This is my first attempt at starting a thread. I am grateful to this forum for providing so much knowledge with a lot of openness. I am an IT guy with limited understanding of the investment world. I have no expertise whatsoever in textile industry. But I have understood the importance of headwinds and tailwinds – fo shure. In my opinion, Indian textile industry is at the crossroads today with lot of tailwinds. For starters we now have no obligation to deter own businesses to keep our silly neighbors happy. Here is the recent bite from Piyush Goyal (Minister of Commerce and Industry of India): https://www.youtube.com/shorts/TDkdt1-8bXs

Indian govt recent anti-dumping probe on the imported polyester textured yarn and imported polyester partially yarn signals further policy support for the domestic manufacturers. This coupled with recent FTA with European Union are beneficial to textile industry. Additionally, govt has permitted 100% FDI in textile industry.

Before we move further, I highly recommend watching this video from SOIC to understand the value chain of textile industry: https://www.youtube.com/watch?v=egZR1Ga4ltU

Borana Weaves Limited is a textile manufacturing company engaged in the production and sale of woven fabrics. The company’s products are primarily used by garment manufacturers, exporters, and other textile processors. Borana Group is one of the largest producers of greige polyester woven fabrics in India, producing 22 crore metres of high-quality synthetic and blended greige polyester fabrics annually. Borana Weaves started as a small textile trader back in 1975. Overtime, the business evolved and the company came with its IPO in May, 2025 with a price of 216. The purpose of IPO was to finance the cost of establishing a new manufacturing Unit to expand its production capabilities, funding incremental working capital requirements and general corporate use.

Here is a brief detail on the Promoters and executive leadership:

Mangilal Ambalal Borana – Chairman & Managing Director

Founder and promoter of the company with multiple decades of experience in the textile industry; drives overall strategy and vision.

Ankur Mangilal Borana – Chief Executive Officer (CEO)

Heads operational functions including production, sales, procurement, and HR. He holds a Bachelor’s degree in Commerce from Veer Narmad South Gujarat University with 13 years of industry experience

Rajkumar Mangilal Borana – Chief Financial Officer (CFO)

Leads financial strategy, commercial planning, and corporate finance functions; has significant industry experience across textiles and related sectors. he has same qualification as Ankur.

Now lets deep dive into the business. Business has two segments Greige Fabric and PTY Yarn. Griege Fabrics contributes about 90% of revenue while remaining is done by PTY Yarn. Greige Fabric is utilized in below applications:

-

Apparel and Garments: Processed into soft, everyday garments for men and women.

-

Home Textiles: Processed into soft, durable bedding products that offer a premium feel.

-

Technical Textiles: Processed into durable, weather-resistant materials for tent applications, hospital linens and waterproof fabrics.

Borana has four advanced manufacturing units based out of Surat, the Manchester of East. This location gives strategic advantage from procuring raw materials to selling finished products. Proximity to major ports may also help with future exports (currently only clients export). Current capacity, as of Dec 2025, stands at 39.21 crore meters. The company claims to operate at scale that is currently unmatched among the companies with a similar product focus. Company plans to meet 70% of its electricity demands through renewable sources (18 crores worth power saving) and taking steady steps to achieve this target. Company plans to double its capacity in next two years (1000 to 2000 water jet looms). Unit 4 is currently in expansion phase with 160 water jet looms installed and working. Total cost of additional 1000 water jet looms will come around 350-400 crores: 200 cr capex, 70 cr WC, remaining renewable cost.

Borana currently benefits from two state subsidies: interest and power. As per management, 30% to 40% of the interest cost subsidy and 2 rs per unit of power subsidy. The power subsidy is given for 5 years with current status for each unit are: unit 1 till 2026; unit 2 till 2027; Unit 3 till 2028. Margins will remain intact once these subsidies are over as the balance will come from renewable. Below are the clients of Borana Weaves:

- GANGA TEX TRENDZ (P) LTD

- OSWAL INTERNATIONAL

- NIRANKARI TEXTILES

- SUDARSHAN SILK MILLS

- AMBAJI FABRICS

- VARUN TEXTILE

- SHRI HARI TEX

Below are the key growth drivers for this industry:

- Rise in demand for athleisure, performance & technical textiles.

