I’m surprised that there isn’t a thread on FirstCry already so will try to share everything as per my understanding and hoping for informative feedback from the community.

Introduction

FirstCry was founded via Brainbees Solutions Ltd. in 2010 and the FirstCry platform was launched in India with the goal to create a one-stop destination for parenting needs.

FirstCry stands as India’s largest omni-channel platform for mothers’, babies’, and kids’ products. It drives revenues primarily through its robust India multi-channel retail model, and the company has expanded internationally to UAE (2019) and KSA (2022), and diversified into adjacent segments through GlobalBees for leveraging brand recognition capabilities and Intellitots for early childhood education.

The Complete Business Model

The four business segments described by the Managing Director & CEO, Mr. Supam Maheshwari -

“The first one is our core ‘India multi-channel business’ segment, which has been at play for last 13+ years from the beginning and that consists of our online India as well as our 1000+ offline stores and our distribution, the new small sub segment that we started recently. These are the key drivers of our India multi-channel that constitutes to drive our India multi-channel business and this is a core and the first sort of a business segment which drives a large part of our revenues. The second business segment is international, which is a same playbook of India, we took it to UAE and then subsequently to KSA. So UAE and KSA put together constitute our second business segment, which is ‘International’. The third business segment is ‘GlobalBees’, which is an initiative, a company that we incubated 3 years back, May 21, and the fourth one is a smaller business segment that we operating which is called ‘Others’ in our RHP and essentially it is the preschool business that is an asset like preschool business. So these are the four business segments that we will talk about during the course.”

1. India Multi-channel : FirstCry

Leveraging deep customer insights, data analytics, in-house design and development capabilities, and the strong “FirstCry” brand, the company offers a broad assortment of products from third-party Indian brands, global brands, and its own home brands.

The integrated multi-channel retail model combining sales from Online platform, FOFO stores, COCO stores and General Trade Distribution -

I’m not sure about the General trade sub-segment that they’ve started as there’s not much information about it, but I think it is regarding the sale of diapers through general trade. Globalbees acquired a majority stake in Swara Baby Products and Solis in 2021 to strengthen and scale the in-house diaper manufacturing.

Total brand outlets as on March 2025 - 1,156

Out of this 45% are BabyHug or FirstCry COCO stores.

The no. of FOFO stores have been slowing down over the past 3-4 years while COCO stores have been growing faster.

- 527 COCO (296 BabyHug + 231 FirstCry) stores

- 629 FOFO stores

- 78% of the total GMV comes through online channel and rest 22% from offline retail outlets

- 8,000+ brands sold across channels

- 55% of the total GMV sale from own home brands

Home Brands - basically private label brands of the company that help generate higher gross margin than selling third party brands. 55% of the total GMV in FY 2025 came from the home brands and these home brands are not available on any other marketplace. Share of home brands is significantly up from 37% in FY 2021. One of the home brands, BabyHug is the largest multi-category mothers’, babies’ and kids’ products brand in India by GMV.

