While BSE’s historical performance has been impressive, the core investment thesis was based on the rate of change — the pace at which traders migrated from NSE to BSE, largely driven by regulatory support. That phase of rapid displacement now appears to be largely behind us.

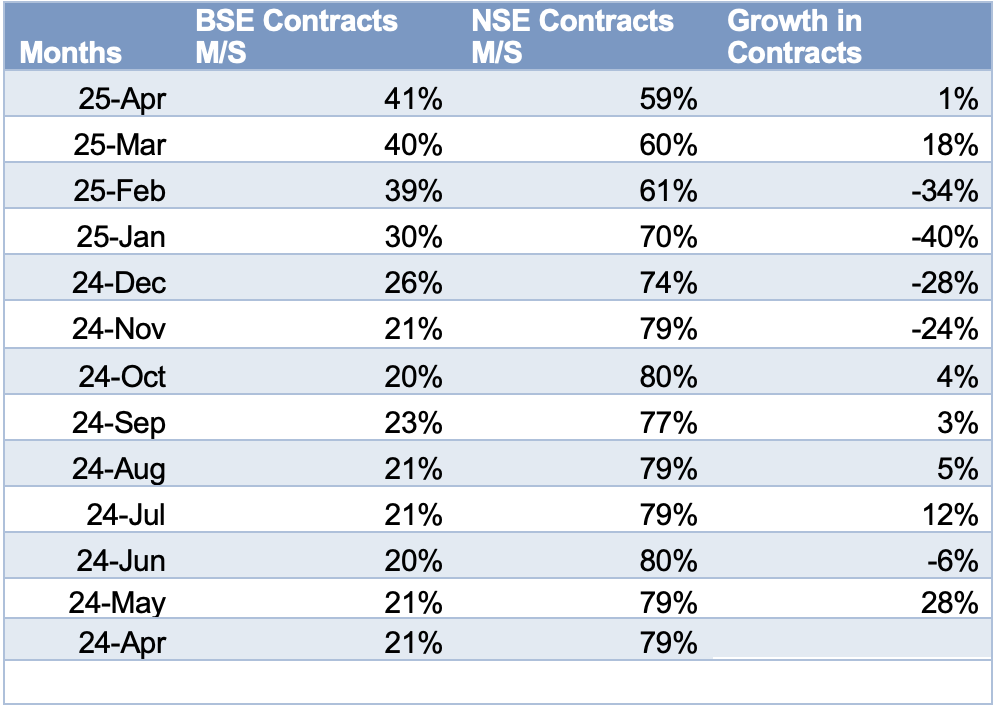

Today, BSE has already captured close to 40% market share in terms of contracts traded, and about 35% in notional turnover. These were the more accessible milestones, as both metrics naturally tracked each other due to the similarity in contract design and the influx of traders moving platforms. This shift reflected the easier part of the transition — where low friction and regulatory nudges made it convenient for traders to adopt BSE.

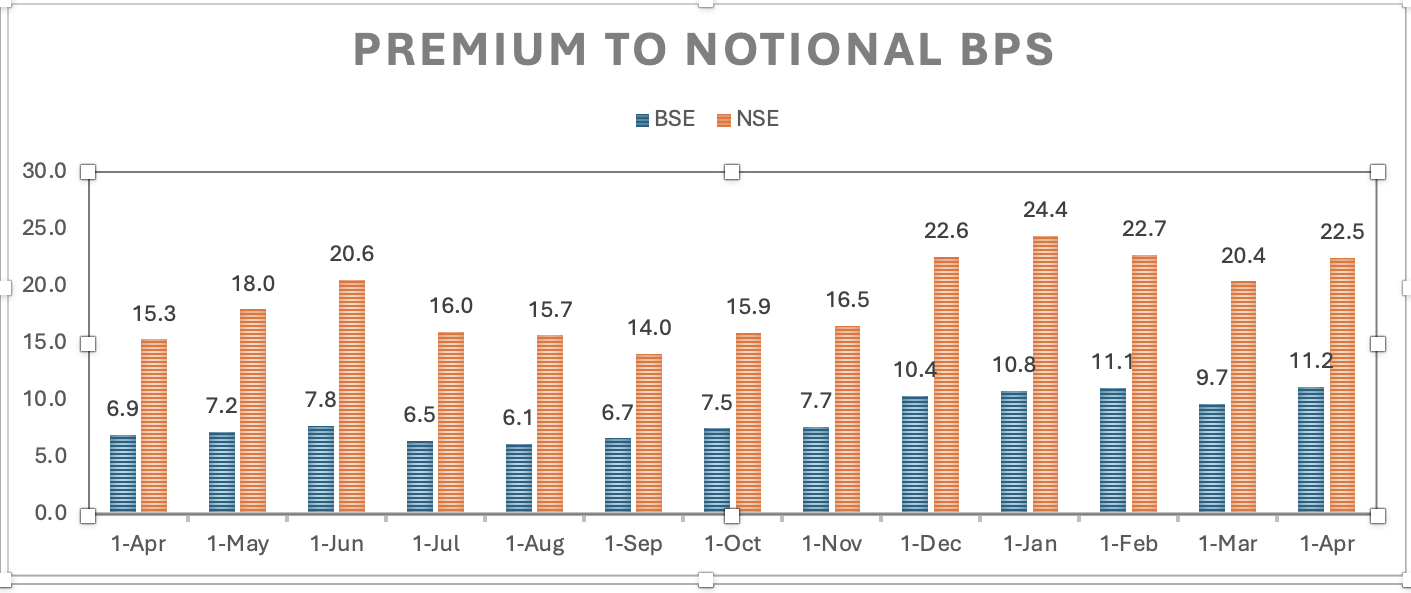

However, the real challenge lies in premium turnover, where BSE’s share remains at around 25%. This is the most meaningful metric when it comes to evaluating true liquidity and depth. Premium turnover reflects where serious capital is being deployed — especially by larger, more sophisticated traders — and this doesn’t change quickly. Unlike contracts or notional, premium share improves only when the market consistently offers tight spreads, depth across strikes, and confidence in execution quality.

Given that much of the initial migration has already happened, we are now entering a phase of structural, gradual growth. Without a fresh regulatory push, the pace of change from here is unlikely to be as sharp as before. The duopoly between NSE and BSE is approaching saturation, with a 50:50 split in contracts possibly being the upper bound. From here on, any gains in premium share will be slower, and driven by operational strength and liquidity quality — not regulation.

The attached charts support this view. Would love to hear your take on how fast, realistically, BSE can gain premium market share from here. What does an Investor from here bet on?