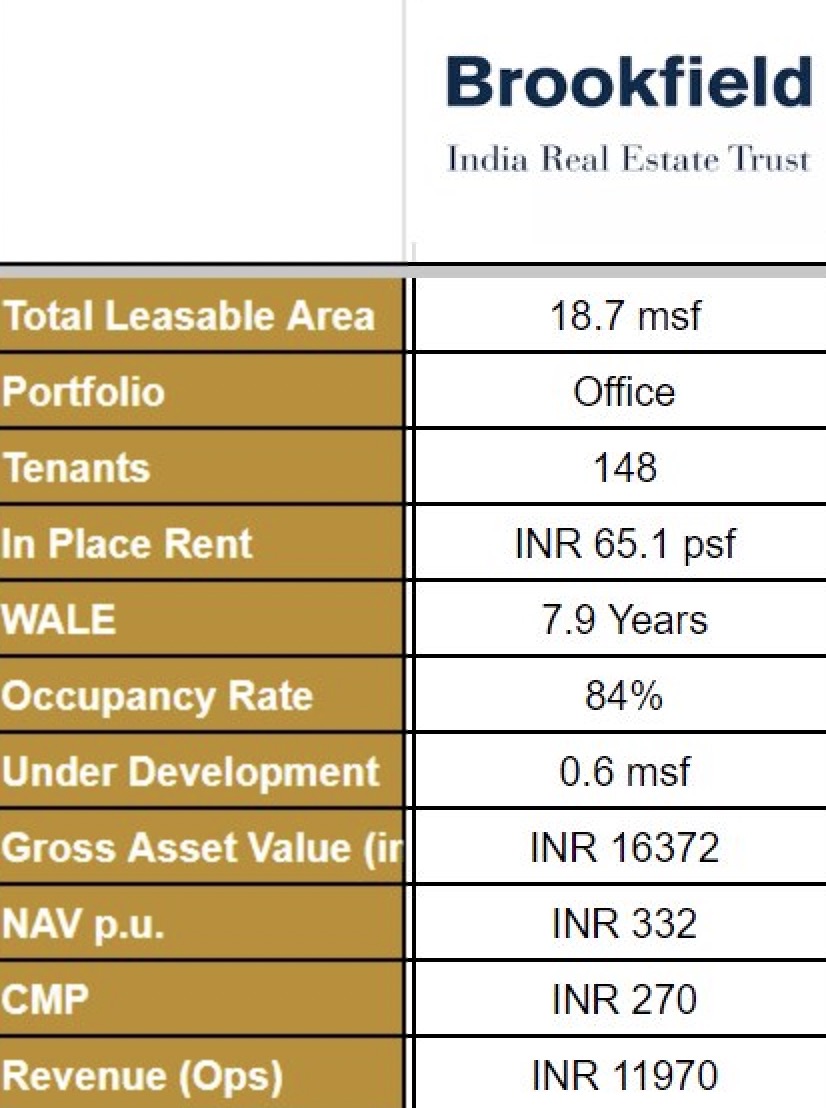

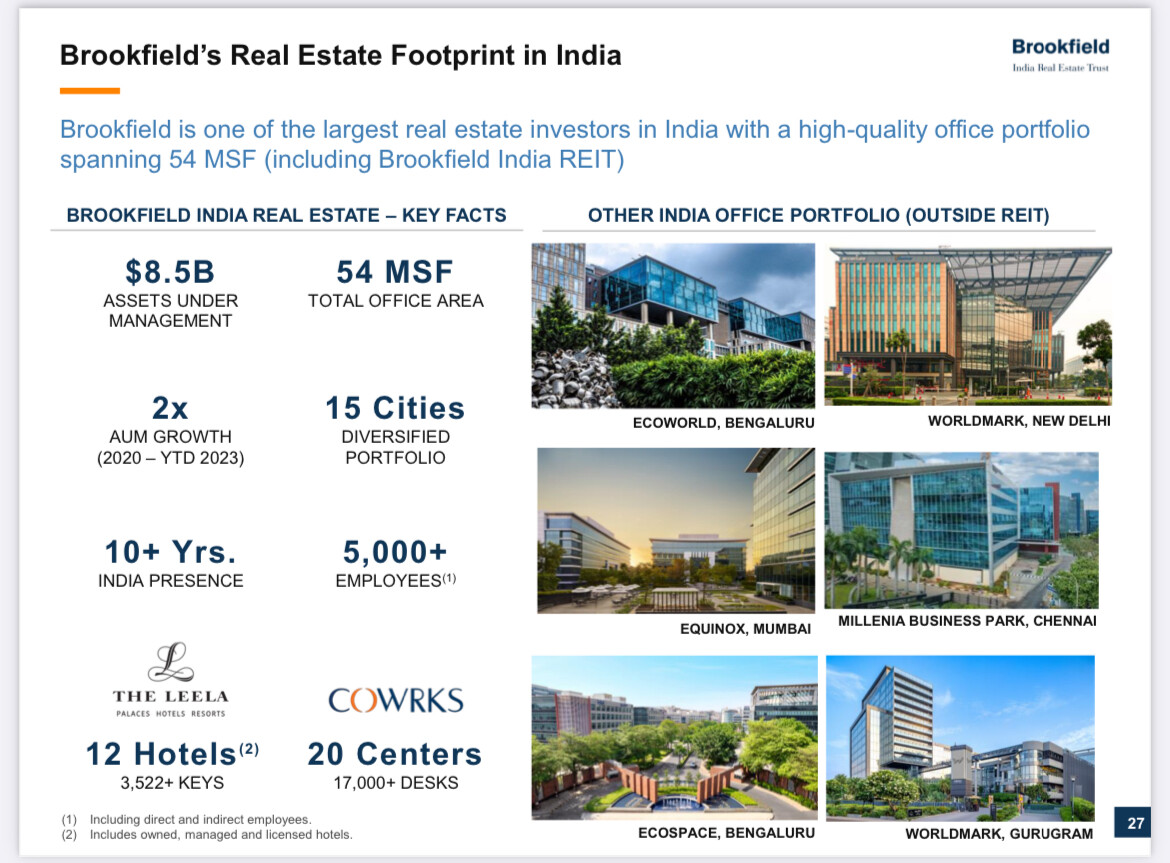

BIRET is India’s only listed Institutionally managed Trust, run by Brookfield Asset Management, one of the largest Real Estate investors in the world. The REIT manages popular office spaces like Kensington in Powai Mumbai, Candor Tech parks in Noida, Gurugram and Kolkata. Some of BIRET’s current tenants include Accenture, Amazon and Samsung

