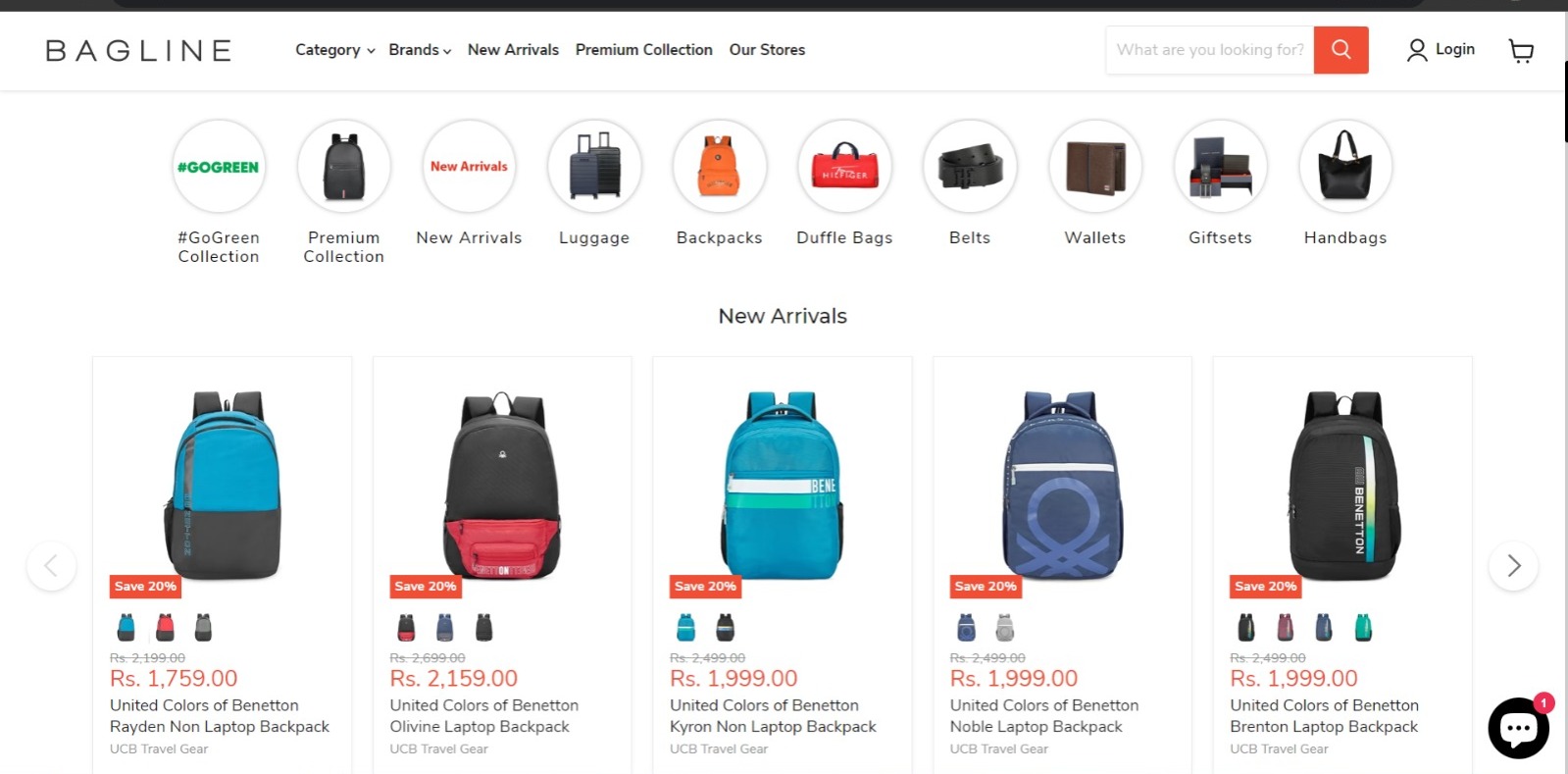

Brand Concepts Ltd specializes in the manufacturing of bags, backpacks & fashion accessories for the Indian & International markets.

KEY POINTS

Business Model

The Company enters into franchise or trademark license agreements with reputed brands.

Analyses the brand and other factors and creates a product design, a sample is manufactured and on approval from the brand it outsources its manufacturing activities to the manufacturers located in India and China (majorly).

They have exclusive rights for Tommy helgifer and United colour of Benetton. Guiding for 30+ percent growth for next few year.

KEY POINTS [ edit ]

Business Model

The Company enters into franchise or trademark license agreements with reputed brands.

