This is a valid point.

I also have not understood the rationale of raising funds through debentures and increasing the dividend payout to almost 200%.

Debt / Equity ratio looks high above 1.5 due to this, I believe.

I am not sure whether I have missed any thing here.

As FMCG business, one would expect it to be debt free company or with minimal debt, and still able to grow at reasonable rate of 8-10%.

Is their business model different from other FMCG companies? I woud like to know more on this.

Disc : Invested but finding it difficult business to understand.

Britannia distrbiuted bonus dividend carrying 8% and 5.5% annual coupon. The interest paid on bonus deneture would be tax deductable for company, while dividend/interest received by Indian minority shareholders would taxable at marginal rate. Hence, as compared to pure dividend cash payment, paying dividend through bonus debenture have some tax advantage to company with no difference for Indian shareholder in my limited understanding.

Discl: I have tiny investment (less than 0.5% of my equity portfolio) in the company. My view may be biased. Not recommeding any stock action and also my understanding may be incorrect about taxability point.

That could be the logical way of looking at it.

I am not sure whether this is good practice or not, but probably could be the management thought process.

I generally like to invest in debt free business as much as possible, hence this D/E ratio of 1.5 was my concern.

India’s biggest biscuit maker Britannia has appetite for acquisitions_ - www.ft.com.pdf (2.3 MB)

Takeaway: High inflationary environment is weeding out weaker players in FMCG segment across world which makes them takeover targets for large companies like Britannia.

RM inflation to continue and volume growth to dip going forward for few quarters.

Disclaimer: Invested with a 4% allocation to my current PF.

Business is currently available at higher dividend yield than ITC . It’s FMCG margins are also much ahead of ITC. What remains to be seen is for how long pain will remain. Is it a possibility we can buy this at 6% yields ?

Disc: Invested in both.

How did you get 5% yield? May be one time dividend. They are paying around 75 rs which is 2.5%. ~75 is their cash EPS so they can not pay more unless there is one time dividend from cash balance. But again not sustainable. 2.5% sustainable dividend is best one can expect.

Dividend payout was more than 200% for last FY which was exceptional one and we can expect only regular dividend payout of 60% or less. So I expect dividend may be less than 2% at CMP of 3170 if EPS is 60 for this FY on conservative basis. Stock price fell down a lot from top and looks reasonably valued now however still current PE 50 is more than median PE which is 45.

Disc : In my watchlist

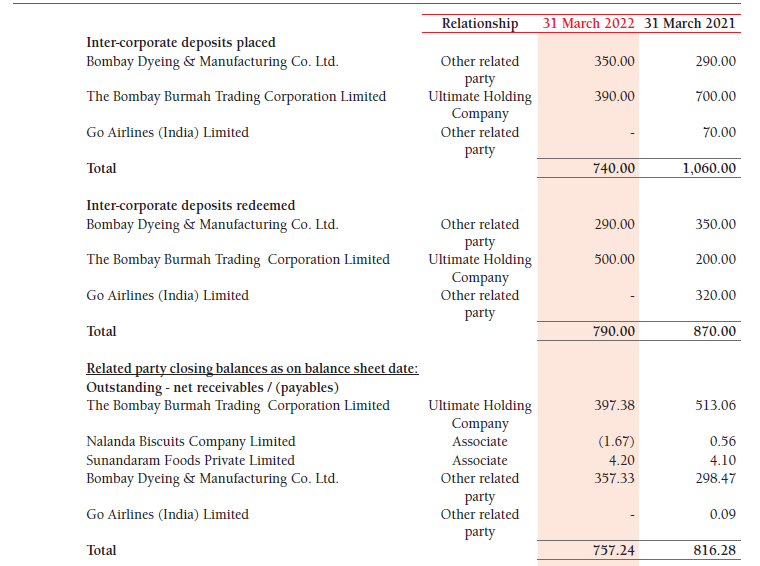

Did you take into account the NCDs as well?

2020-> 118

2021->84 something.

Q2FY22-23

Conference Call

Transcript

Financials

Related Party Transactions

Surprising how they could pull off such a show when the whole world is complaining of inflation. May be if someone can put concal call notes, would be interesting

I would suggest some caution to anyone tracking Britannia because of Wadias and their shenanigans in Bombay Dyeing. They might be cooking books in Britannia as well.

There’s never just one cockroach in the kitchen - WB. Exited.

I believe that, though results look rosy, an investor community should wait for the conference call transcript and presentations before coming to any conclusion.

Also, one can read latest ICRA and CRISIL reports which are available for understanding of related party transactions.

There could be doubts due to the earlier Management record or transactions but one should study all the things in detail. One of the reasons for better margins could be due to price hikes which were taken during April-June and also during July-September quarter which might be reflecting now with lagging effect.

Also, as per Management, they have gained market share which is now at 15 year high level, aided by new product launches like Crosissants, NC Seeds and Herbs, Biscafe, Potazos, 50-50 Golmaal, Marble cake, Muffils across geographies. Due to pricing actions and intensified cost efficiency program, they have been able to improve margins beyond pre-COVID levels.

Disc : Invested and User of New Britannia products like Crosissants apart from old products. Views could be biased.