

-

removing ICICI as they are the bottom topper of returns in the last 10 years, 5 years, and 3 years.

-

removing quant as they don’t align with my current investment strategy (value investment); they rely on the proprietary VLRT framework, and also they were in a bad limelight recently.

-

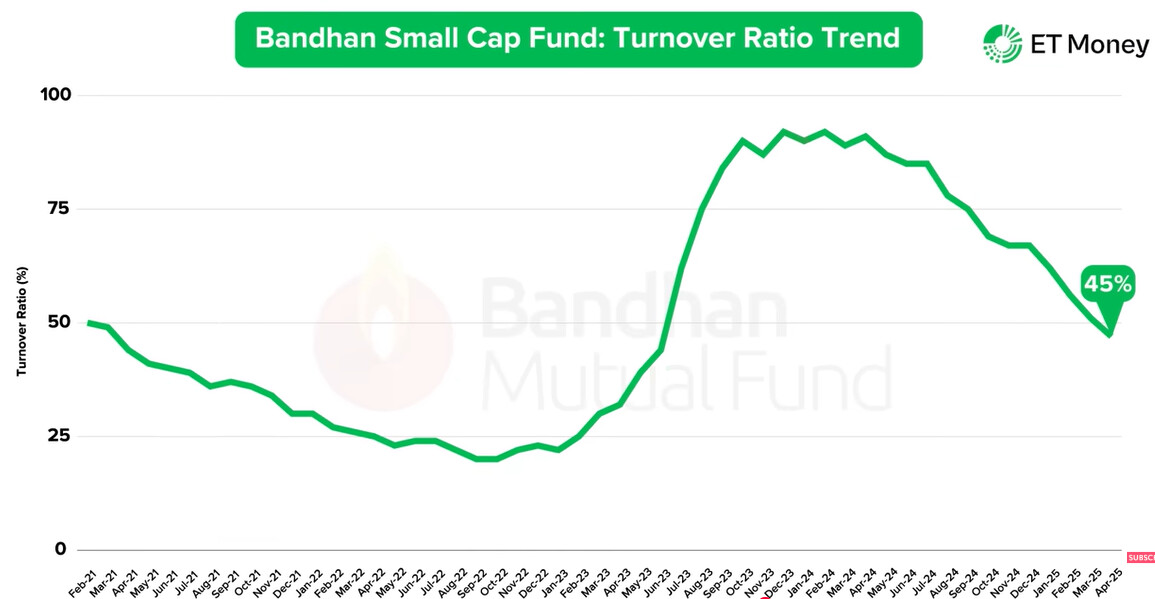

SBI has a turnover ratio of 100, which means they change their entire portfolio in one year (not value investing, I think). Also, they are the bottom performers in remaining funds in return for 5 years and 3 years.

-

ignoring PE and PB ratios, as I think they don’t matter in funds … because they invest across multiple sectors.

-

Canara and Kotak are bottom toppers in the current list in both Sortino and Alpha. We have better options than them if looking for returns (bottom toppers in 3-year returns and bad returns in other years). Well, Kotak has been working since 2004; it’s a good thing about them (time-tested), but I’m removing both.

this is the final funds list in the filter, in which if we look according to risk and benefit factor, we can shortlist 4 funds that are

- bandhan

- invesco

- HDFC

- Edelweiss

Now I’ll read about each of these 4 funds one by one—their history, their fund managers, and any bad reputation about them. I’ll write everything about them, and then we will decide where we have to invest.

Also, I’ll request to all my readers, please, give some valuable suggestions of yours, like what I’m doing wrong if doing so, and what I can improve.

Thnx.

4 Likes

…make sure you initially make a networth rebalance strategy (Meaning which is reviewed after every 2-5 years- Equity/Debt/Emergencie etc) …such a strategy should reflect your current circumstances …I mean 80% cash flow coming from your job, etc…for choosing funds on a portfolio level two strategies can be followed largely…over lifetime…A) .choose 10-20 funds …after every 3-5 years churn them… make sure they together never reach beyond a set percentage of your networth (Here the assumtption is youll get lucky with your choice)…Kill funds ruthlessly after 3-5 years… … B) Another one here choose one fund (Whatever cap irrrelevant)…After every 3-7 years (Kill or reduce the exposure to the fund manager if he/she significantly underperforms - then choose a new single one)…On a portfolio level make sure Equity+Fund_Manager never reaches a set %age of your networth- if it does reduce exposure…(Here the assumption is over lifetime youll find good fund managers once and survive)…Both these strategies assume its not your full time job - main cash comes from job and you will follow these lifetime…Only exposure you manage is make sure you survive and then make gains…I dont know your personal circumstances and this is not SEBI Registered advice please consult your Financial Advisor for the same…