- Sustainability: increased demand for rPET / recycled polyester yarns and biodegradable variants.

- Government incentives: e.g. Production Linked Incentive (PLI), quality / standardization schemes.

- Innovation in new yarn types: low shrinkage, high modulus, etc.

- Geopolitical Uncertainties and trade barriers in key markets.

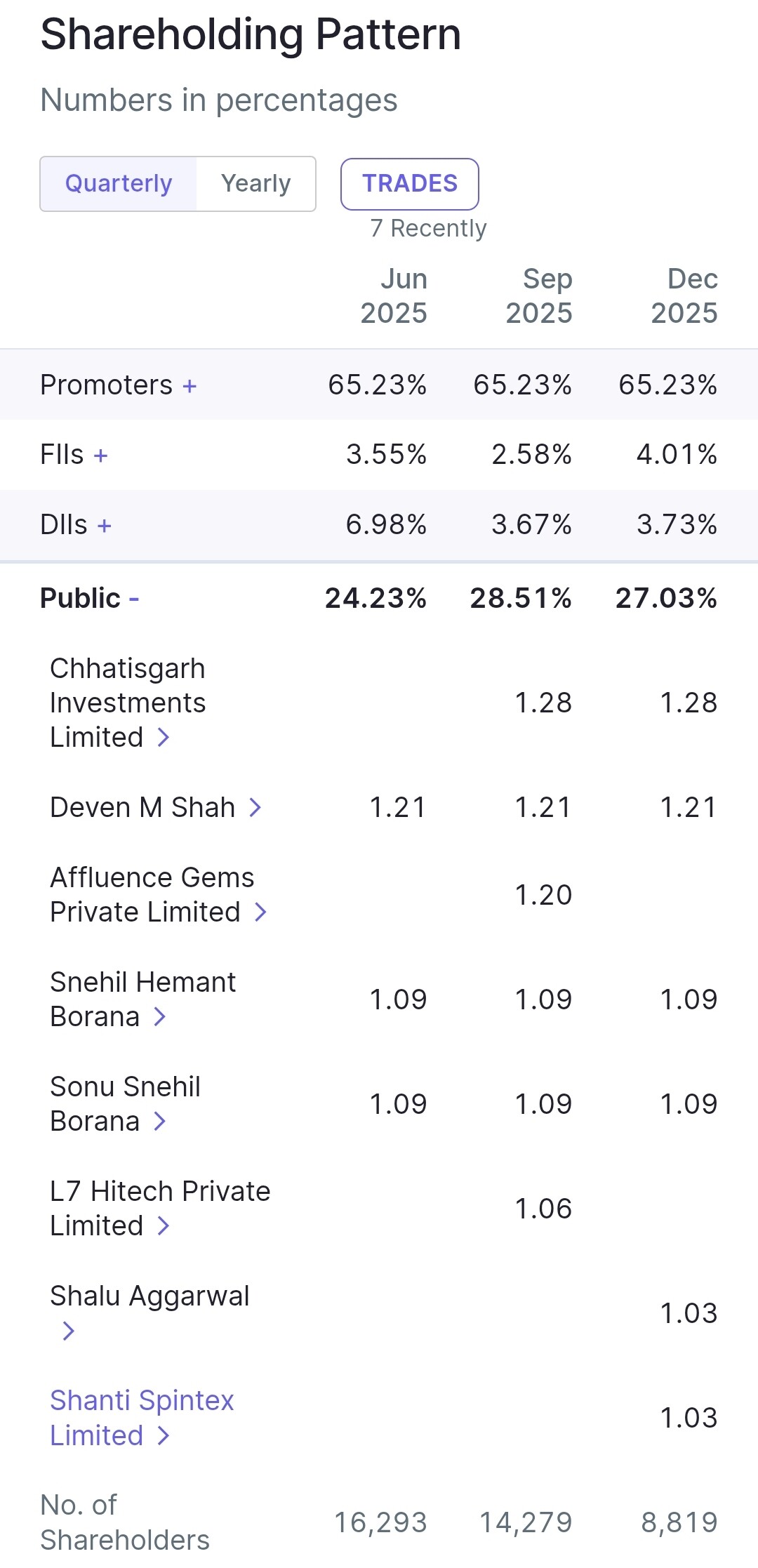

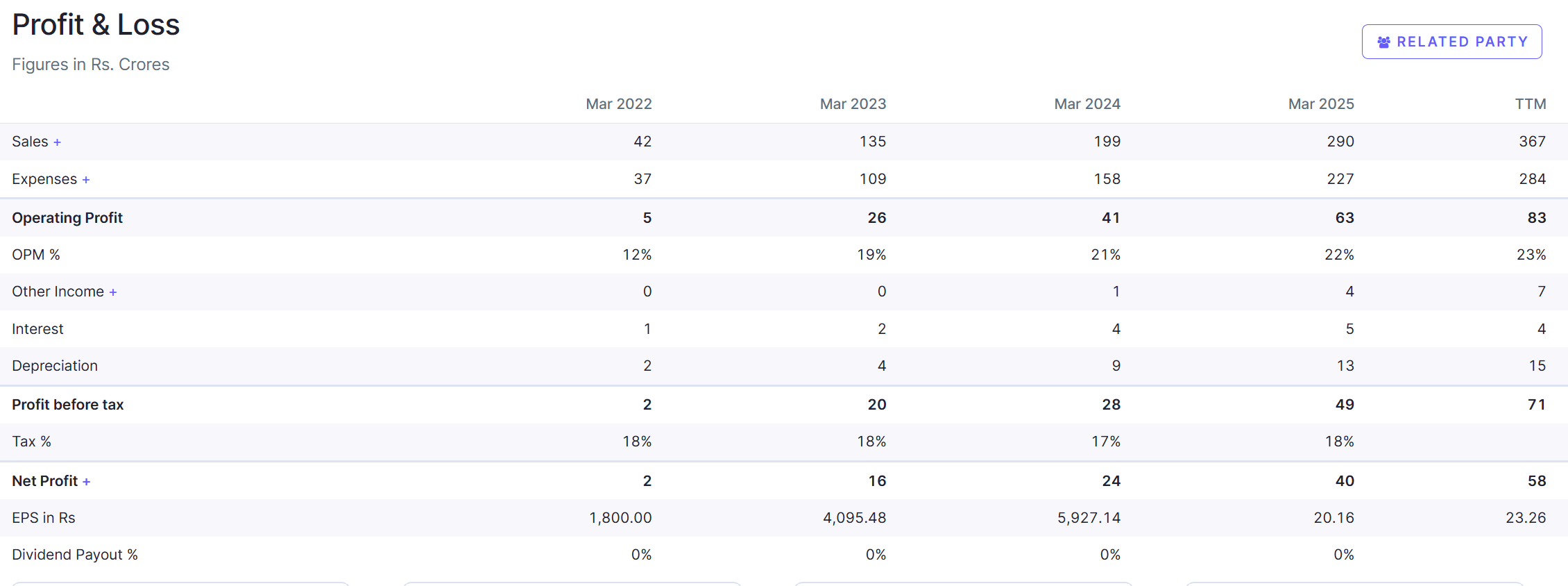

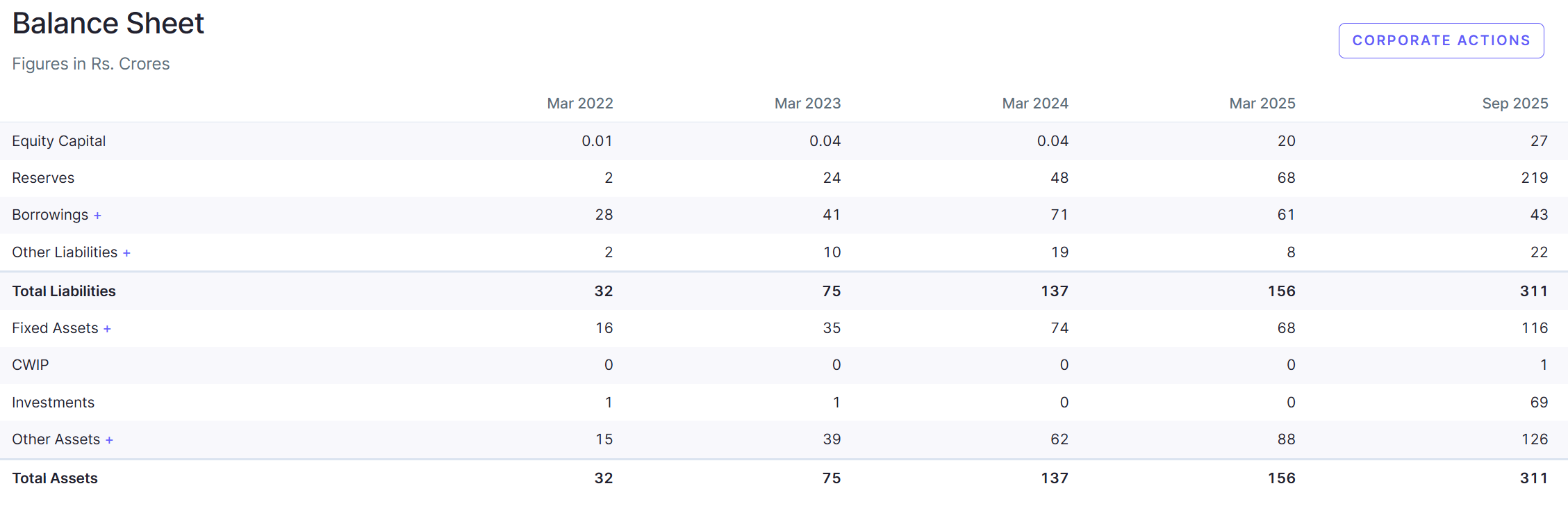

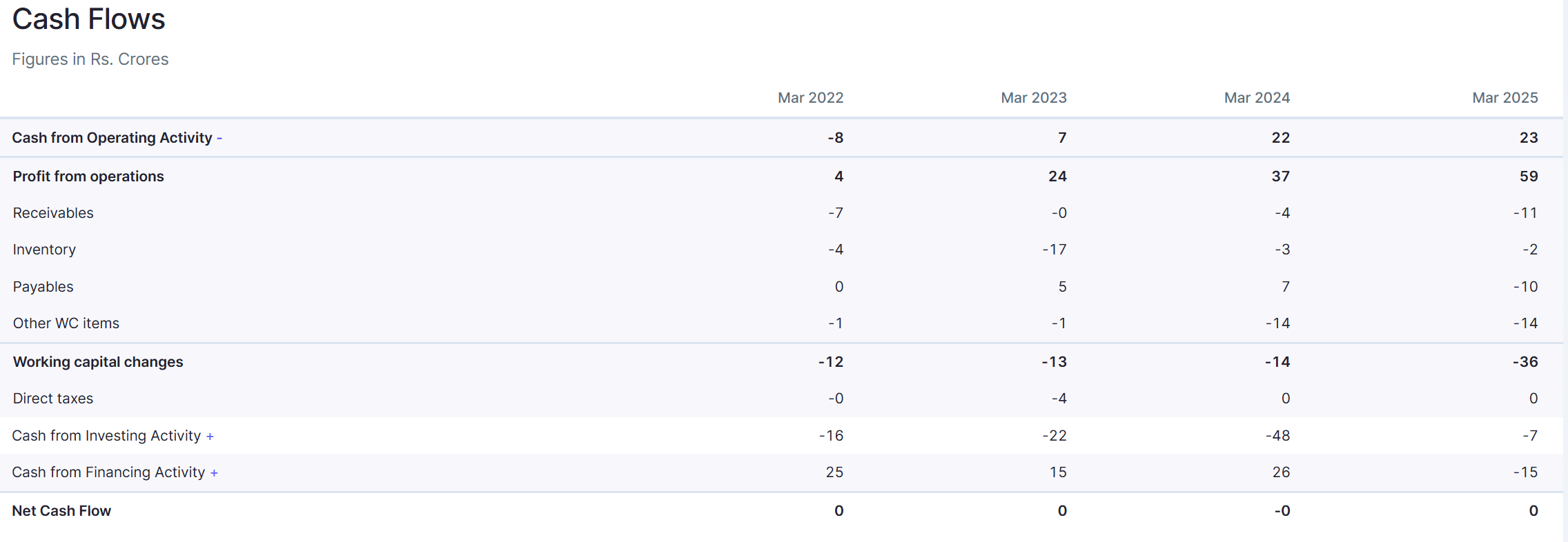