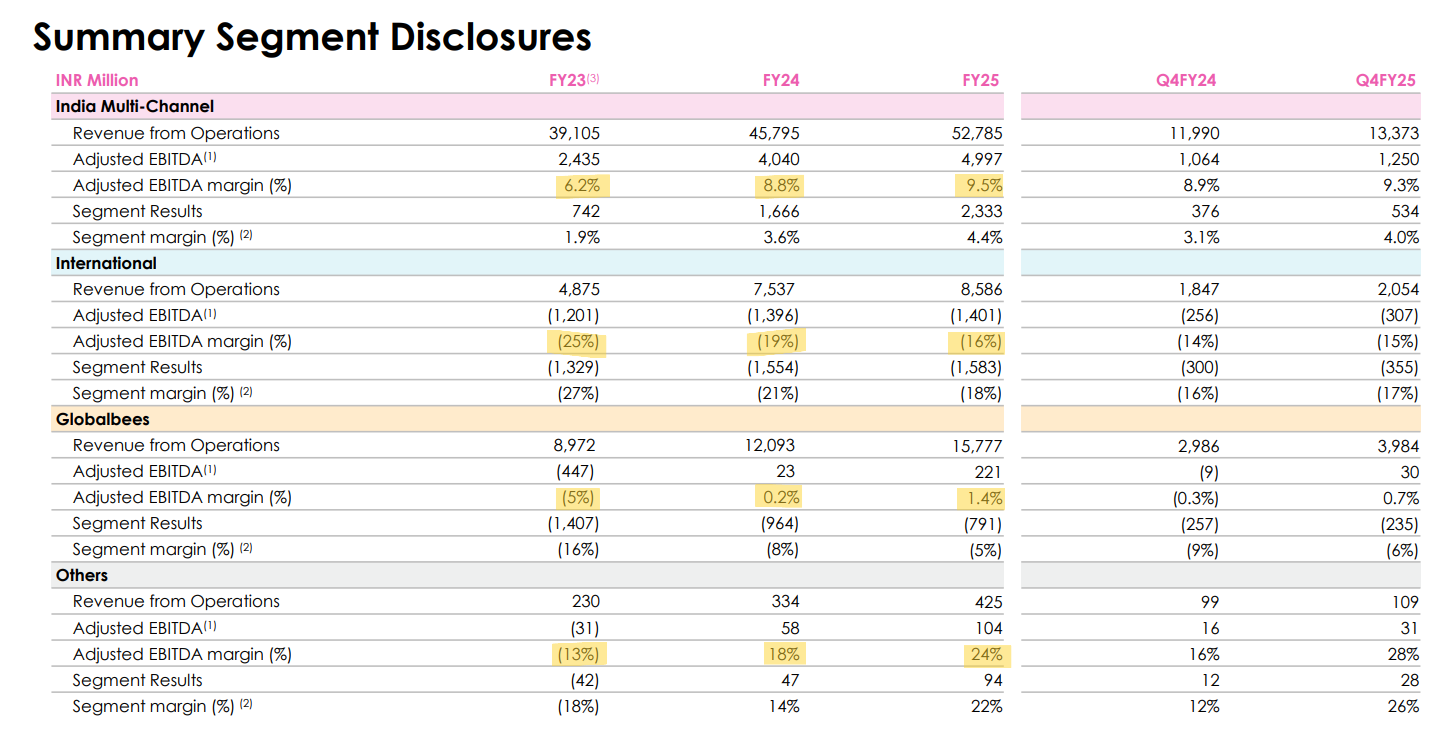

Segment Financials :

FY 2025

Revenue - ₹5,278 Cr. ![]() +15%

+15%

EBITDA - ₹500 Cr. ![]() +24%

+24%

Q4 FY2025

Revenue - ₹1,337 Cr. ![]() +12% YoY

+12% YoY

EBITDA - ₹125 Cr. ![]() +17% YoY

+17% YoY

AUTC crossed 1 Cr. (+17% YoY)