Analyses the brand and other factors and creates a product design, a sample is manufactured and on approval from the brand it outsources its manufacturing activities to the manufacturers located in India and China (majorly). [1]

Products

The Co. manufactures trendy backpacks like laptop bags, duffle & gym bags, rucksacks and school backpacks. Handbags, Clutches, Men’s belts & wallets, Luggage Bags etc. [2][3][4][5]

Clientele

The company works with brands like Tommy Hilfiger, AND, Global Desi & HEAD and also sells its in-house brands Sugarush and The Vertical. [6]

Distribution Channel

The company has an omni channel presence operating through a mix of Company owned company operated outlets (COCO – 8) and Franchisee owned outlets (FOFO – 22) and 30 EBOs. It sells its products to several MBOs/Retail and is systematically moving to a master distributor model across all zones / cities to reduce working capital in the business. [7]

Online Presence

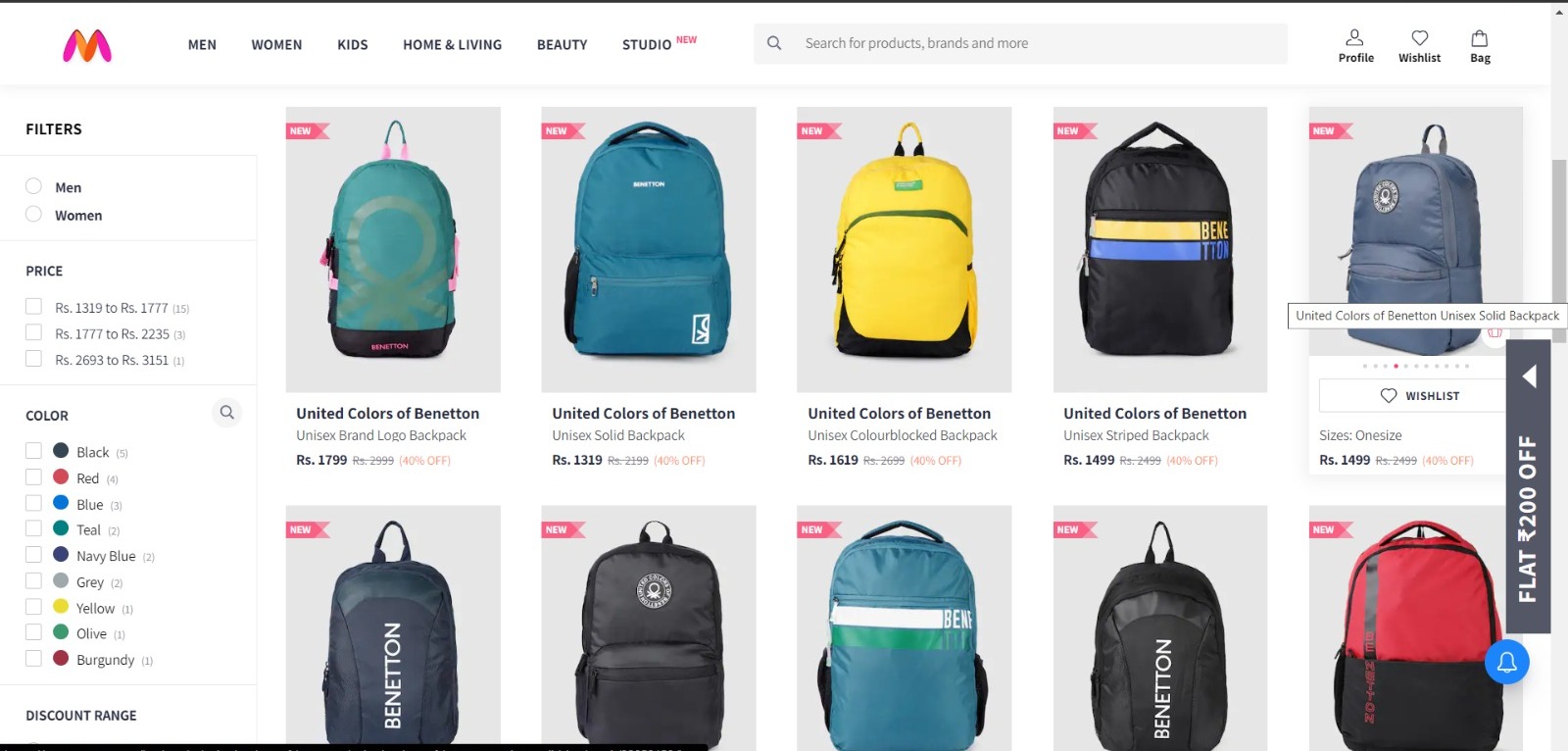

The company sells through several Ecommerce platforms such as Myntra and Amazon [8]

It also has developed the website www.baglineindia.com for sale through e-commerce. The physical stores of BCL also go by the name of “BAGLINE”. [9]

