Introduction: BMW Industries Ltd (BMWIL) is one of the leading Steel Service Centres (SSC) for large primary steel companies like Tata Steel Ltd (TSL), JSW Steel , SAIL etc.

Major names in the SSC space are Mahindra Accelco, Tata Downstream Products Ltd, JSW MI Steel Service Centre etc.

BMWIL is mostly dedicated to TSL’s product services in the steel downstream sector in various processes for which it derives service revenue and the named players are not competitors of it. As the primary steel players’ focus gradually shifts from selling semis to higher value-added products, the need for the SSCs in the Steel ecosystem is set to rise like in Western countries, because a primary steel player can’t convert all hot metals into value-added products directly, which would ask for humongous inventory space and logistic issues to address different territories. However, a primary steel player can convert a fraction of hot metal, and indirectly transform the majority of semis (hot-metal production in the form of HR Coil/Billets) to value-added products and markets across territories and customers having varied purchasing powers through SSC like BMWIL.

BMWIL-TSL unique SSC arrangement: BMWIL undertakes various steel engineering services through its 7 dedicated manufacturing setups in Jamshedpur (5nos) and Howrah (2nos). The service contracts are renewed periodically (3-5years) considering the factor of production cost trends aligning with inflation. No raw material is part of its Cost of Goods Sold, and all logistics costs are borne by TSL, thereby yielding a decent margin irrespective of volatility in the metal sector. Furthermore, BMWIL has 100+ fleets of heavy-duty trailers which are deployed in the logistics operations of BMWIL-TSL agreements which cost is also borne by TSL. In contrast, in Western countries, SSCs like Ryerson Holding (RYI: NYSE), Olympic Steel (ZEUS: Nasdaq), Reliance Steel (RS: NYSE) etc. buy raw materials like HRC, Billets, etc and process them to sell independently to end industrial customers. BMWIL has three decades of SSC relationship with TSL, which itself is a great strength. The service rates for different operations are negotiated in such a fashion to yield decent margins and cash flows at the hands of BMWIL.

Manufacturing Services delivered: BMWIL undertakes several services to TSL like Slitting & Cut to Length of HRC, Hot Roll Coil (HRC) Pickling & Oiling, Annealing and Galvanizing of Cold Roll Coils, Galvanised Plain & Corrugated (GP/GC) Sheet manufacturing (sole manufacture of Tata Shaktee GC sheet for TSL), Structural Pipes (Tata Structura), Water and Oil & Gas ERW Pipes, Galvanised Water Pipes, Tata Tiscon Rebars. All the facilities are TSL audited for complying to quality/safety standards. BMWIL does not carry any marketing rights or risks, but only derives service income from TSL which have been stable over the years. Prior to FY21, BMWIL had ventured into its own manufacturing into steel profile manufacturing etc, but post FY21 it has strategized to focus on servicing TSL to ride on growth opportunities TSL is going to offer till FY2030. Currently, BMWIL is deriving major revenue from TSL.

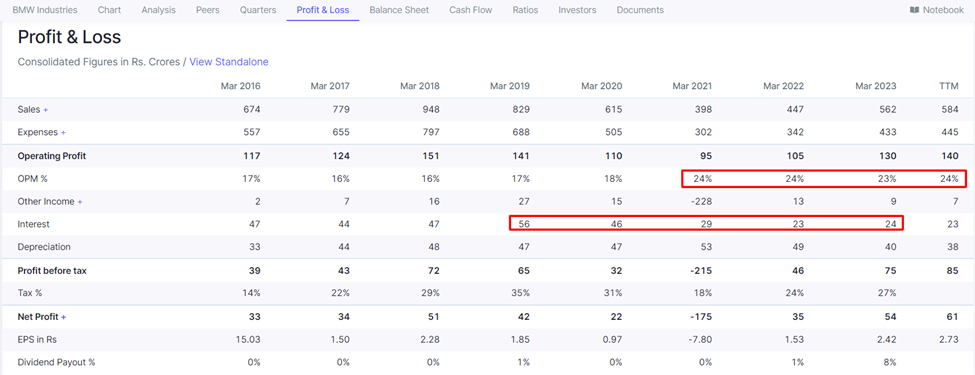

BMWIL bracing for the next level of growth The Company has reduced its debts from a peak level of Rs569cr (FY16) to Rs238cr in FY23. While most parts of the loans of the past capex are repaid, BMWIL is now bracing for the next round of growth, mostly from the Pipe and Tubes segment. BMWIL enjoys A- debt rating from the top rating agency Fitch (India Ratings). Renowned Lodha & Co are the statutory auditors. Detailed report - India Ratings and Research: Most Respected Credit Rating and Research Agency India.