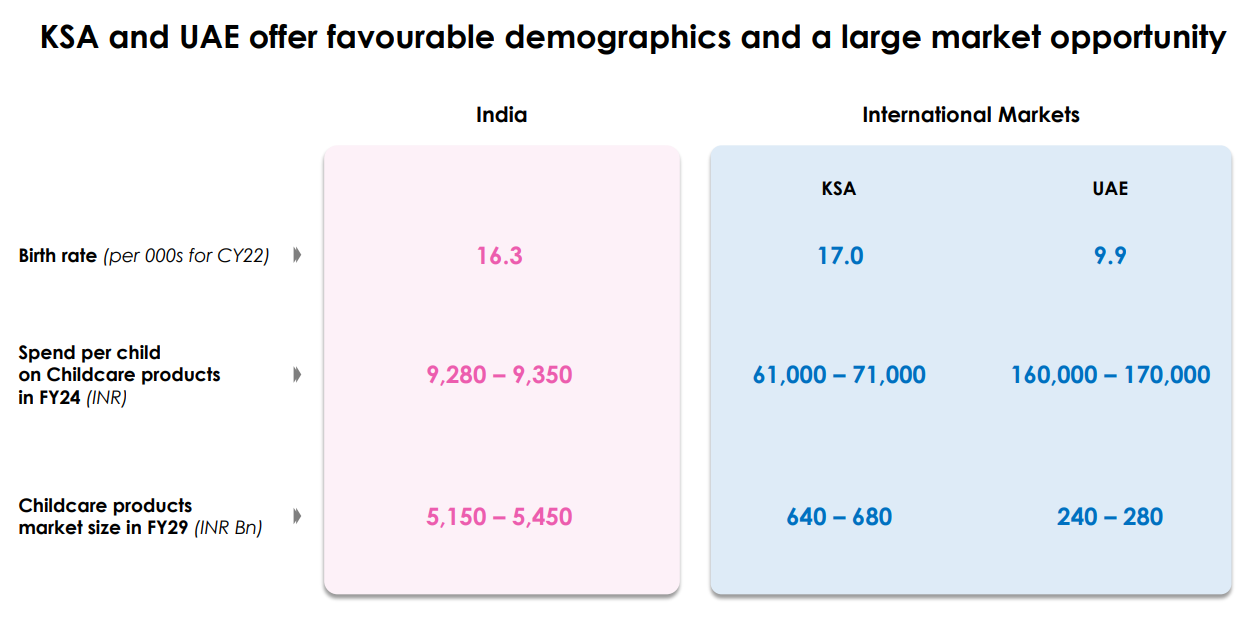

2. International Business : UAE and KSA

Leveraging their India playbook and with an online-first approach, the company entered UAE in Oct. 2019 through its wholly owned subsidiary FirstCry Management DWC LLC and expanded to KSA in Aug. 2022

At present, they operate exclusively as an online e-commerce platform in both the markets. In future UAE will remain only an online play, while KSA will see a replication of multi-channel approach as seen in India.

Their rationale for entering middle eastern markets?

- Management is very confident about capturing the Middle East market by replicating their successful India playbook

- Lack of childcare focused vertical players in the Middle east markets just like India

- High birth rates and 7-8 times higher per-child spending compared to India

- AOV in the Middle East exceed India’s by 4 times

- Launched middle eastern specific home brands

Segment Financials : the only loss making segment

FY 2025

Revenue - ₹858 Cr. ![]() +14%

+14%

EBITDA - (₹140 Cr.)

Q4 FY2025

Revenue - ₹205 Cr. ![]() +11% YoY

+11% YoY

EBITDA - (₹30 Cr.)

EBITDA margin in FY25 improved from -19% to -16%

3. GlobalBees : D2C

This is the fastest growing business vertical of the company. However, I personally find this segment very unsettling because it needs near perfect execution skills to scale so many brands in their own niche under a single consolidator and there’s no other large scale player in this segment.

Within a short span, GlobalBees has emerged as the largest and the only profitable player in the D2C roll-up company. GlobalBees acquires and invests in digital-first consumer brands across categories. It then uses the parent company’s strength in supply chain and digital distribution to accelerate growth and drive operational efficiencies while consolidating the centralized costs like marketing, supply chain, analytics, technology, and logistics.

All the acquired brands only sell online through 3P-platforms as well as own websites.

Since launch in 2021, it has acquired and scaled over 25 digital-first D2C brands across four major verticals -

- Home improvement & utilities - Household essentials, decor, and innovative utility products

- Home appliances - Premium kitchen and home appliances

- Home & personal care - Skincare, haircare, and wellness products

- Active, lifestyle & accessories – Apparel and accessories

“In the next 5–10 years, we’ll have 100+ brands, each solving a real problem for Indian households. That’s the dream.” — Nitin Agarwal, CEO & Co‑founder, GlobalBees

Brainbees has invested ₹1,300 Cr. in Globalbees as of Nov’24 and holds 50.73% in the entity, rest is owned by private equity. It is likely to deploy further cash (₹150-200 Cr.) to pay for earn-outs of the founders of acquired brands.