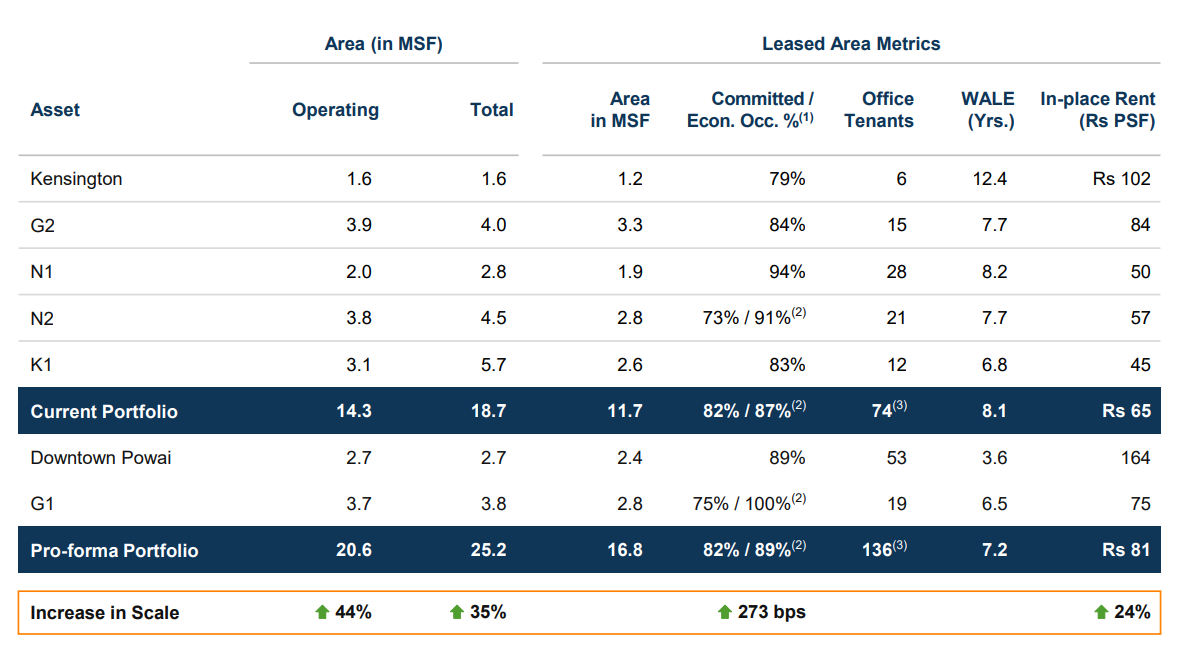

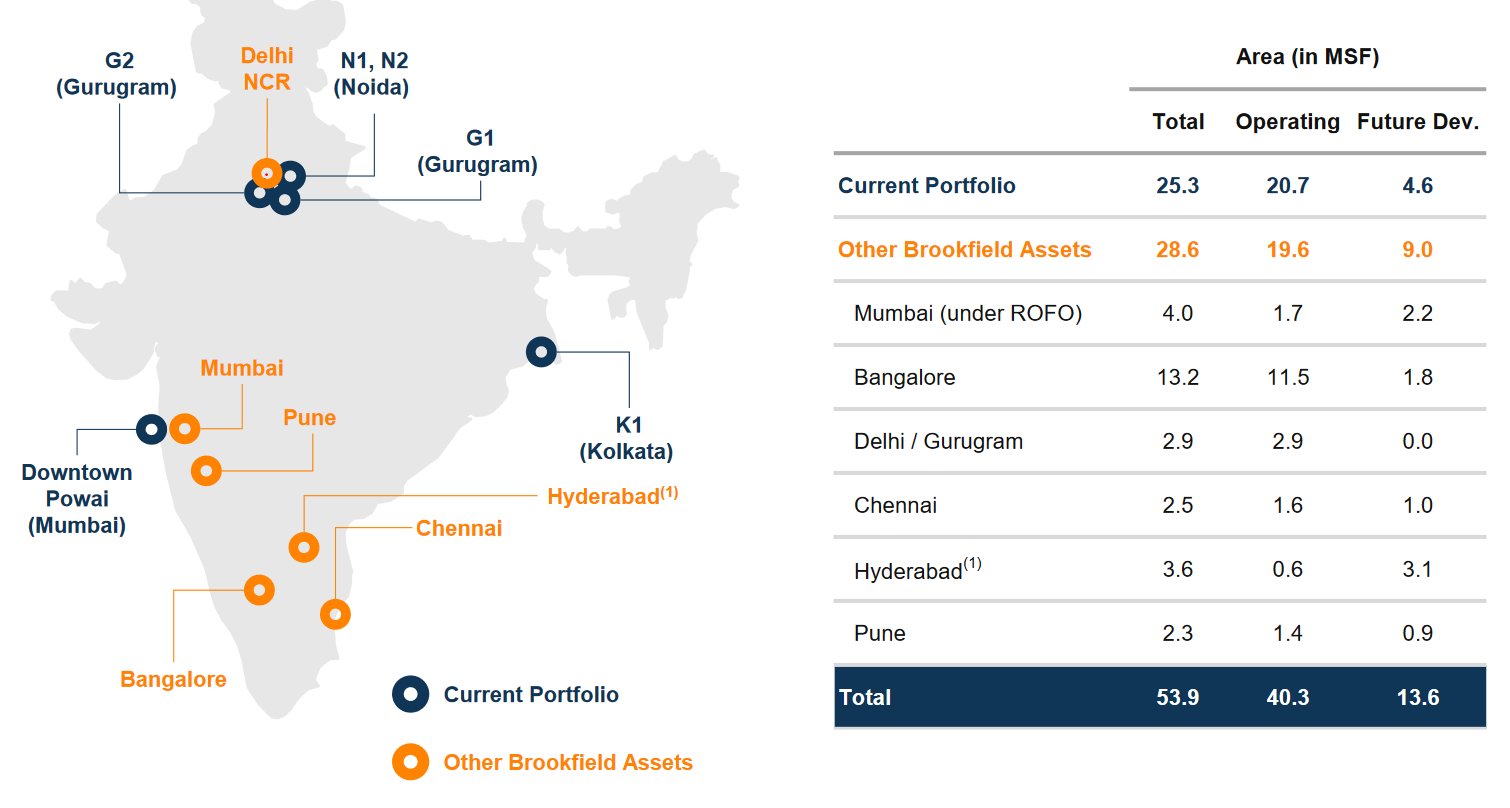

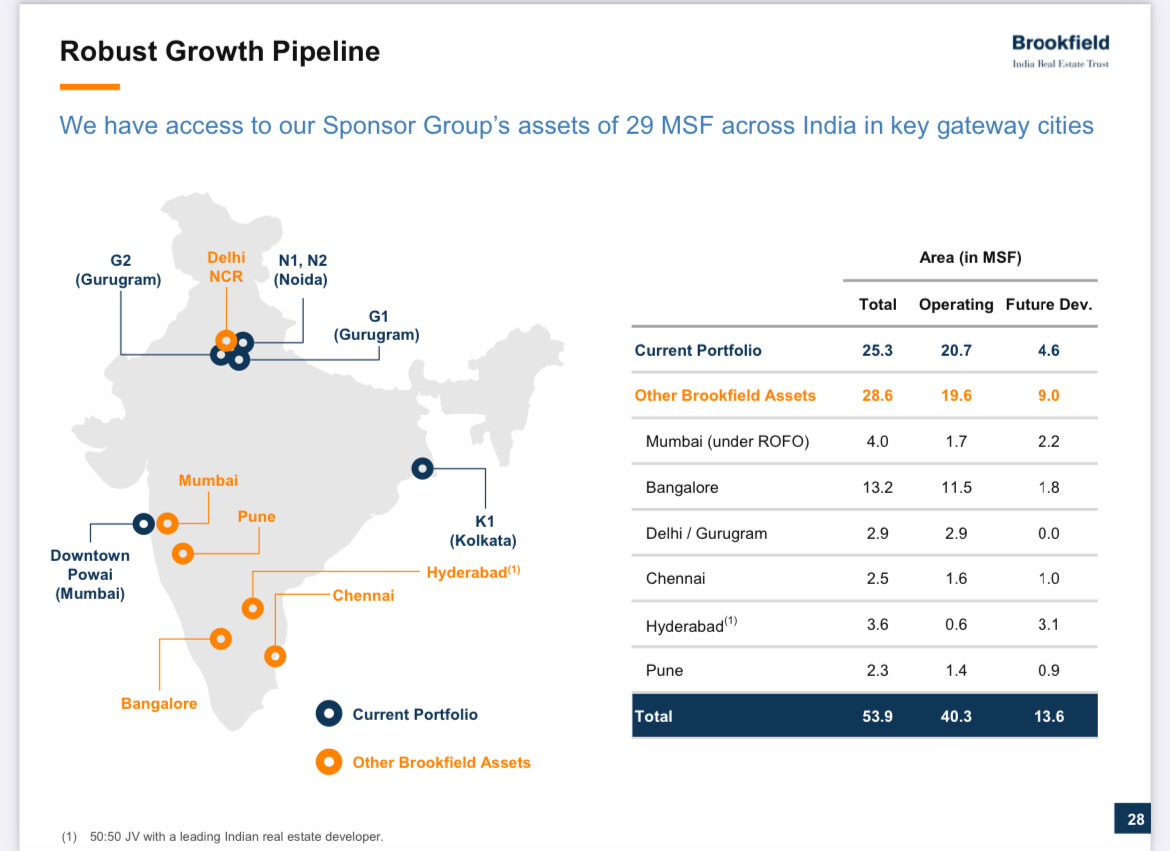

BIRET recently completed a Rs 2300 Crore fund raise through QIP. It has further plans to raise another Rs 1150 Crore, and these funds will be used to acquire 6.5 million sq ft of office space for BIRET for a total of $1.5 Bn in a 50:50 joint venture with GIC Singapore, resulting in a 35% increase in total leasable space and a 44% increase in operating area for the REIT.

