The traditional way of buying MFs is through RTAs (CAMS, Karvy, etc). These are the 85% odd of the market as of today. The whole appeal of Star MF like platforms is that essentially you can aggregate all of these RTAs and make the MF investing process 1) completely digital so no need to go the RTA with physical documents & 2) convenient since can do all the processing for different mutual funds at one place instead of coordinating with 4-5 different RTAs and 40 different AMCs. The competitors as of today are MF Utilities (platform run by AMFI) & NSE MF (NSE run platform).

Essentially, Star MF was able to acquire so much market share because they just had superior functionality in the beginning when they launched, so when various distributors were deciding which platform to opt for: Star MF seemed the obvious choice. There is a moat, switching costs are relatively high. I dont think it is feasible for a distributor already on Star MF to switch unless functionality being offered by another platform is much better. Essentially, think of what it would be like to switch from using Gaana.com to Saavn/Spotify. You would have to migrate all your songs from one platform to the other, which makes it unlikely you would do so unless there is a significant benefit from switching. It is a similar case from Star MF.

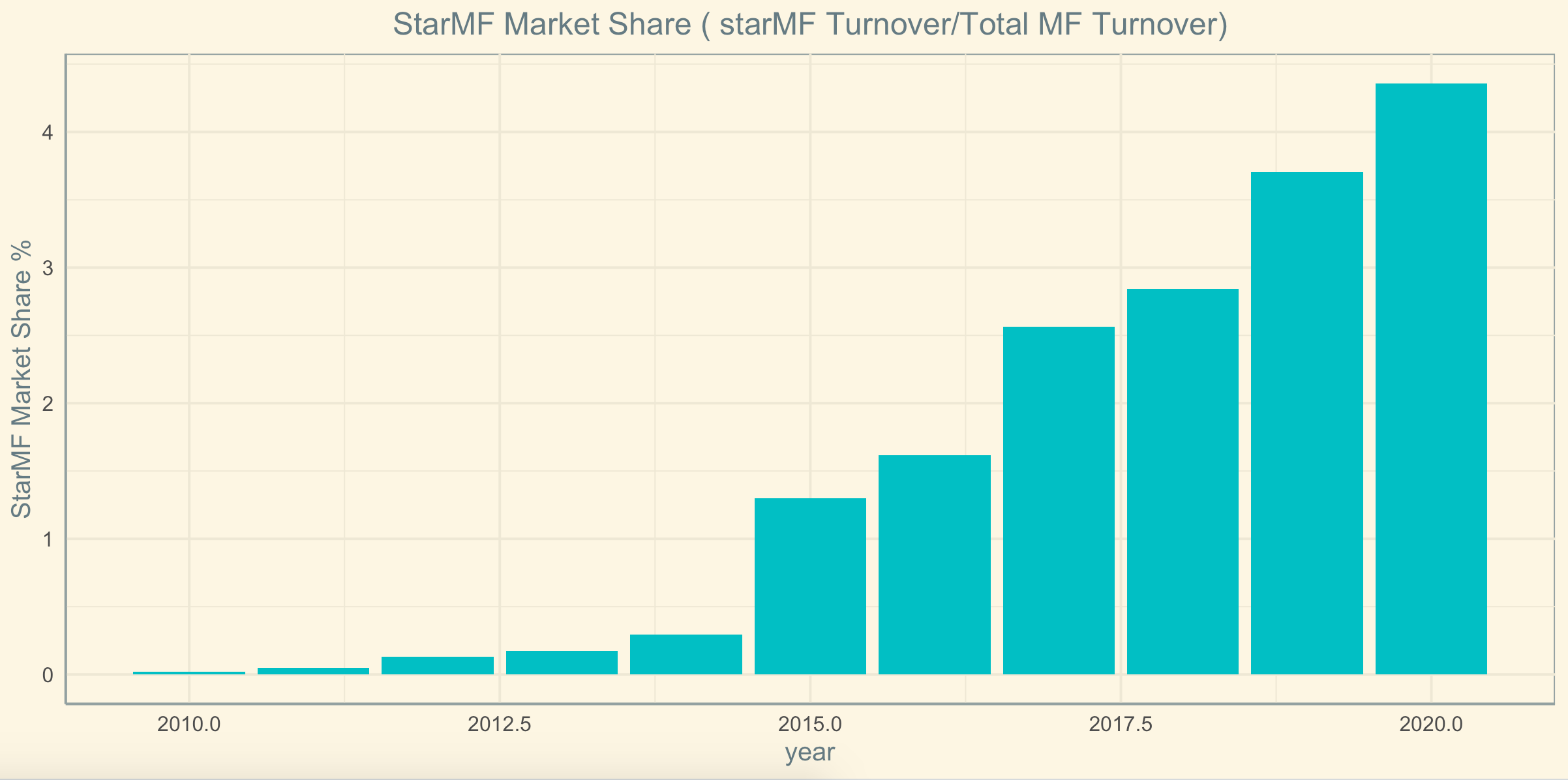

So, Star MF today, which already has 50k + distributors on its platform, out of total distributor base of about 120k in the country, is in a great position to scale the platform up. Growth can come from:

- Existing distributors (already signed up at Star MF) routing more of their existing client transactions through Star MF