Post covid due to unprecedented surge in venture capital inflows, GlobalBees was valued at $1.1 Bn. following a fund raise of $110 Mn. As I’m writing this, the entire market cap of Brainbees is at $2.2 Bn.

Segment Financials : turned EBITDA profitable in 2024

FY 2025

Revenue - ₹1,577 Cr. ![]() +30%

+30%

EBITDA - ₹22 Cr.

Q4 FY2025

Revenue - ₹398 Cr. ![]() +33% YoY

+33% YoY

4. Preschools Franchise : Intellitots

The company shares performance of this segment under the head “Others” in their quarterly results and RHP. This segment forms a very small part of the business however high profitable margins. Company operates all of the preschools with the brand name “Intellitots” under franchise model.

Segment Financials :

Revenue FY25 - ₹42.5 Cr. ![]() +27%

+27%

EBITDA FY25 - ₹10.4 Cr. ![]() +79%

+79%

That was all regarding the Four Business Verticals of Brainbees Solutions.

Consolidated Financials

FY 2025

Revenue - ₹7,659 Cr. ![]() +18%

+18%

EBITDA - ₹393 Cr. ![]() +43%

+43%

Q4 FY2025

Revenue - ₹1,930 Cr. ![]() +16% YoY

+16% YoY

EBITDA - ₹100 Cr. ![]() +20% YoY

+20% YoY

Continuous Gross Margin expansion across all business verticals YoY.

IPO Proceeds

Industry and Market Position

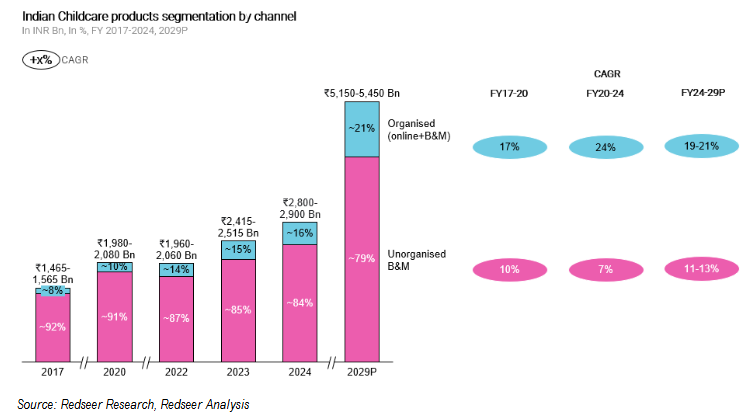

India Childcare Market

India’s childcare industry valued at ₹2.8 Lakh Cr., with ~85% of the market being unorganized.

The short usage life of children’s apparel (1-6 months), results in a lack of brand loyalty compared to other branded categories and, hence, a lack of pricing power for brands/branded retailers.

Dedicated kids’ formats have struggled to achieve scale, but FirstCry found success by focusing on infants and toddlers (0-6 years), being the first mover in the online channel/omni-channel approach.

The company accounts for almost 25% market share of the online childcare market with no competitor of significance in the 0-4 year age group, with it’s home brand BabyHug being the largest national brand serving this category. Strategically, FirstCry does not sell its home brands on other 3P marketplaces, this ensures that customers keep coming back to its multi-channel platform.

But even after its great execution the company holds about 12.5% market share in the organized sector and only 1.8% market share in the whole childcare industry.

The domestic childcare industry is projected to reach ₹5.3 Lakh Cr. by 2030 and remains a very underpenetrated market in India.

International Market of UAE and KSA

UAE will remain an only online play due to low birth rates but has much higher spend per child than both India and UAE.

But KSA market is 2.5 times of UAE, combined with much higher spend per child and birth rate than India. The company will penetrate KSA market through Multichannel retail similar to what they have done in India.