Plus write this all down (To review after whatever duration you set-- to really reflect your circumstances) - follow it to the core

Only thing you control largely is your exposure and duration (Rest all is your luck and analysis)

Typical mistake young people make is following someone else life

remember n=1, your strategy/ your story it will be unique from the entire world

Wish you all the best

2 Likes

Thanks, Himanshu, for your valuable reply.

Truly, I will follow the rebalance strategy, I will review all my MF investments every 3 years, and also I will continuously inform on this page.

Right now I’m investing all in equities, and for emergencies my father has a few FDs. I’m considering it as an emergency fund for the whole family. I’m making an emergency fund from my pocket this month and will increase it gradually.

Also, I’m going with your strategy B will invest in 2-3 funds across different cap , and will review all the MFs

1 Like

To be frank,

Don’t know for sure,

From a cash flow perspective

if you have a job from where you’re getting cash flow which is stable~ your time horizon or strategy makes sense~ (If business by nature it would be volatile which your matching with a super volatile cash flow)

Regarding strategy B, its more about switching cost, over lifetime, (Thats why it focuses on 1 fund) - In the end I feel you’re giving money to someone to manage thats it (You are giving money to three teams)

Plus further assumption is you can choose those three people who willl out perform over 3-7 years (Caps dont matter or thats not the only way exposures are really divided in the market)

From my experience you try to elongate the duration of family portfolio (So I think there should be limit of transfer of money from father too) - That ensures your family survives more than you think - you fail first - never your family - there are levels - so emergency fund from fathers perspective isnt there

(Obviously its very personal and I dont know you deeply in that regard)

I am not sure, anyways I am wrong a lot

Wish you all the luck and good wishes

This all does not apply if you are planning to start a business of mutual funds or stocks or something

Not be to be critIical or anything here…but just take into perspective your lifestyle goals and aspirations.

Getting rich slowly is most for fund managers/big shot CXO’s who get decent annual salary and bonus year on year (irrespective of performance!).

Warren Buffet had already achived financial freedom in his early 30’s. Unfortunately, people have taken his ‘get rich slowly’ approach without considering their own personal/financial situations and life stage.

Whats the point of being wealthy at Old age when you have no teeth left to eat or no energy to travel ?

Early 20’s, early 30’s we need to be more aggresive in our approach to wealth creation.

Unless your priority is to make your ‘future’’ grand kids wealthly, then take a 40-year view ![]()

I made a big mistake not taking advantge of my 20’s and today I am starting investing with reasonable networth deployed at age 32. While, I still have a long runaway ahead, but had to pay huge opportunity cost. (completely missed out 2018-2019 bear market, despite learning gyan from our dearest VP gurus)

