1.Britannia took price hike

2.palm oil price fell 50% from high in may-June

3. New products introduction

4. Every FMCG company given great result ITC NESTLE HUL

2 Likes

One thing evident in this mega inflation enviornment is that urban/premium is doing much better than rural…hence urban focussed FMCG faring better… Britannia seems to have a unique proposition here, their products are urban focussed but even in rural, plain biscuits can prove cost effective snacks/food . Similar thing was observed during lockdown etc. When biscuits everywhere in India seemed to substitute many food articles not readily available…in both urban and rural…

Disc. Invested since long…Not added since long because not sure about corporate governance but business seems solid hence could not exit also. Views maybe biased. I can be wrong in all my assessments and not eligible for any recommendations

2 Likes

This has been clarified by Management, that they borrowed 1000+ crore for Dairy unit capex, at a rate of 5.6%. And their treasury yields were much higher than this. This was put up in the latest tweet by Mangalam Maloo himself (author of the above original post)

1 Like

britannia and varun beverages leads the fmcg pack

1 Like

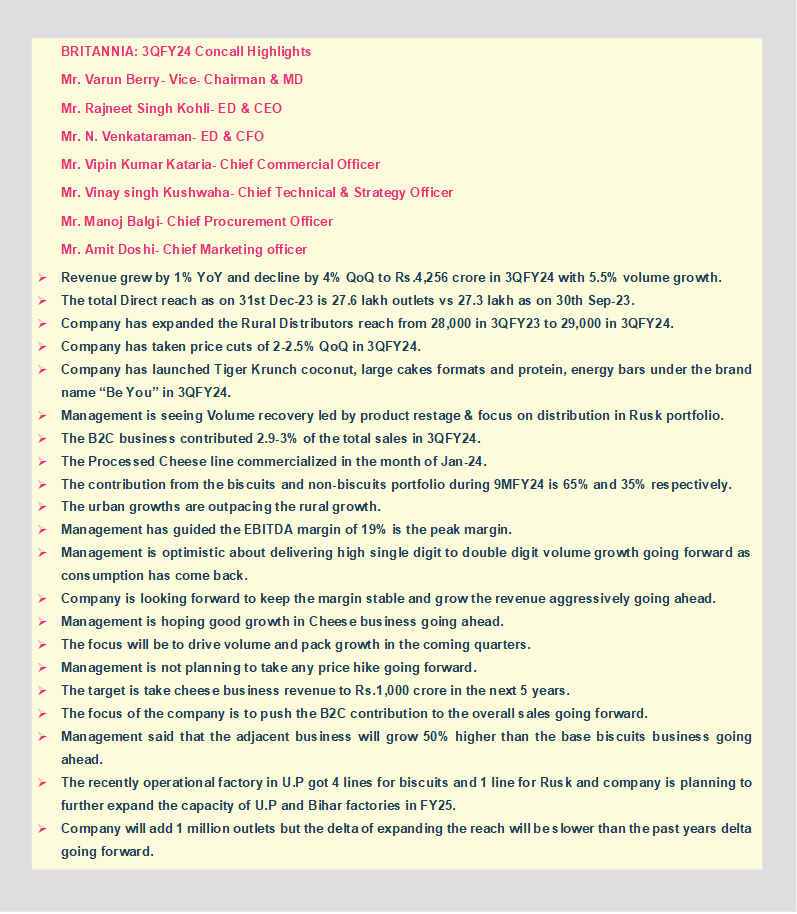

Britannia Q2FY24 Concall Summary

4 Likes

- Britannia Industries Ltd reported a 40% decrease in its consolidated net profit for the quarter ended December 31, 2023.

- The net profit amounted to Rs 556 crore compared to Rs 932 crore in the same period last year.

- Analysts’ expectations were not met, with a poll of six brokerages predicting a net profit of Rs 566 crore.

- Sequentially, Britannia’s profit slipped 5% from Rs 587 crore.

- Factors contributing to the muted growth include a high base effect, some price cuts, high competition, and low single-digit volume growth.

3 Likes

Britannia Industries Limited: Financial Overview for FY 2023-2024

Key Financial Metrics

- Revenue: The total revenue for FY 2023-24 was ₹16,186.08 crores, showing an increase from ₹15,618.42 crores in FY 2022-23.

- Net Profit: The company reported a net profit of ₹2,082.05 crores in FY 2023-24, compared to ₹2,139.30 crores in the previous year.