Considering the recent raise via QIP were at a discount to CMP and the deep discount to the NAV of Rs 332, this could be an investment to consider for fixed income part of one’s portfolio.

Disclosure: Invested and will continue to add at deeper discounts.

Bro…thanks for starting this thread…I was interested in this as my workplace is owned by this only …I am only concerned here about few things in general as well as specific to Brookfield

Will it ever provide returns more than 7-8% per year in terms of income distribution?

and why this unit price is continuously going down…it’s bit concerning

To be fair all REITs/INVITs have been affected by the interest rate movements globally and in India. The office reits have also had to deal with reduced occupancy (WFH, Hybrid models) and now some slowdown in IT.

I think it can produce 7-8% on invested capital however my concern is the growth of DPU. While NOI can grow, there is a lag in DPU increase especially if there is a lot of debt or unit dilution

Disc: Invested

Directionally, like the thought process behind the acquisitions in partnership with GIC. It would take a while for the NOI growth to translate into increase in DPU for unitholders, so no instant benefit. Plus there has been dilution of units (normal for REITs)

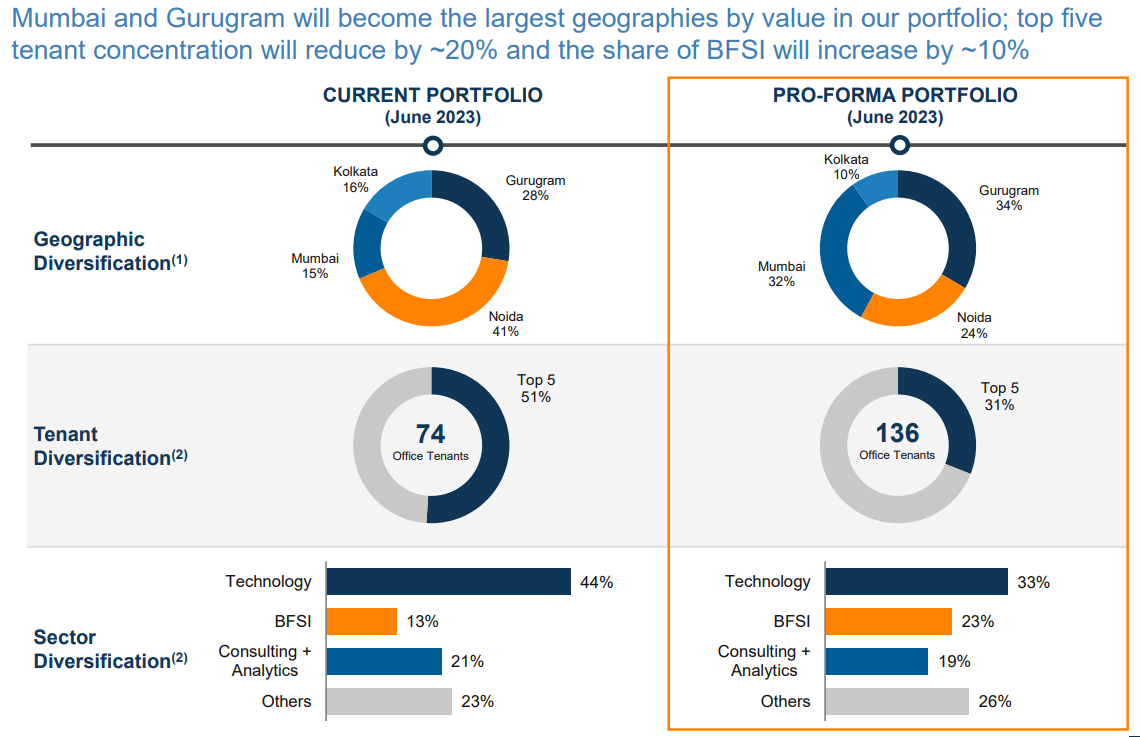

Adds scale in operating lease area

Expands presence in the financial hub of Mumbai

Diversification of tenant base in terms of sector (for BFSI now) and client concentration

Increases liquidity of units as large DIIs have now come in (mutual funds etc.)