- Signing up of more distributors

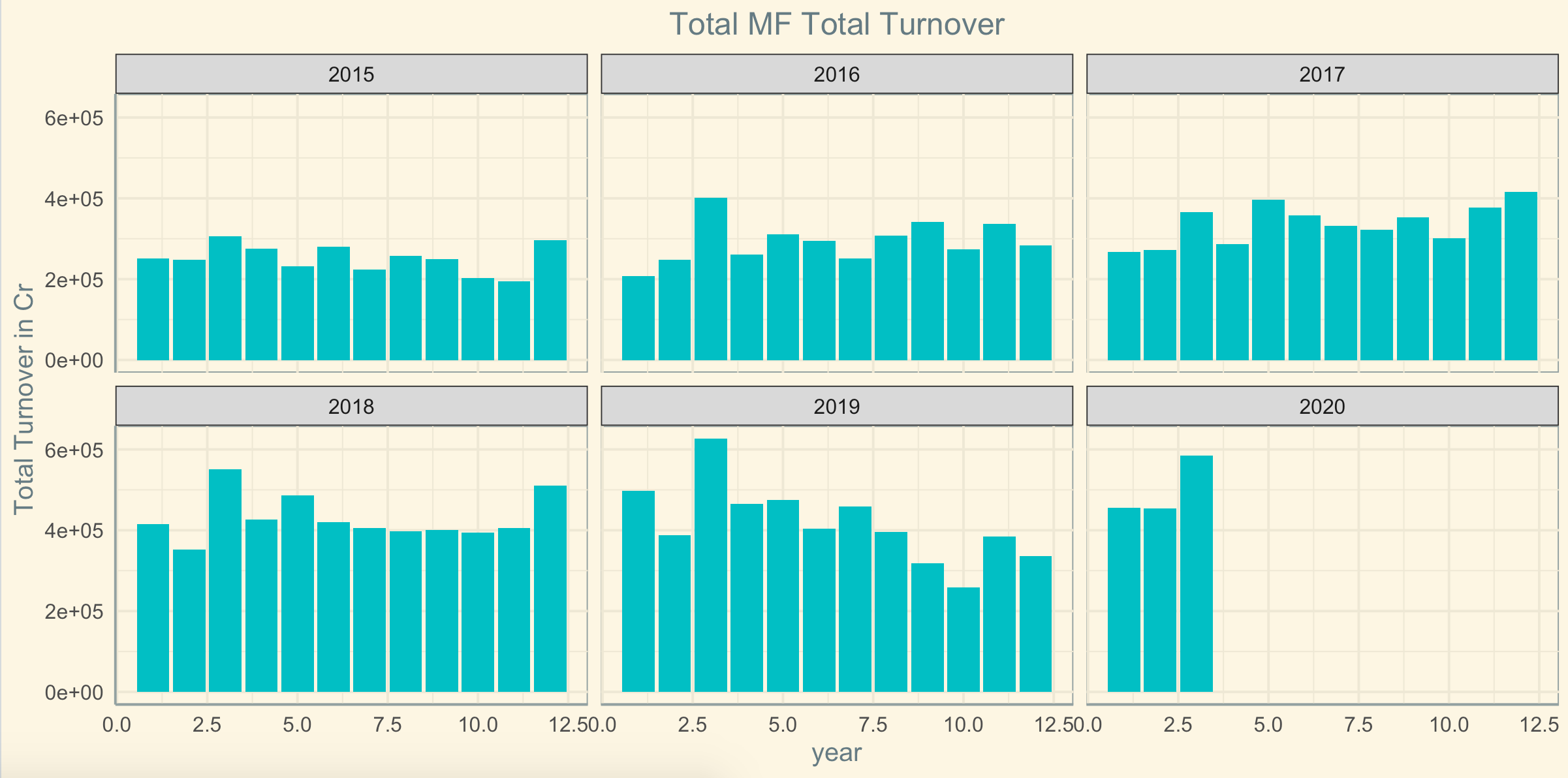

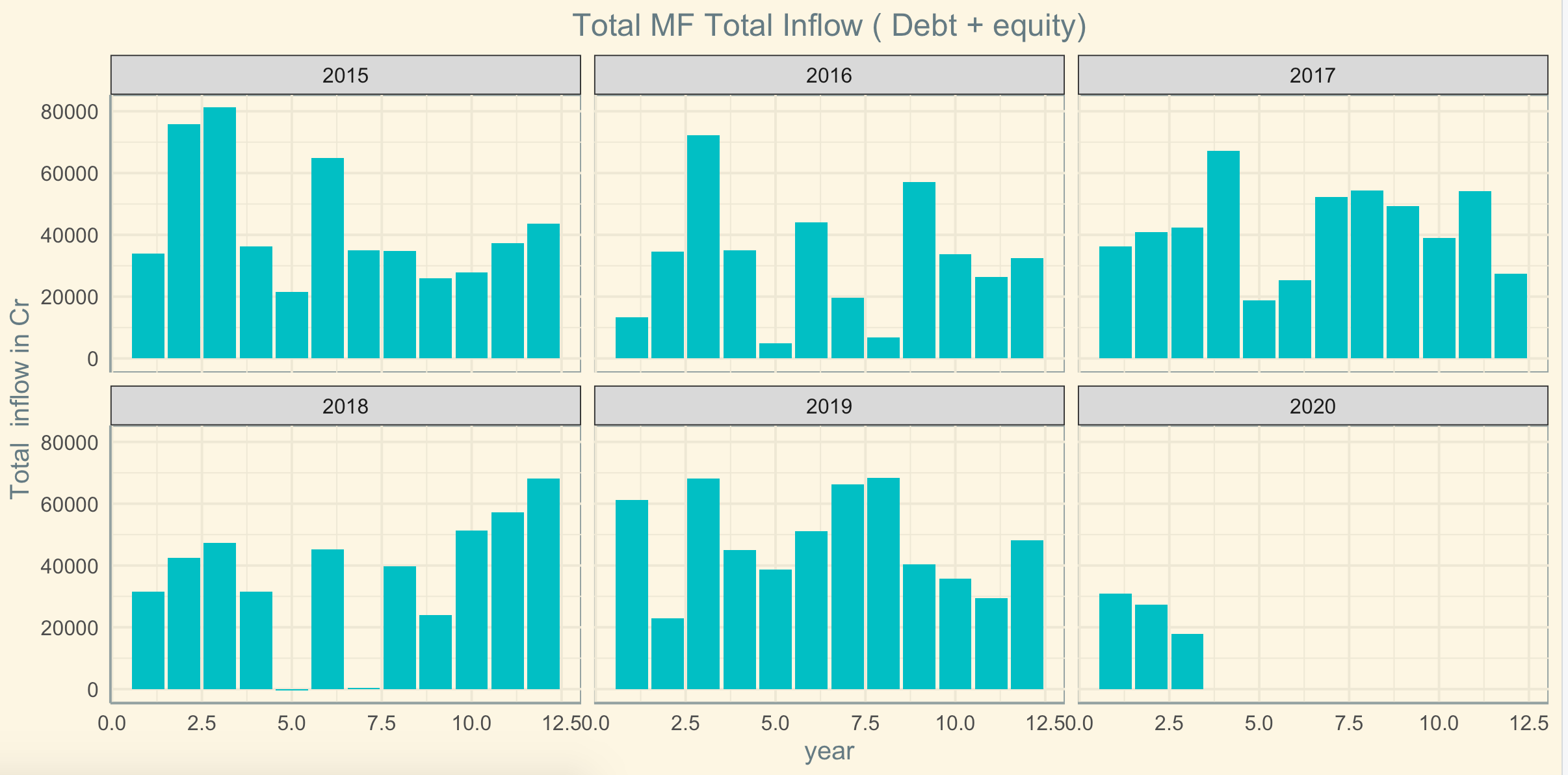

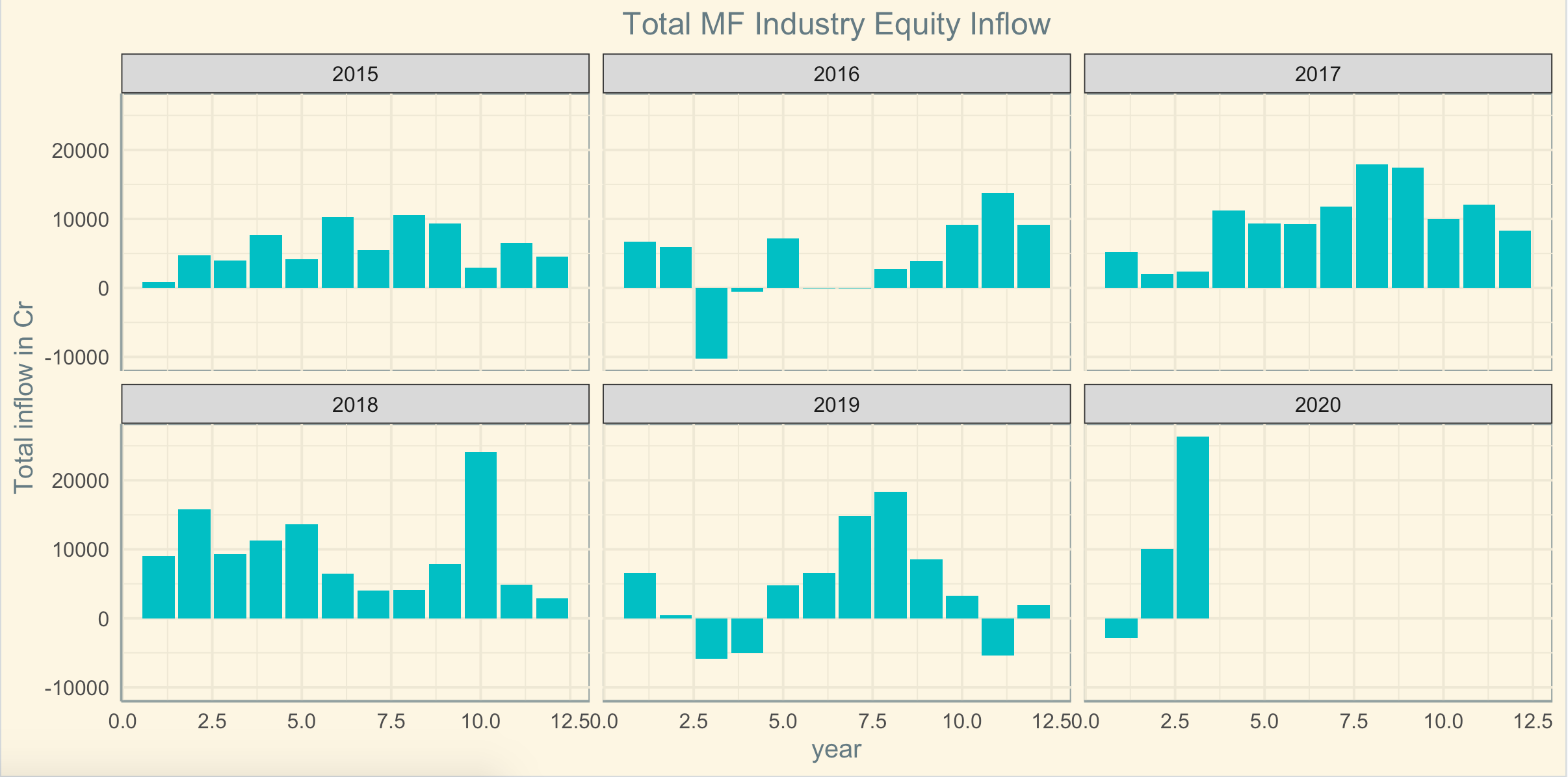

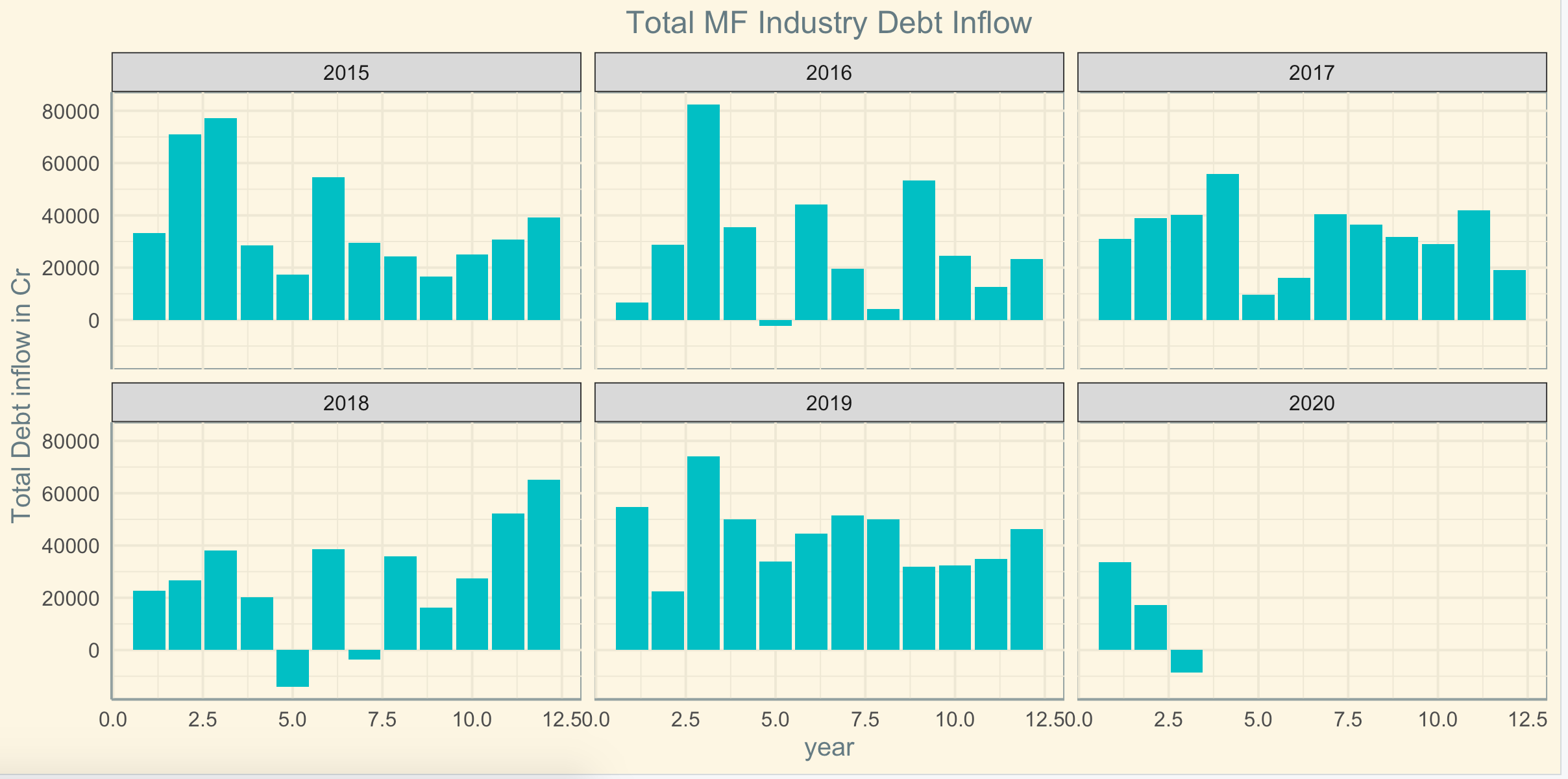

- Overall growth of the mutual fund industry transactions

My understanding is that Star MF is largely a platform for Mutual fund distributors vs PayTM is more for retail investors. Essentially, PayTM can be a customer for Star MF. I think there is a long term threat of investors going direct rather than going through a distributor. As of today, less than 20% of equity transactions are done without a distributor. If Star MF can keep tying up with players such as Zerodha, who are likely to attract retail investors, I think this risk can also be mitigated.

BSE is one of the top picks in my portfolio largely riding on Star MF. At current price, you are basically getting the entire company at below net cash value, so the downside should be relatively small, whereas you have the entire growth of Star MF & potential monetization of INX & EBIX as potential upsides. All this, while the company will reduce its cash balance and pay out dividends. At this price, dividend yield essentially should be 10+%, makes it a no-brainer according to me.