3 Likes

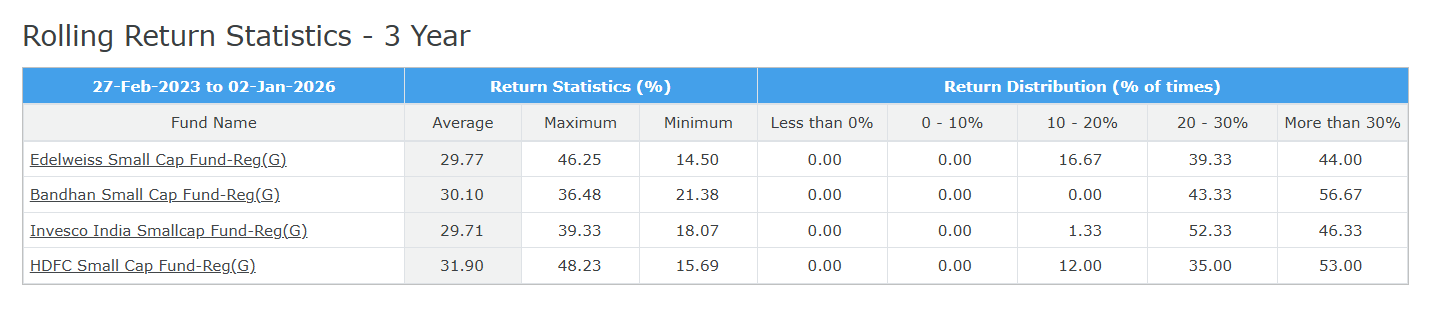

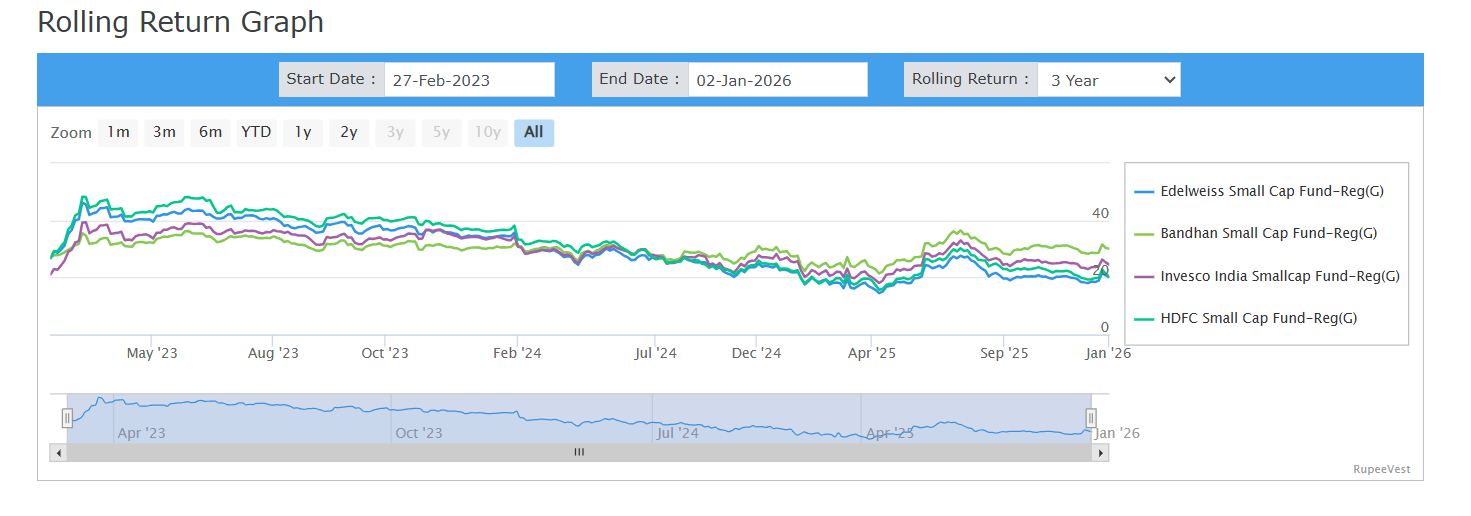

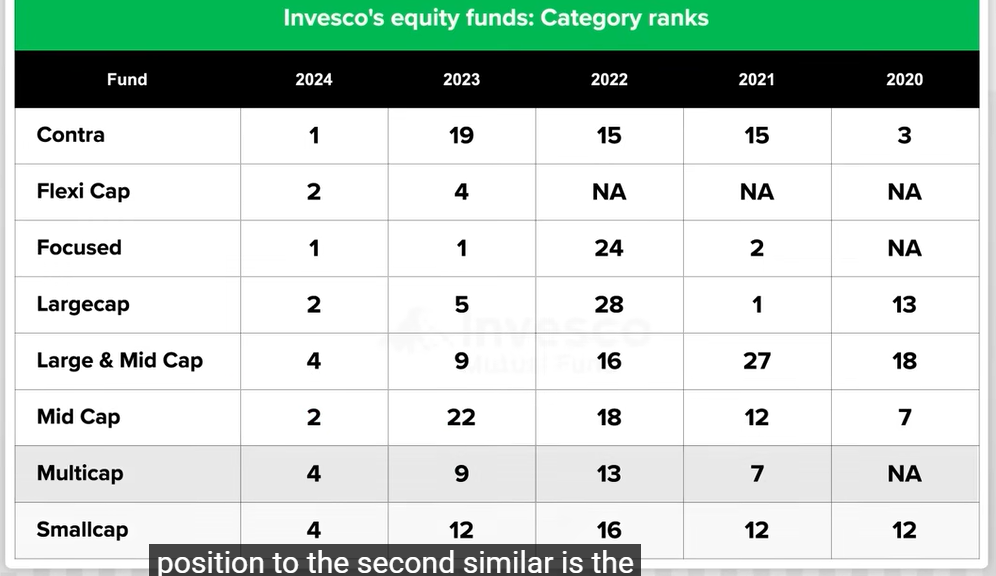

The rolling return of the above-mentioned funds is given below.

HDFC small cap → HDFC had been on top from 23 to mid-24 and is also doing well. Also, their average RR is the highest.

Bandhan small → bandhan was average performer earlier, but after Gunwani Sir joined, it’s doing good

invesco& Edelweiss—they are average performers.

Bandhan and HDFC have a slight edge in RR. I am impressed by HDFC, as Bandhan had the edge of the Covid crash. Also, I’m seeing that Edelweiss has been at the bottom since 2019.