Channel Distribution

Online : 58% in FY21 vs 30% in FY20

LFS(Large Format Store): 7% in FY21 vs 30% in FY20

CFS: 17% in FY21 vs 17% in FY20

COCO: 5% in FY21 vs 7% in FY20

FOFO(Franchisee Owned Company Operated) : 5% in FY21 vs 8% in FY20

DND: 7% in FY21 vs 8% in FY20 [10][11]

Focus

The Co plans to expand presence in Tommy Hilfiger by scaling up existing MBOs and EBOs. In SUGARUSH brand the co. plans to grow its offerings and presence through MBOs, EBOs and Bagline stores. The company is planning to add 2-3 new international brands (FILA, VANS, ZARA, etc.) for exclusive licensing for India in their focus categories, setting up its own manufacturing of luggage category. [12][13]

**Investing in a company like Brand Concept can be a risky proposition. Here are some of the reasons why:

The company may not be able to secure the exclusive rights to sell the product in India. This could happen if the brand owner decides to sell the product through other channels, or if the company is unable to negotiate a favorable contract with the brand owner.

- The company may not be able to market and sell the product effectively. This could happen if the company does not have the right marketing channels, or if the product is not well-suited for the Indian market.

- The company may not be able to generate enough revenue to cover its costs. This could happen if the product is not popular, or if the company’s marketing and sales efforts are not successful.

Here are some of the potential benefits of investing in a company like Brand Concept:

- The company could be very successful if it is able to secure the exclusive rights to sell a popular product in India. This could lead to significant profits for the company.

- The company could gain a valuable foothold in the Indian market. This could give the company a competitive advantage if it decides to expand its product offerings in the future.

-

The company could learn valuable lessons about the Indian market. This knowledge could be used to launch other successful businesses in India.

MAY 23 Quarter concall highlight

New Brands:

- Signed up two new brands, United Colors of Benetton and Aeropostale

- Exclusive licensee for UCB in India for all channels and regions, including their own stores

- Aims to sign two new brands within the current financial year

- Target audience of Tommy Hilfiger are those who aspire to wear the brand, not those who are not aware of its positioning

- Aims to be more inclusive rather than exclusive in its brand positioning, with Benetton being more affordable and Tommy Hilfiger thriving on exclusivity

- Aims to have one brand in the bridge to luxury segment and another in the mass-premium space

- Company plans to enter lower price segments with brands like UCB and Aeropostale

- Aims to enter the lower price point segment with new brands to unlock value

Product Development:

- Starts product development after signing the agreement with a brand

- Process of designing, sampling, and production for new products takes approximately 7 to 9 months

- Aeropostale is expected to hit stores before UCB

Store Expansion:

- Target is to have 50 stores by the end of the year

- CapEx for a franchisee store is around 40-50 lakhs, including stock investment and rent deposit

- Company is free to open UCB Travel Gear exclusive stores

- Company plans to invest in its own stores in top locations and take a franchisee route for Tier 2 and Tier 3 locations

- Company plans to steadily grow its number of stores, with a focus on good locations and potential airport stores

- Underpenetrated in terms of distribution and plans to increase its number of distributors and large format stores

- In talks with large format stores to enter with new brands, including UCB and Aeropostale

