Ratings upgrade.

ICRA Ratings report now attached

ICRA ratings upgrade report.pdf (281.5 KB)

Ratings upgrade.

ICRA Ratings report now attached

ICRA ratings upgrade report.pdf (281.5 KB)

Hi

Got a message from a friend about this tweet. Any views (posting this in the Borosil thread but it is applicable to Borosil renewables too).

Rgds

Disc: My views are biased since invested

While the list highlighted by the tweet shows Borosil group in bad company, it could be an issue of selective sampling… as we don’t know the entire list of companies audited by this auditor. Also auditor is just one item on the check list which apparently looks bad for Borosil (hope they change it sooner).

But I have been investor in this group (Borosil Ltd and Boro Renew) for last 3+ years and invested big portion of my PF. If you look at their past actions , whether it is 23% buyback in 2016(unheard of in Indian industry), liquidating real estate assets and equity mutual funds and investing that money in acquiring value accretive growth businesses (Klasspack, Hopewell tableware etc) or investing in debt mutual funds, launching and completing amalgamation scheme which removed related party transactions and simplified the corporate structure, I feel comfortable with their capital allocations, transparency and their minority investor friendliness. So not too concerned with the quality of auditor as of now but I hope they change it as it may affect their image and credibility in the market

Q3 FY 21 results. YOY 9% increase in Sales and 20% increase in PAT . QoQ much bigger growth. Overall good results. Highest ever quarterly profit. Scientificware (vaccine vials?) helping the profitability whereas company may had to give more discounts in consumerware as can be seen from segmental breakup.

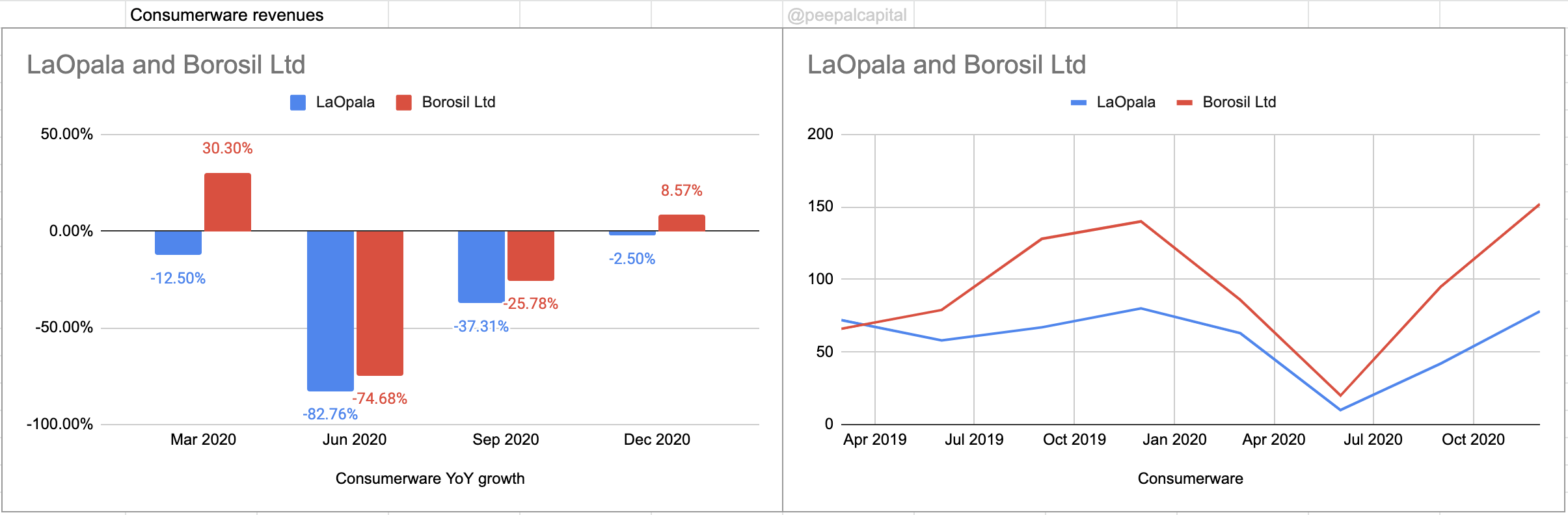

If La Opala guys decide, they can make life difficult for Borosil…but they are not. They are too complacent and are happy with their margins and their market share (which is going down slowly). This means they are allowing Borosil to get in and establish themselves… As a shareholder of Borosil, I have no complaints…

Hi Deevee - I am not sure comparing the Consumerware division vs LaOpala is the appropriate comparison? Perhaps comparing Larah with LaOpala is more appropriate (although LaOpala also sells some glassware)? Borosil used to separate out the Larah sales previously and did not for Q2 results (don’t think they have released the Q3 presentation where they seemed to indicate they would go back to better disclosure). In FY21 Q1, Larah was down 87%?

