Nowadays I see lot of people at airports travelling with Tommy travel gear. The trend of using luggage as an accessory and that too as a fashion accessory is still in its infancy stage. When people have met their basic needs, they do spend on such stuff. I see a lot of scope here as a shift to luxury in the luggage segment.

5 Likes

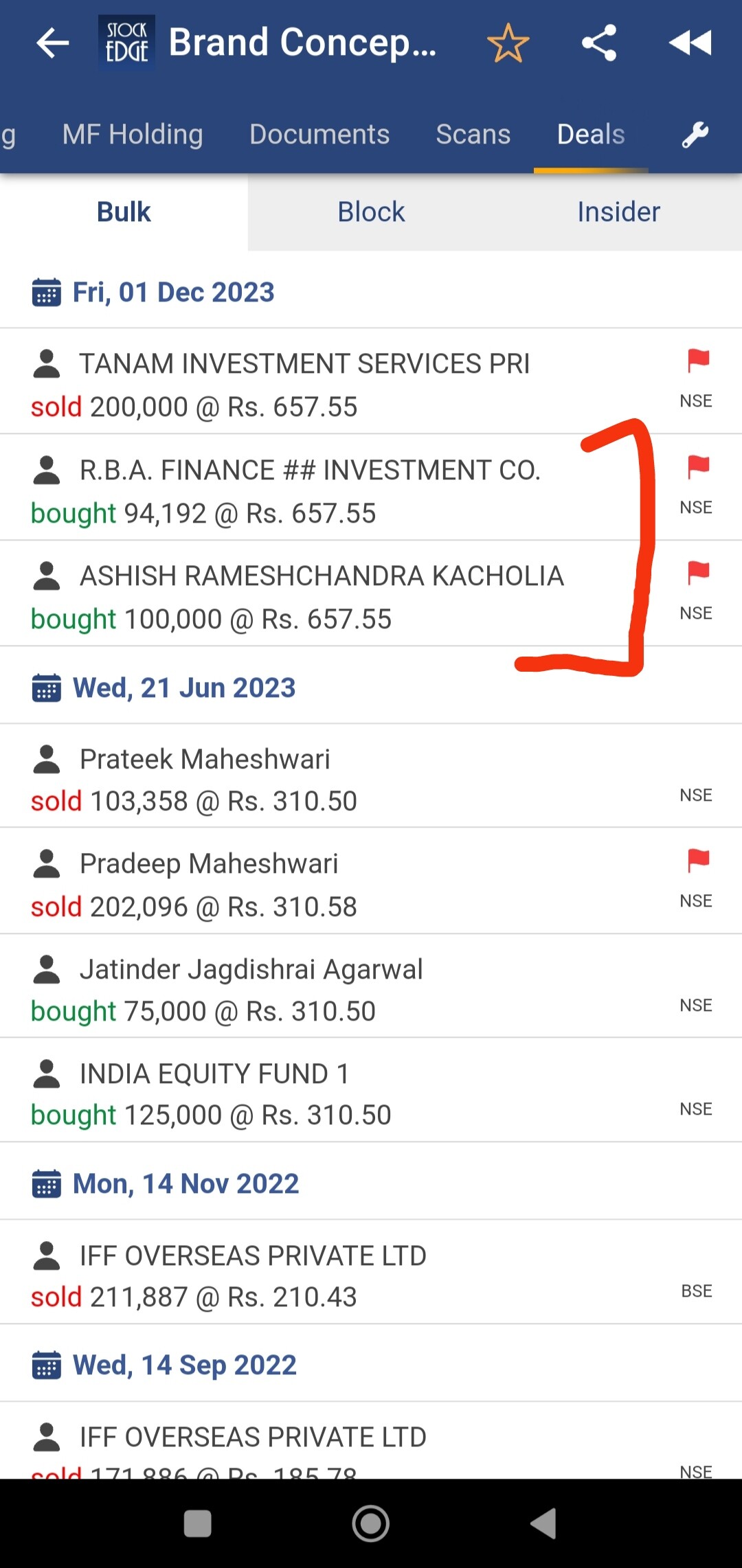

Mr Ashish Kacholia bought a small stake in Brand Concepts.

Now a lot of people who were sceptical will re-think.

It’s not that these marquee investors are always right but their mental models and calculations generally lead them to right companies.

4 Likes

Straight forward answer

General business + Corporate Sales

Corporate Sales are doing good which management gave answer in concall

A friend who recently visited a Bagline store shared the images. Guess is the new brand available at Bagline stores. Priced in 10k to 15k range. The sales of Guess,once they take off are likely to significantly increase the revenues.

Yet to find out if they making themselves or just selling like many other retailers selling Guess products.