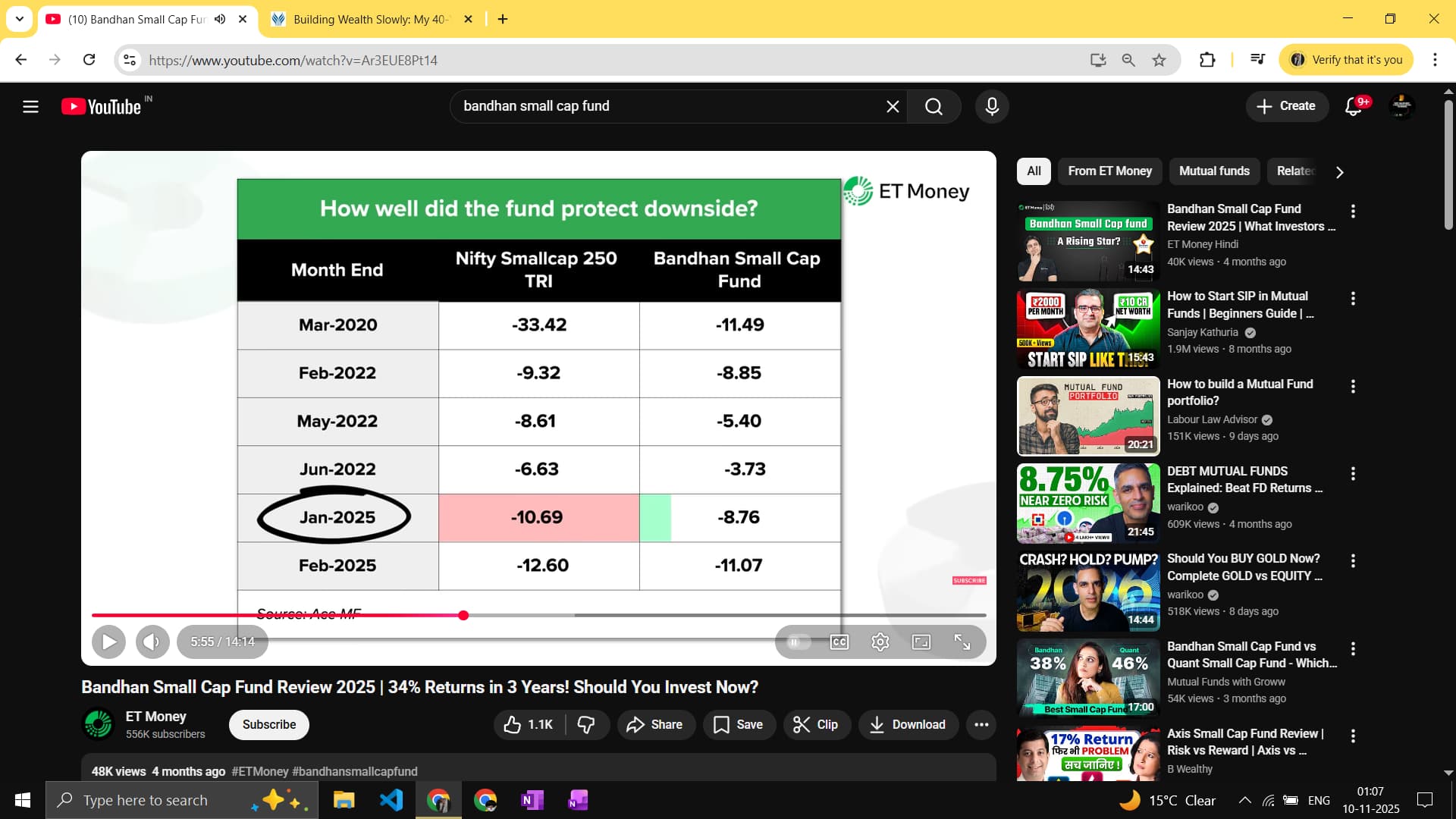

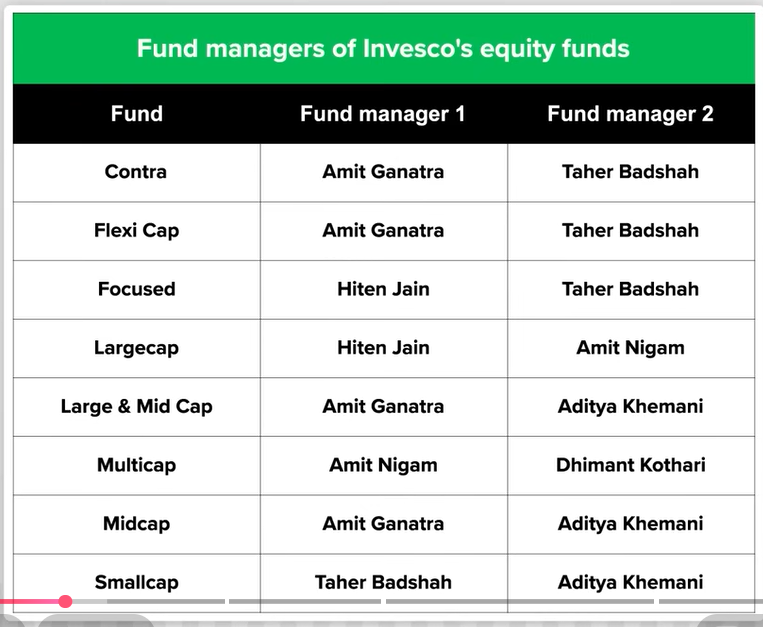

Bandhan small cap is managed by the same fund manager who managed Nippon Mutual funds for a long time. It’s a good point, as he is a well-reputed fund manager.

bandhan

Bandhan started just before the covid crash… and it helped a lot.