- Earnings Per Share (EPS):

- Basic: ₹22.01 for FY 2023-24 (FY 2022-23: ₹23.17).

- Diluted: ₹22.01 for FY 2023-24 (FY 2022-23: ₹23.17).

Financial Position

- Total Assets: The company’s assets stood at ₹8,370.84 crores by the end of March 2024.

- Equity and Liabilities: Total equity was ₹3,527.52 crores and total liabilities were ₹4,843.32 crores as of March 2024.

Ratios

- Debt-Equity Ratio: 0.58 in FY 2023-24, which suggests a healthy balance between debt and equity financing.

- Net Profit Margin: 13.32% for FY 2023-24, indicating the percentage of revenue that constitutes the net income.

Dividend

- The Board recommended a final dividend of ₹73.50 per equity share for FY 2023-24.

Auditor’s Opinion

- The financial statements received an unmodified opinion from the auditors, indicating that they present a true and fair view of the company’s financial condition and operations in accordance with applicable accounting standards.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/0800ba05-cd8a-4c42-b8d4-6db25227a1f4.pdf

2 Likes

Few of my takeaways from Q1 FY25 of Britannia Industries

𝐂𝐨𝐫𝐩𝐨𝐫𝐚𝐭𝐞 𝐓𝐫𝐚𝐣𝐞𝐜𝐭𝐨𝐫𝐲:

- Revenue grew 4% year-over-year to INR 4,130 crores, with volume growth of 8%

- Operating profit increased 10% to INR 680 crores, with margins at 16.5%

- Rural markets showing signs of recovery, with rural growth outpacing urban

- Focus on driving topline growth even if it means slightly lower margins in the near-term

𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐁𝐥𝐮𝐞𝐩𝐫𝐢𝐧𝐭:

- Continuing distribution expansion, especially in rural areas and Hindi belt states

- Implementing sales transformation project with Bain & Co to improve efficiency

- Investing in brand building and innovation, launching new products like Pure Magic Stars

- Scaling up adjacency businesses like dairy, with focus on cheese and beverages

- Expanding manufacturing footprint with new facilities coming up in UP and Bihar

𝐌𝐚𝐫𝐤𝐞𝐭 𝐃𝐲𝐧𝐚𝐦𝐢𝐜𝐬:

- Recovery in rural demand after prolonged slowdown

- Premiumization continuing across portfolio

- Focus on innovation and new product launches

- Expansion into adjacent categories like dairy and snacks

Industry Tailwinds:

- Improving rural sentiment and consumption

- Moderation in inflation compared to previous years

- Growing preference for packaged and branded food products

Industry Headwinds:

- Inflationary pressure on key commodities like flour, sugar, and cocoa

- Intense competition, especially from regional players

- Downtrading in certain markets to cheaper alternatives

𝐈𝐧𝐯𝐞𝐬𝐭𝐨𝐫/𝐀𝐧𝐚𝐥𝐲𝐬𝐭 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬:

- On slower pace of distribution expansion: Management emphasized weighted distribution growth and focus on extraction from high potential outlets

- On margin pressure: Company prioritizing topline growth over margin expansion in near-term

- On dairy business profitability: Gross margins in line with overall business, but depreciation impacting net profitability

Competitive Landscape:

- Continuing to gain market share, albeit slowly

- Large gap with market leader (50% share vs Britannia’s 18%) provides headroom for growth

- Facing competition from both large national players and regional brands

𝐅𝐮𝐭𝐮𝐫𝐞 𝐏𝐫𝐨𝐣𝐞𝐜𝐭𝐢𝐨𝐧𝐬:

- Targeting high single-digit to double-digit volume growth

- Expect 4-5% inflation in coming months, may take some pricing actions

- Focus on driving topline growth even at slightly lower margins

𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐃𝐞𝐩𝐥𝐨𝐲𝐦𝐞𝐧𝐭:

- Investing in manufacturing capacity expansion

- Continued investment in brand building and innovation

- Scaling up adjacency businesses like dairy

Opportunities & Risks:

Opportunities:

- Rural recovery and distribution expansion

- Growth in adjacency businesses like dairy and snacks

- Premiumization across portfolio

Risks:

- Commodity price inflation

- Intensifying competition

- Potential economic slowdown impacting discretionary spending

𝐂𝐨𝐧𝐬𝐮𝐦𝐞𝐫 𝐏𝐮𝐥𝐬𝐞:

- Rural demand showing signs of improvement

- Some downtrading observed in certain markets

1 Like