5 Likes

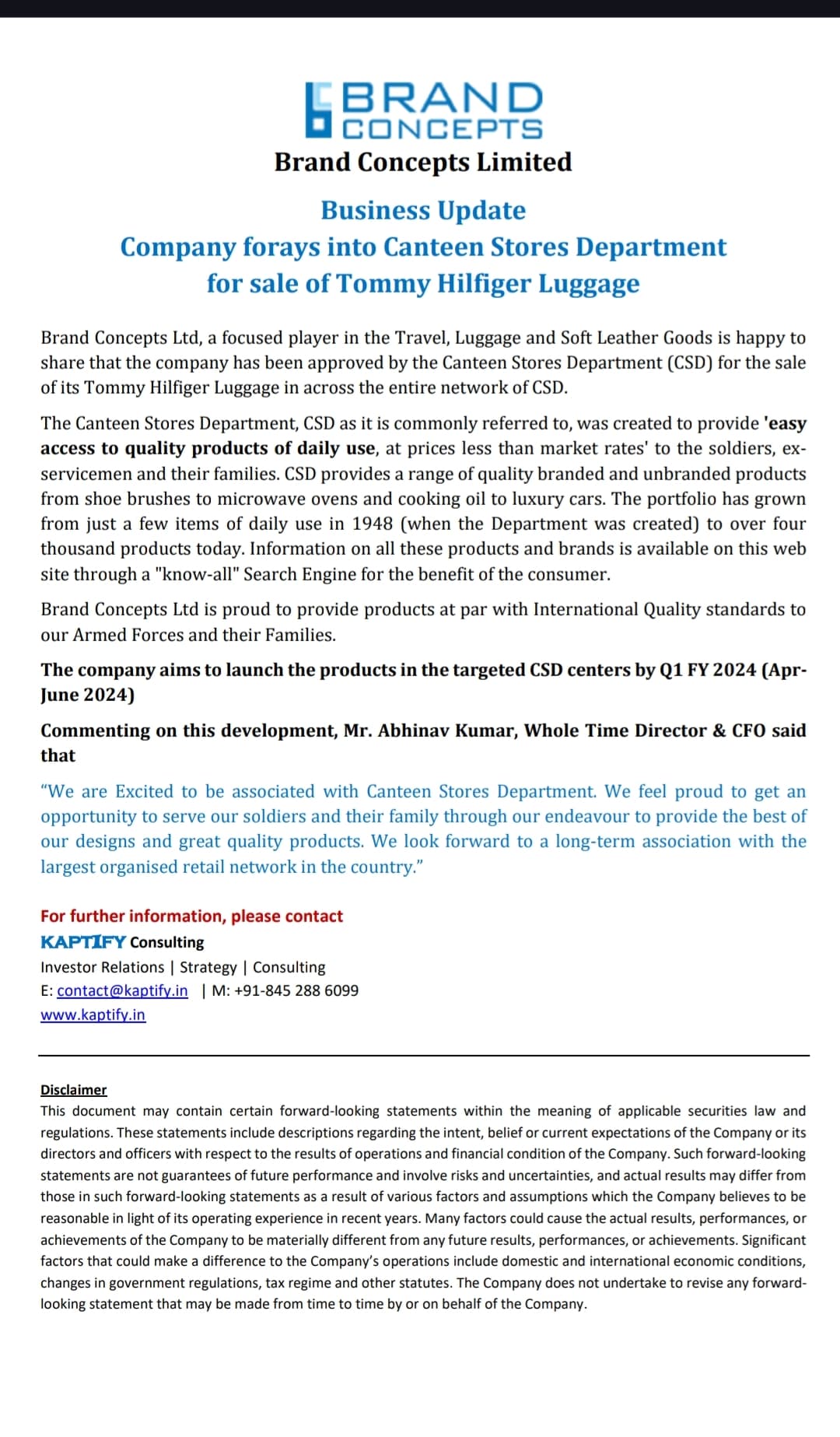

Any news about Tommy Hilfigure licence renew…

5 Likes

https://www.bseindia.com/xml-data/corpfiling/AttachLive/6959d7a7-4ce9-486c-804f-5258521fff3c.pdf

Licence has been renewed for next 3 yrs.

1 Like

not sure, maybe just selling I guess since their manufacturing is mostly in backpacks.