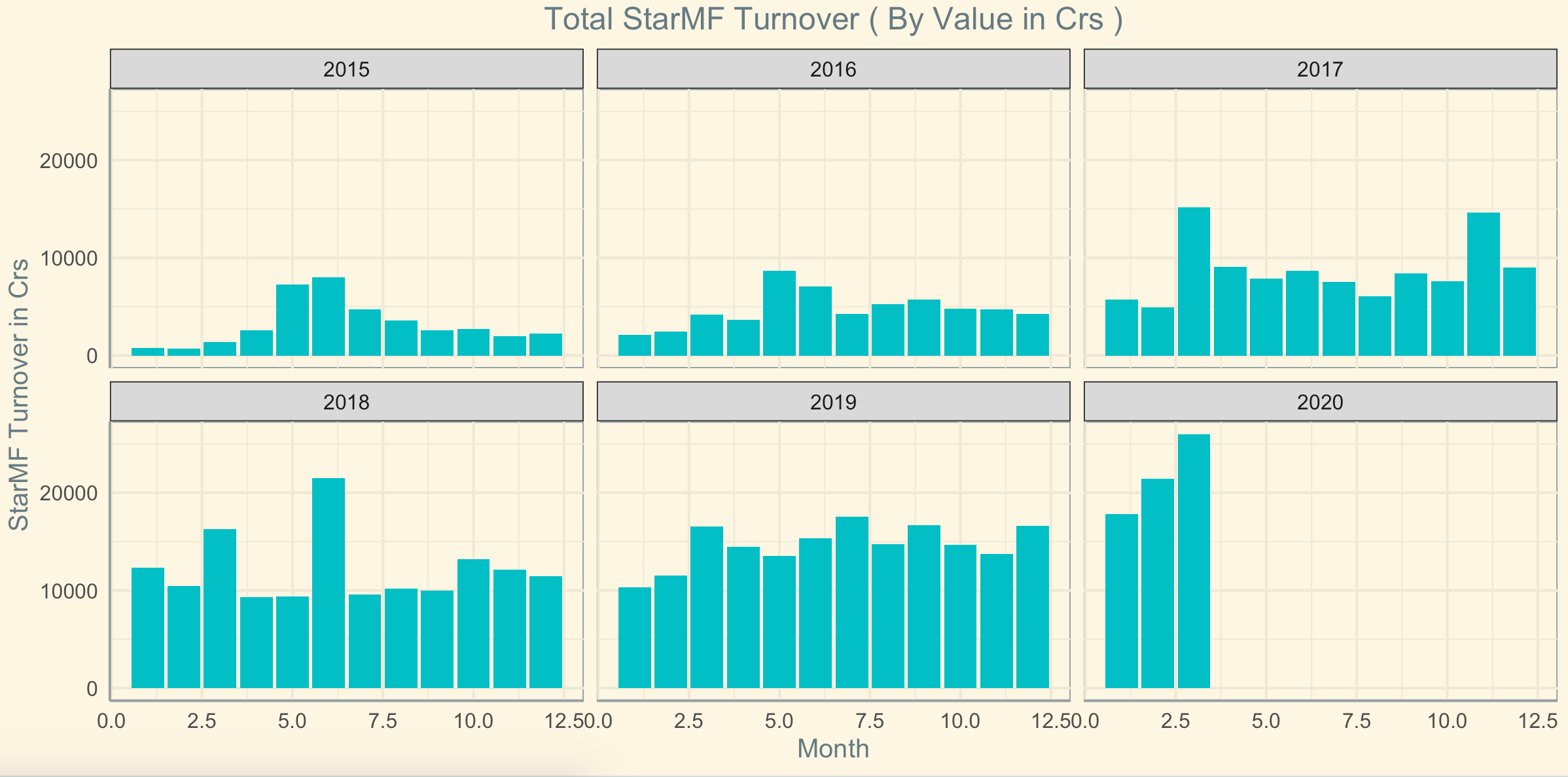

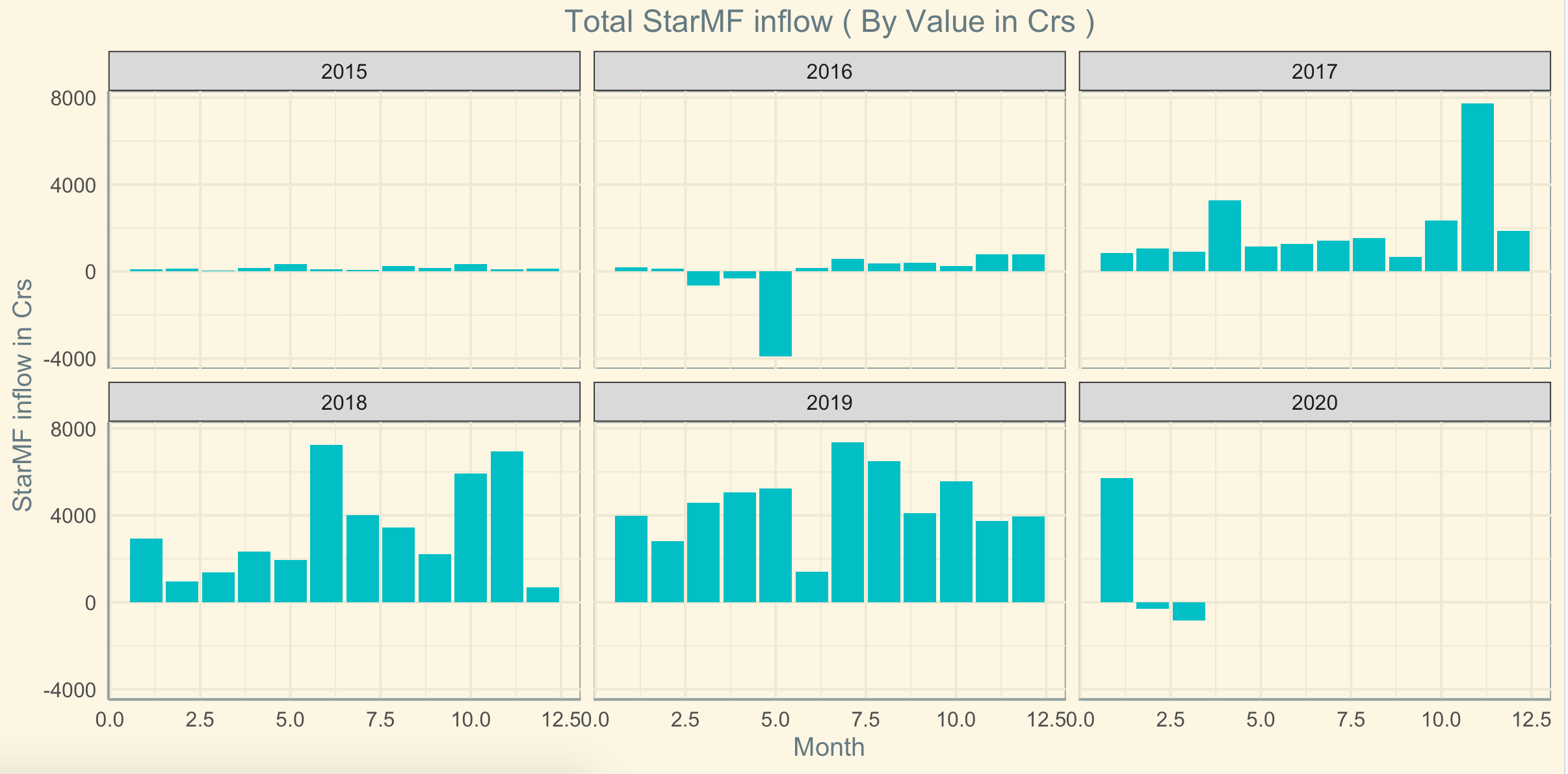

There is no reason why Star MF by itself could not do about 200 mn transactions in 4-5 years time (which would be 40% of industry transactions). At price/transaction of about Rs 15 (CAMS charges Rs 20+), you are looking at revenue at Rs 300 with PAT of Rs 180 cr. Valuing this company at about 20x, 2x of the current market cap of the company can be explained by just this one product in 4-5 years time.

Plus, I actually think Star MF would be one of the beneficiaries of the whole COVID situation. Lots of people today who want to open MF accounts cant, because they need to do physical paperwork, sign, etc; not feasible in a lockdown. I would not be surprised if Star MF growth trajectory actually increases post the lockdown. Might be a second-order effect of the current situation.