Without a doubt Larah was gaining market share previously but would be great to see the split. Having said that, I suspect they appliances part of Consumerware has done really well this time and hope they start splitting this out as well.

Disc: Invested in Borosil Ltd so am biased

Hi @akacker

Yes it is not right to the dot but the next best comparison available. Your hypothesis is perhaps right on the appliances business line. Lets wait for concall transcript.

rgds

By any chance if you attended the concall please could you share your notes. Thank you.

Rgds

Deepak

Hi

Was looking at the deck

Opalware increased by 8.9 percent YoY for Borosil vs a de growth of -2.3% for LaOpala revenues.

cc: @akacker

Rgds

Cello is a strong contender and has been taking away market share from the leader.

What % of Borosil’s revenue comes from electronic appliances and has the management given any guidance on it?

I recently ordered a Borosil Oven and it’s been working really well. Quality is top grade. My mother broke the front glass door by dropping something on it so we had to call the service number. Service was extremely good, they were on time, followed up, charged a very nominal amount and everything was super professional and hassle free.

Then recently, I ordered 2 air tight glass jars from Amazon. They were made by Borosil as well. Again, top notch quality and great stuff. Very modern and functional design that you don’t see from some of the other players. Even Amazon reviews on almost all of its products are great and have top ratings.

Has anyone looked at their revenue growth rate in other segments like consumer electronics, Amazon sales etc?

| Sales | Q3FY21 | Percentage | Growth YoY |

|---|---|---|---|

| Glassware | 34.33 | 17% | -21.20% |

| Non Glassware | 61.63 | 30% | 36.70% |

| Opalware | 56.01 | 27% | 8.90% |

| Laboratory Glassware | 33.86 | 16% | -1.50% |

| Lab Instrumentation | 4.41 | 2% | 8.90% |

| Pharma Packaging | 14.98 | 7% | 22.80% |

| 205.22 | 100% | ||

| Total Consumerware | 151.97 | 74% | 8.50% |

| Total Scientific | 53.25 | 26% | 5.20% |

| 205.22 | 100% |

Hi @deevee,

Yes, I did attend the concall but unfortunately did not take any notes. The most important highlight of the call was they will be supplying vials to Covaxin (and not to Serum covishield) and hence yet to start any meaningful supply of vaccines. Management felt it may start from Q1 FY 22. But they are getting lot of business from other pharma companies who are not getting their supplies from their regular suppliers, as these suppliers are busy supplying vaccine vials. Also management felt that there is no demand supply gap for vaccine vials as of now. So they see no need for further capex unless they get clarity about life of the vaccine ie. effect of the vaccine. If it is going to be onetime shot, then adding more vial capacity right now could create long term over capacity problem. So they are cautious and would like to be bit conservative right now till they understand if the demand would persist or not.

Deciding to invest in a company based on its auditor is one of the most illogical conclusion I have come across.

Name me an auditor and I will show you the scams they were involved in. From KPMG, PwC, Deloitte to even any local company, or even credit agencies. Everyone has been involved or been a victim of scams.

Read about the Wirecard which was a German Bluechip and KPMG was it’s auditor.

Can’t they repurpose their vial making factory later for making other glassware needs, e.g. scientific glassware or consumer glassware? I just worry that they may loose out on making a big sum if they can’t supply enough vials than what is needed. If they don’t take this opportunity, someone else will do it and they will also loose out on the reputation associated with it. Regardless, enough reports claim that Covid vaccines won’t be an onetime shot.

Shreevar Kheruka mentioned that vial making machines are custom designed machines and hence can not be used for other items like syringes etc. Being in that business, he would be knowing what is happening in that area. What we see/read/hear from outside could be bit of “noise”. Borosil group is conservative (similar question was asked on Boro Renew concall about why don’t they increase solar glass capacity by 4 times, rather than only 2 times and answer was they would like to take one step at a time)

PM took Covaxin shot today. This is significant for Bharat Biotech and in turn Borosil Klasspack.

Hi @JJu,

Wasn’t able to find any direct link between Covaxin and the vials made by Borosil. Could you please share the source for this?