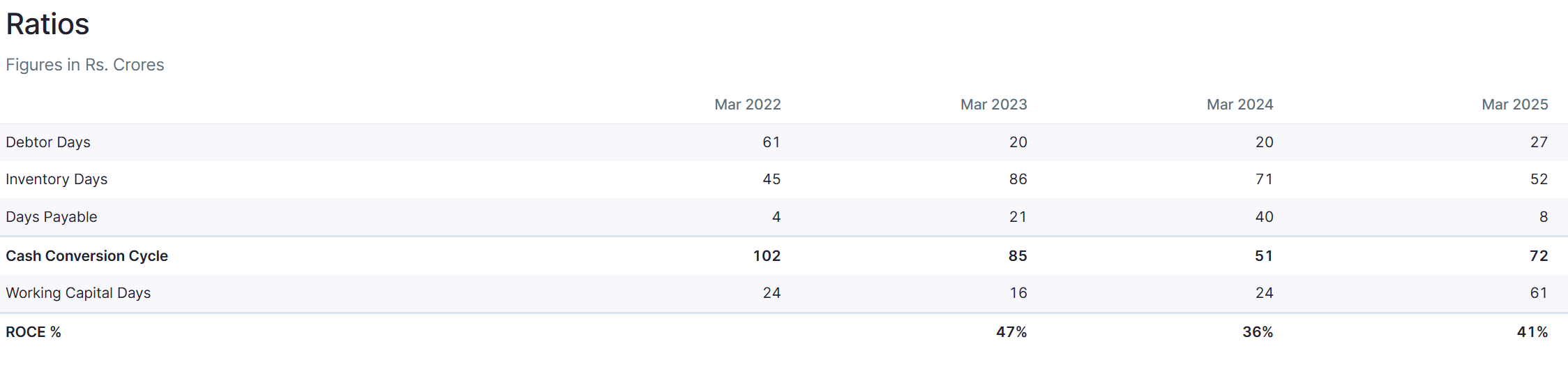

Financials: I am presenting the screener screenshots for P&L, Balance sheet and Cash flow statement.