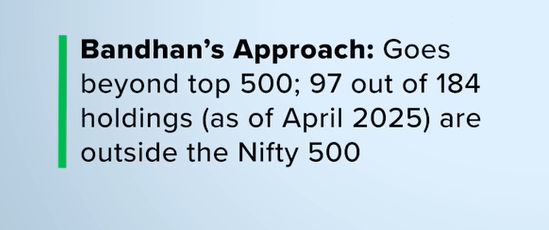

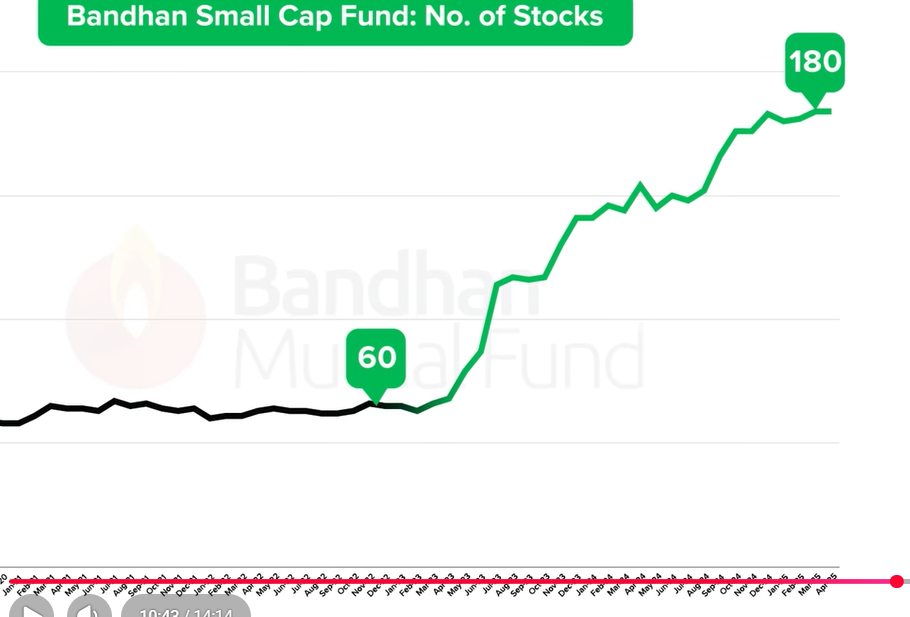

Bandhan’s strategy is reducing risk by owning/diversifying to 220+ companies, known as the “long tail approach,” but what if a bear phase comes and most companies out of 220 will underperform, as they are the quantity pick, not the quality pick?

Look, Bandhan has a good manager, but I’m looking at Gunwani’s pattern; he’s frequently changing his companies (switching), so maybe in a few years he’ll leave Bandhan???

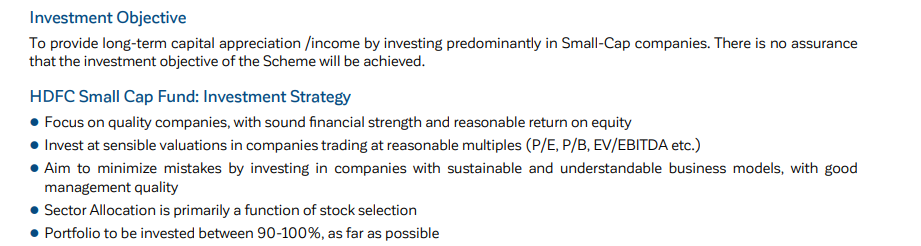

HDFC is well managed by a manager who is also managing their mid-cap, with good performance there also (one of the best), and they are time and market cycle tested (that’s what the other 3 funds lack). A low turnover ratio over time means they have confidence in their investment and they are performing well also, but the issue is they have the second-highest AUM at ~36k cr (following Nippon at ~66k cr). I think 36k CR is a big amount to handle in small caps . Very high expense ratio, like, common man, 0.67 is really high.

investment objective aligning with my objective of long-term capital appreciation.

Chirag Setalvad has been with HDFC since his career started, so we can assume maybe for the next 5-10 years he will be there (not like Gunwani, with due respect).

Look, I’m not liking Invesco, as you can see by rolling return. These returns are new returns; they were not that good of a performer in the past.

In my opinion, HDFC is for the bear phase; value investing is needed there, but in the bull phase (currently at its peak), we can go with Bandhan.

Whatever experience I have with MFs, I can tell that after every couple of years a new fund ranks 1 and 2, but we can’t change our funds every year, so we select a few funds and stick with them.

My strategy will be that when I get my salary, I will first wait and watch the market for a few days and will consider stocks that I can invest in on my own; if I’m not able to invest on my own, I will put the rest of the money in a mutual fund.

I’m going with HDFC, as it is a time-tested fund. Also, they are good when the market comes into a bear phase, and I think this is the time of the bear phase, so I’m adding in to HDFC.

Also, please wear mask and use air purifier if you are living in NCR area, as the biggest investment u can do is in your health… to increase not only your lifespan but also healthspan

First and foremost, happy Republic Day to all.

after investing in a small-cap fund. I started exploration … searching for stocks that can give a good return.

I went through multiple companies and found 2 in which I can invest.

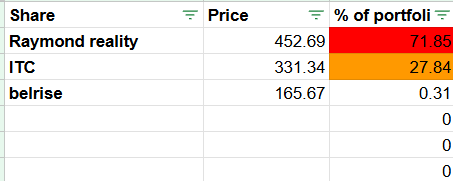

Raymond Realty—a reality company working in MMR separated from its parent company last year—has a big 100-acre land in Thane, and management is working well. IMO it’s underpriced right now .

First, I will find some more stocks in which I can invest to bring down the 72% proportion to a decent value. If after that the price of RR is in my range, I’ll buy more.

ITC—a great company that has a very large share in the cigarette market; also, it’s exploring the FMCG area.