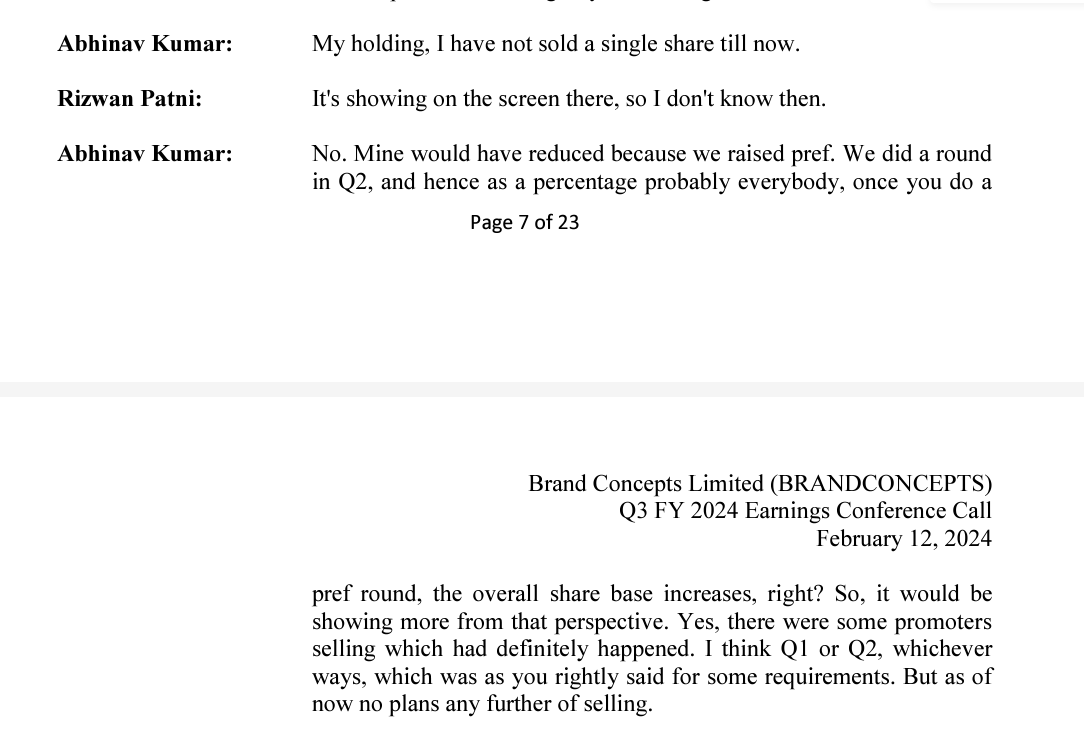

Promoter holding decreased by a certain % ,along with this Mr.avinav kumar .

Can anyone come up with the reason , why ?

51.24% - 48.81% QoQ

Company might be doing it to avoid debts and it might be just cash management for future growth

If one needs to be cautious , he should be cautious when Abhinav Kumar stakes are decreasing

1 Like

Abhinav kumar stakes decreased from 7.21 to 6.85 in 3 quarters. Need to be cautious or it’s ok.

He has full skin in the game, it’s capital intensive business & co is in expansion mode, so dilution will come automatically as promoter stake decreases as per ratio AK’s share % will decrease as well whether he sells a single stock or not,

2 Likes

If the Investment decision is based on someone selling stake, then the entire investment process is flawed. I remember Genomal Family continuously reducing stakes when the company was in expansion phase. Still the Company rewarded the patient investors handsomely.

3 Likes

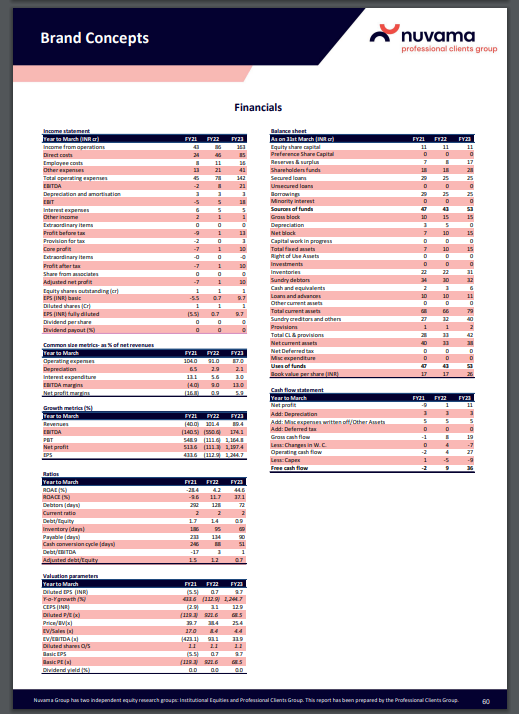

Any idea why such de-growth in March 2024 in net profit (around -64%)?

1 Like

Due to esop expenses of 54 lakh , pre-operating expenses of new manufacturing plant (hard luggage) , Trade shows & new launches , commissioning of new office in indore , A&P & marketing , subdued demand in retail segment as a whole so no economies of scale.

*as per management in Q4 concall

5 Likes

After hearing two concalls , management seems to be honest. ceo is quite frank in admitting his faults.