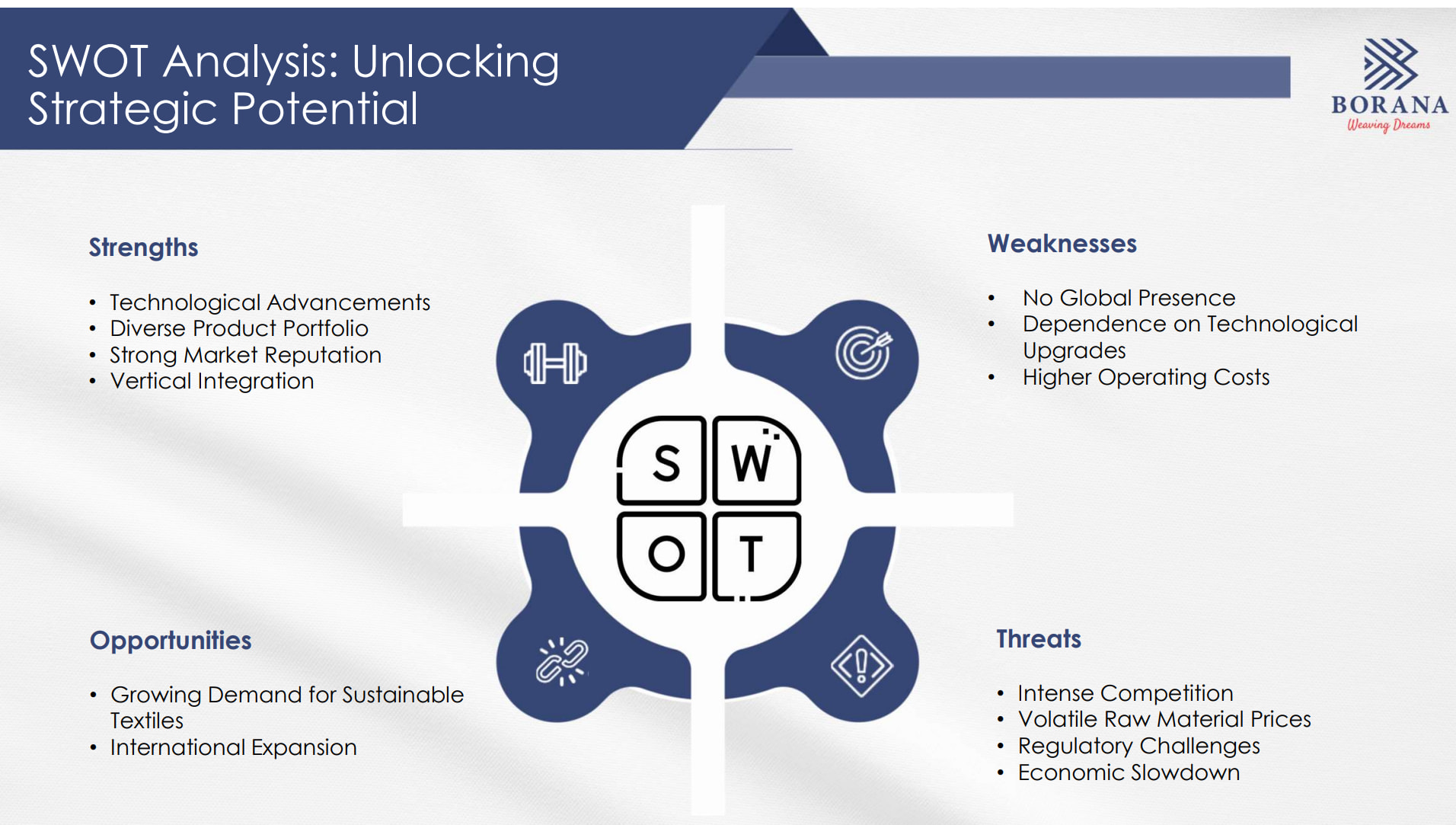

Borana enjoys EBITDA margins of >20% which is quite good in this industry. I am yet to do the valuations. Will share once I do those calculations along with a bull, base and bear case scenario. Below is the SWOT analysis from recent ppt.

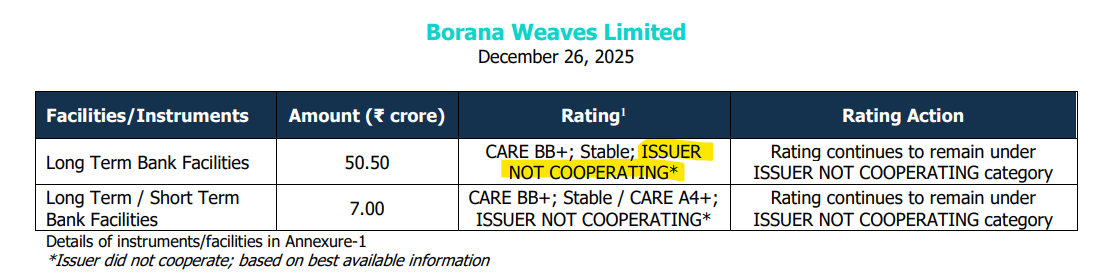

I was going through the latest credit rating by care edge released in Dec 2025. I found a big red flag of non-corporation by the firm.

I tried to find mention of the same in latest concall but none of the analysts asked this question. I am not sure what to make of this other than CG issue. I request forum members to help understand this part. I have attached all the sources at the bottom.

I continue to research on the company and will add more information soon.

Disc: tracking without position

Concall Jan 2026.pdf (1.1 MB)

Ratings Dec 2025.pdf (146.9 KB)

AR FY25.pdf (4.0 MB)

ppt Jan 2026.pdf (5.5 MB)