- I see there will be a smaller increase in the prices of cigarettes, but only a marginal increase of 2-5 rupees. I don’t think it will affect people’s buying decisions.

Problems

- The problem is the black selling of cigarettes, which will dent the revenues of the government and also of ITC, which is funding these revenues to grow their FMCG market.

- What if the government increases taxes further, as I saw that taxes are low as compared to WHO recommendations? So maybe in the future the government will increase more taxes to increase their revenue, which is already dented due to last Oct. GST cuts.

it’s still going down, and i wil accumulate more if it comes to my range.

Belrise— I bought this in very small proportion to observe the company will sell it in a few days.

yeah… i put a lot of money in RR. That’s wrong, I know. I will maintain a healthy proportion between invested shares from next month

Right now I’m studying the power sector, the transformer sector to be more specific.

I’m open to feedback—happy to hear what I can improve or if I’m doing things right.

2 Likes

Raymond realty has some management issues. It was highlighted in the dedicated thread for raymond realty. Please go theough thw thread.

Hi Robin, thanks for the reply.

I went through the entire RR thread, and honestly, I couldn’t find any real management-related red flags.

If you’re talking about the family issues—like the mismanagement claims made by his wife—IMO it looks more like a case of both sides trying to defame each other. There’s no solid proof backing the “personal fiefdom” narrative.

From a business point of view, management has mostly delivered on what they said. The only concern I see is the EBITDA margin coming in lower than what they initially guided. Their explanation was that after the demerger, RR is now a separate entity and has to manage everything on its own, which obviously increases costs.

That said, they should’ve factored this in earlier. Claiming ~20% margins without fully accounting for post-demerger costs was a bit optimistic.

The 20% EBITDA margin is not for FY26. They’re targeting it by Q4 FY26 or Q1 FY27 and then sustaining it.

Still, if execution goes well, they should be able to meet their revenue guidance, which is a positive sign.

Overall, I’m invested.

At current levels, it looks quite cheap. Management is mostly doing what they said they would, and I think over the long term it can give very good returns.

All the best Nishant. If you want to ever talk and bounce off ideas about investing, happy to be a part of it. I am 23 and also investing actively across different assets and investing styles.

Hi @ShaheerAnsari,

→ i added more RR and brought the avg. price to 446

→ will invest more in ITC as it will go down, IMO. The next quarterly result may not perform well due to a sudden price shock to customers. There we can buy more at 315 → 305 → maybe even below 300. I missed the previous dip.

→ Right now I’m looking at the Anant Raj data center and transformer sector…because their business prospects are good enough, but in the market they are not performing very well.

→ will love to listen from your side to what ideas you are exploring.

Valuable lessons learnt by me till now,

→ Don’t invest all the money in one go. When the US attacked Iran, I assumed the mighty US army would eradicate the Iranian regime (citing Arabs, Israel, and their own people against them). Hence, the war will be over in a few days…but the Iranian regime taught me a valuable history lesson… We don’t fight on papers; we fight with strategy + will + intelligence + special powers, then military might. Well, I didn’t invest in one go…but eventually exhausted all savings till the 17th-18th of March…and these people are still fighting.

→ Right now I’m also looking at my pattern and seeing I’m basically trying to thrive on people’s fear … My investment strategy in the recent past was… I look for companies whose prices drop and also have good chances to bounce; I invest in them (with some problems, obviously)…well, this is a good investing style…but doing only this is not great; I should look at rising sectors like data centers, rare earth, and power sectors.

→ I also assumed gold prices would increase … as all the other investment options are not performing well … so investors will again look to gold … and demand it; hence, the price will increase … I was so wrong.

PF Update

- Raymond Reality → (40%, @424) → special demerger situation, causing it to be at cheaper price (distress capture strategy)

- ITC → (29%, @313) → same strategy as above → good business at cheaper price

- Anant Raj → (15%, @465) → rising sector strategy.

- InterGlobe → (10%, @4230) → again, a distress capture strategy → good business, and I’m sure after 1-2 quarters it will again start performing.

- IDFC → (3%, 70) → (distress capture strategy).

- SBI → (3%, 1220) → PSU banks have been performing very well since the last 1-2 years; also, their P/E ratios were quite low. Also, I wanted to ride the PSU bank rally. (Momentum-driven allocation)…but war happened just after the investment.

2 Likes