Occupancy is now in mid 60%. Not sure whether WFH and flexi work will make it reach 90%

BROOKFIELD Concalls DEC 2023.pdf (1.4 MB)

The expansion strategy appears to be quite promising, with the potential to fuel growth in the upcoming years.

The REIT industry has been seen reducing occupancy levels to their SEZ properties because of the preferential income tax exemptions going away.

Brookfield has had dropping occupancy levels for many quarters and they have not been able to renew or sign up new leases to cover up for the expired leases

Plus they added debt to acquire properties jointly with their Singapore sponsor in AMJ/ JAS quarter. Also issued new units at 254 per share through QIP.

This reduced The Dpu per quarter from 4.8-5 range to 3.8 in JAS -CY23 quarter and to 4.4 in OND-CY23 Quarter.

However the government has made some changes to the SEZ policy by allowing demarcation of the area and allowing non SEZ tenants to take up space.

This will help the industry improve occupancy.

The amendment is yet to be formally notified so this may take 2-3 months.

While entire Listed REIT space is ignored since last couple of years, still among the listed REIT’s, Brookfield is most neglected.

I personally think REIT should have space in one’s fixed income protfolio, but market’s apathy seems to point in other direction.

For ME, fundamentally risk rewards in Brookfield are favourable at Rs 250 per unit, however, price action (technical indicators) signals that reverse is true.

Things that I dont like in Brookfield include:

Concentration of top tenants - Even after recent deal, top 4 tenants commands 35% of the space, which looks too much concentration.

Quality of Tenants - Top 5 tenants are IT services firms, which are very price sensitive. GCC’s in general offer much better tenant profile, as they are not price conscious and are reaady to pay up for better quality properties.

Income support from promoter - The distributions are supported by promoters as a large portion of the properties are vacant. This income support is available for next 1.5 years, post which, DPU will fall if vaccanies are not filled.

Under construction properties - are located in Kolkata which offers lowest rent.

Yes, it is only for newly acquired properties, but it constitutute 25% of distribution per unit. So, the income support is material when viewed from overall distribution.

I don’t think they have the luxury to go on an expansion spree in the near to medium term without pushing up leverage, which will lower Credit worthiness and Distributions further.

But do you think that REIT got compensated for taking on this risk. I assume that GIC bought 50% so REIT and GIC wouldn’t have been handed a raw deal by sponsor. As long as it is fair deal, it is not a concern. Also, Brookfield is viewed as professional as they are probably largest globally in this business.

Not sure how relevant this is for Indian Office Spaces / Commercial RE, as a growing economy can we consider ourselves to be immune to such issues in the medium run?

Here is a DPU track record of 3 office space REITs. None of them have given any appreciation in DPU since listing. I don’t think any of these are working for minority share holders. All their focus is either to increase their assets under management or benefit sponsors.

Embassy REIT:

First full year DPU (FY 2020): 24.39

TTM DPU: 21.33

Brookfield REIT:

First full year DPU (FY 2022): 22.1

TTM DPU: 18

Mindspace REIT:

First full year DPU (FY 2021-22): 18.79

TTM DPU: 19.2

To me it looks like a failed investment product yielding DPU in the range of 5-7% with no YoY appreciation. Given this track record, do you see any case for investment here?

Last year deal happened at 5000 crore EV. This year BIREIT buying at 6000. 20% appreciation appears on higher side. Ideally should have been appreciation of 8%, i.e. 5400 crore.

But when we look in context that BIREIT is not paying in cash but issuing units at Rs300 which is almost 20% premium of yesterday prices. This makes deal look good and probably BIREIT got it cheaper. Ideally should be positive for existing unit holders.