Over the next 24-30 months the company will open 12 stores in KSA, they want to have a deep understanding of the market before they really expand. The management is also being cautious of the competition from two new recent e-commerce entrants in the market. This also slowed their growth Q3 FY2025 onwards because of increased promotional activity from this competition to acquire customers.

The management expects a ‘rough ride’ of heightened competition for a few quarters but remains confident in FirstCry’s niche vertical focus and operational advantages to win long term. They have made a deliberate decision to refrain from excessive promotional spending, aiming to strike a prudent balance between profitability and sustainable growth.

D2C and preschools

I don’t think there’s any realistic way to evaluate their GlobalBees TAM realistically because they acquire brands that are performing good in their own small niche and it would not make sense to look at the total D2C market of India because they only want to scale the acquired brands in their own niche and run them efficiently over the long run. The more brands they acquire the more TAM increases for their GlobalBees segment.

Preschools franchise forms a very negligible part of the company so not looking into the TAM.

The Value Proposition

I would only like to focus on the Indian multichannel retail segment of FirstCry for now as the International markets remain very uncertain and there’s no realistic way to estimate growth of the D2C segment.

I believe the India multichannel retail segment will grow from ₹5,200 Cr. revenue in FY2025 to ₹12,000-13,500 Cr. revenue in FY2031

I did some napkin math from different perspectives to reach the estimated number.

Organized sector penetration : (source company RHP)

The total childcare industry is projected to reach ₹ 5.3 Lakh Cr. in 2030 and organized sector will obviously gain market share from the unorganized sector and grow at a higher rate.

Organized sector as of 2024 held only 15% market share valued at ₹42,000 Cr., I assume this market share will increase to 20% by 2030 reaching ₹1.05 Lakh Cr.

(Taking a bit pessimistic estimate of 20% CAGR in comparison to the whole industry CAGR of 12-14%. For reference the total childcare market grew at a CAGR of 7% from 2020-24 while the organized market share grew at a CAGR of 24%.)

FirstCry holds a market share of 12.5% in the organized sector with FY25 revenue ₹5,278 Cr. FirstCry being the market leader of the sector will definitely grow faster than the industry and gain some market share, but I’ll take a pessimistic approach and assume due to intense competition it will only be able to retain its market share till 2030.

This translates to FY 2031 revenue of ₹13,500 Cr. with a CAGR of about 20%.

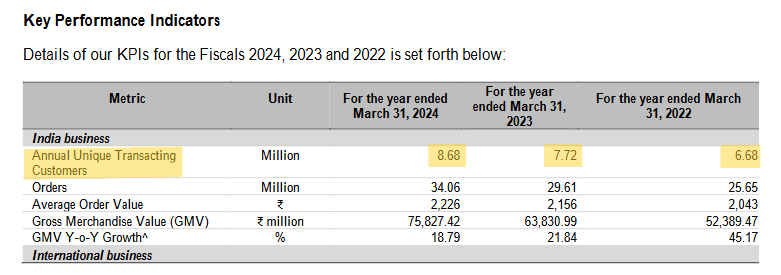

Annual Unique Trasacting Customer (AUTC) approach :

Total no. of households in India - 33 Cr.

Households with annual income >₹5.8L - 10.6 Cr.

Share of the households in this income cohort will grow at a CAGR of 4% for the next two decades and the number will reach 14.5 Cr. by 2030

FirstCry targets aspiring middle class families through mass-market approach with premium extensions, due to price point and many factors they will always be able to serve only these households with annual income more than ₹5.8L p.a.

Total population in 10 Cr. households - 42 Cr.

Assuming 15% of population in these households is <14 years - 6.4 Cr.