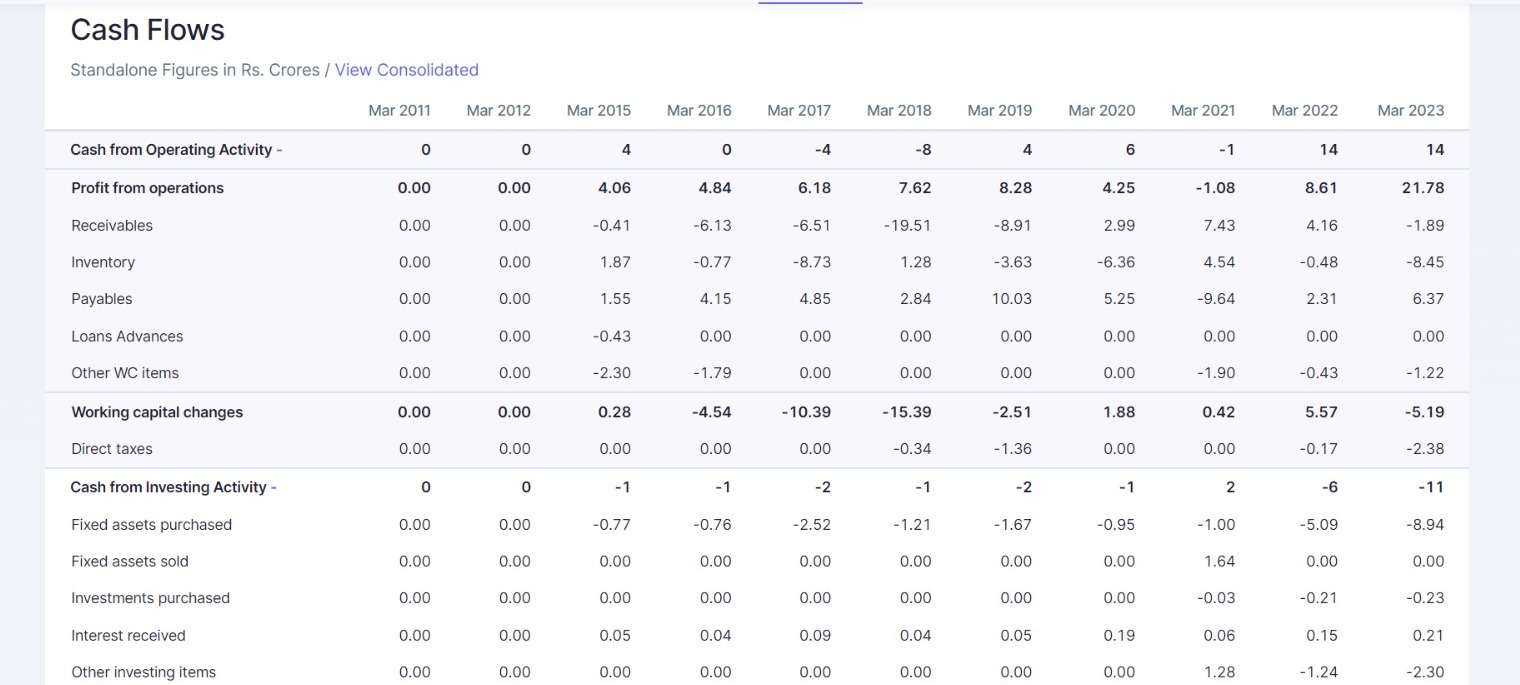

Financials:

- Gross profitability has increased, but contribution has gone down due to increased selling distribution expenses from marketplace activities

- Company is financially prudent and aims to maintain its current levels of profitability while expanding

- Marketing spend will not be high as the company is a licensing company and not focused on building brands from scratch

- Company spent about Rs. 3.13 crores on marketing in FY23, and marketing spend is expected to remain under 5% in the future

- Company’s margins are slightly better in e-commerce, and almost 16-17% of overall sales in FY23 came from their own marketplace

- Contribution from lower-priced brands will be lower but EBITDA margins will remain the same

- Channel margin of 50% includes GST, which is 18% in the company’s case

Market and Competition:

- Travel gear market in India is estimated to be between Rs. 24,000 crores to Rs. 50,000 crores

- Organized travel gear market is around Rs. 5,000 crores to Rs. 6,000 crores

- TH is positioned in the Rs. 500 crore to Rs. 700 crore market, while UCB and Aeropostale are in the Rs. 2,000 crore to Rs. 2,500 crore market

- There is no syndicated study for the Small Leather Goods segment

- Tommy Hilfiger is the market leader in small leather goods in all channels of operation, positioned as a premium brand

- Sees a huge opportunity in India as a manufacturing sourcing hub for brands shifting from China

Merger and Quality Assurance:

- Merger of the company with its overseas promoter is in process and will be effective from April 2024

- Company is setting up a new department for quality assurance and has started offering international warranty on its bags

Sales Mix:

- Sales mix currently consists of 46% Small Leather Goods, 43% Travel Gear, and 11% Women Handbags & Accessories, but the company expects Travel Gear to increase in the future

- Tommy Hilfiger contributed to about 80-83% of overall sales, with some sales coming from discontinued brands like AND and Global desi

- Primary wholesale billing for all sales, including at large format stores

CapEx and Manufacturing:

- CapEx for hard luggage manufacturing is expected to be around Rs. 15-17 crores, and the company plans to occupy 50% of the capacity of the merged entity

- Plans to manufacture 50% in-house and 50% through contract manufacturing

recently added UCB product in BAGLINE INDIA

Anti-thesis pointers for Brand Concept

-

The company may not be able to secure the exclusive rights to sell the product in India. This could happen if the brand owner decides to sell the product through other channels, or if the company is unable to negotiate a favorable contract with the brand owner.

-

The company may not be able to market and sell the product effectively. This could happen if the company does not have the right marketing channels, or if the product is not well-suited for the Indian market.

-

The company may not be able to generate enough revenue to cover its costs. This could happen if the product is not popular, or if the company’s marketing and sales efforts are not successful.

-

The company may be faced with competition from other companies that are also selling the product in India. This could make it difficult for the company to gain market share and generate profits.

-

The company may be subject to government regulations that could impact its ability to operate in India. These regulations could change over time, which could make it difficult for the company to stay compliant.

-

The company may not have a strong track record. This could be a red flag for investors, as it suggests that the company may not be able to successfully execute its business plan.

-

The company may not have a clear competitive advantage. This could make it difficult for the company to stand out from its competitors and attract customers.

dis:invested