BMWIL generates strong cash flow, EBIDTA to CFO 93% historically: BMW has derived strong cash flows which has helped it grow organically and help deleverage its balance sheet. The current leg of expansion in Pipes and Tubes of Rs170cr over FY24-25 can be easily funded through internal accruals by estimating EBIDTA of ~Rs.130-150cr for current year. The new capacity is expected to be margin accretive and the bottom line is expected to record strong growth.

BMWIL’s activity level set to grow ~3-4x from current level on the back of TSL’s massive expansion plans: In recent years TSL has gone on a massive expansion spree to double steel capacity in India by 2030. One of the expansions of 5 MTPA at Kalinganagar (flat 3mnTPA at present) will come on stream by Mar 24, which will be further raised to ~12mnTPA by FY30. Furthermore, TSL also is undertaking plans to do phase expansion Neelachal Ispat (long 1mnTPA) which it acquired in 2022 to 4.5mnTPA by FY26 and thereupon to 10mnTPA by FY30. It’s expected that BMWIL’s service volume is expected to double in 2-3 years and even 2x from there by 2030.

Experienced Promoter: The founding promoter Mr. Ram Gopal Bansal has nearly 50yrs of experience in steel trading, manufacturing etc. He has successfully led Joint Venture with SAIL and collaborated with Tata Steel for the development of the Steel Service Center Industry. Under his vision and leadership strategy, the Company is now one of the leading manufacturers/Service providers in the Iron & Steel sector. He is now ably supported by two well-educated sons, Mr. Harsh Bansal and Mr. Vivek Bansal acting as Joint MDs looking after Strategy/Finance & Operations respectively.

Creeping acquisition by promoters Promoters have been on a creeping acquisition spree in recent years: Promoter group has been buying for the last 3 years (~4% stake) to raise stake at 74% (threshold 75%). No part of the shareholding is pledged.

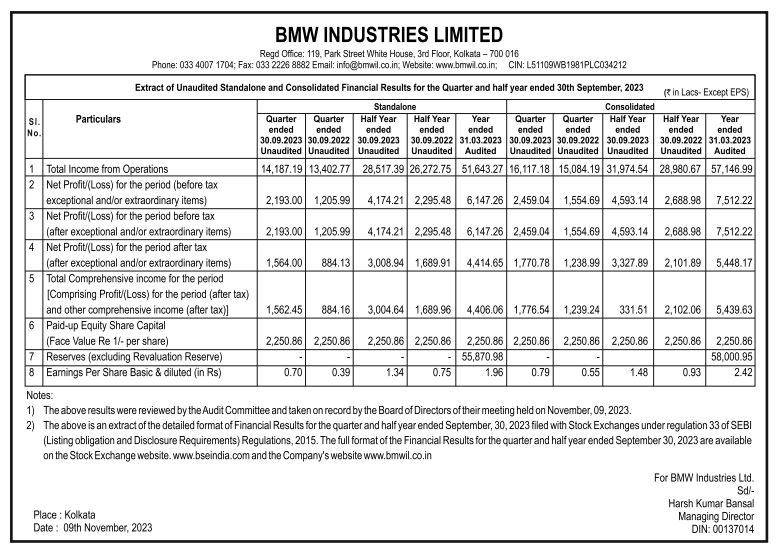

Financials:

Stable EBITDA margins in last 3 years after reducing focus on own brand and working as SSC of TSL. One off loss in FY21 due to under insurance of assets/receivables affected due to Amphan cyclone. Like many old Indian corporates, the company had been insuring assets based on historic value rather than on market value and suffered in FY21.

Debt repayment of more than 400 cr over the years

Risks:

- In case of low GDP growth and low growth of steel sector, TSL plans might be impacted which will impact BMWIL directly.

- Growth in existing rate of services or future rates tied up for services need to be beating inflation.

Disc: Invested. This is not a stock recommendation to buy or sell. Please do your due diligence. I am not SEBI registered analyst.