(India’s total population <14 years is 22-24%, so taking a much lower estimate since birth rates are lower in higher income households)

This translates to a relevant addressable AUTC of about 6.4 Cr. which reach 8.5 Cr. by 2030 and 12 Cr. by 2044

With an AUTC of 1 Cr. as on March 2025, FirstCry has penetrated to only 15.6% of the addressable customers aged <14 years even after being largest childcare retailer in the country. FirstCry’s revenue base is more than 25X its next-largest vertical competitor, underlining its near-monopolistic status in organised childcare retail.

Assuming after 5 years they would be able to penetrate 20% of the addressable customers, the AUTC will reach to 1.7 Cr. from 1 Cr.

(Again taking a pessimistic growth in AUTC with CAGR of only 11% over the next 5 years.

While over the last 4-5 years the company has been able to grow the AUTC at a CAGR of 19%)

FY25 Net revenue - ₹5,278 Cr. and AUTC - 1 Cr.

This translates to ARPU (average revenue per user) of ₹ 5,278

| Fiscal Year | Revenue India multi-channel ÷ AUTC | ARPU |

|---|---|---|

| FY 2024 | ₹4,580 Cr ÷ 8.68 Cr | ₹ 5,276 |

| FY 2023 | ₹4,280 Cr ÷ 7.72 Cr | ₹ 5,545 |

| FY 2022 | ₹1,973 Cr ÷ 6.68 Cr | ₹ 2,954 |

The noticeable significant blip in FY 2023 ARPU & revenue and the plateaued revenue & ARPU in FY 2024 was due to consolidation of Digital Age stores and other temporary factors which i won’t get into rn.

Assuming the ARPU will continue to rise by 5 odd-percent CAGR over the long period factoring inflation, which is again a pessimistic approach because I’m not accounting for increased discretionary spending by the parents which would also increase the ARPU.

So, only factoring inflation ARPU will be ₹7,000 in 2030

This gives us FY 2031 Revenue of :

= Annual Unique Transacting Customers x ARPU

= 1.7 Cr. x ₹7,000

= ₹12,000 Cr. with a CAGR of 18%

Low Valuation

Current Market Cap of the whole company - ₹19,000 Cr.

As per my estimation, FirstCry alone would have a revenue of 12,000-13,500 Cr. by FY2031

Net Profit FY 2031e ⇒ ₹1,200-1,350 Cr. (assuming 10% NPM)

EPS FY 2031e ⇒ ₹23

This translates to a forward P/E of 16 @ CMP of ₹370

Again, this is just from the India Multichannel Retail of FirstCry.

My Thoughts

What we get for “free” at the current price

- Market is fairly pricing only the India multi-channel retail.

- Even if we strip out the loss-making International segment & GlobalBees, the core India multi-channel retail is trading at 3.5x its own sales.

- International e-com (UAE+KSA), GlobalBees roll-up, and a profitable preschool franchise, even tho new businesses but high growing and together generate ₹2,300 Cr. revenue but contribute < 0.5x P/S to the valuation.

- Any upside in these segments is effectively a free call option.

What happens if the management merely hits my “pessimistic” numbers?

- India multi-channel revenue FY31e ⇒ ₹12,000-13,500 Cr.

- Add a very modest ₹4,000 Cr. from GlobalBees + preschools + International (only 10% CAGR from FY25) ⇒ ₹16,000–17,500 Cr. Consol.

- Assume 8-10% net margin (Consol. gross margin already 36%; expected to rise by 400 bps)

Net profit FY31e ⇒ ₹1300-₹1,600 Cr.

Forward P/E ⇒ 12-14x – cheaper than every listed specialty retailer and e-com players of comparable growth.

Why a 10% net margin is realistic?

- Home brands share already 55% of GMV, every 100 bps mix shift lifts gross margin by 60 bps.

- FOFO commission renegotiation and scale in General Trade can add another 150 bps to EBITDA.

- COCO store expansion will give better control over inventory management as well as increase gross margin from offline GMV but can also lead to cannibalization of FOFO store sales.

- Fulfilment and tech opex are largely fixed; AUTC grew 17% in FY-25 while opex rose only 9%.

Disc - Not an investment advice, invested at current level.