Therefore I took a look into Edelweiss research report on management meet. Everything looks positive

but CFO not increasing and debt not going down is confusing me :

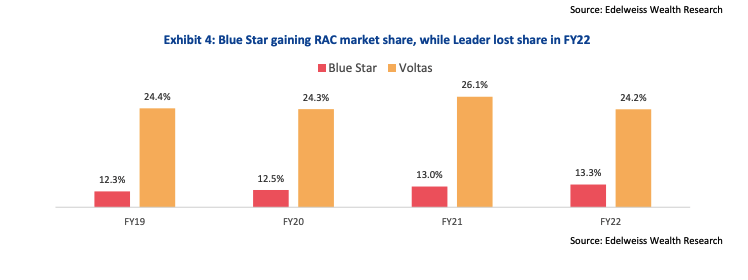

They have been gaining market share since few years.

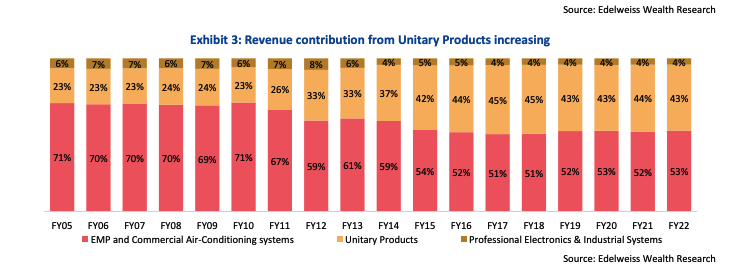

Revenue contribution from Unitary Products is increasing since many years and now stands at 43. I am guessing that unitary products has better cash conversion cycle and hence there cash flow should be increasing since last many years but it is not visible.

They have become conscious before bidding for the government project(known for reducing CFO and increasing cash conversion cycle) but still there CFO is not increasing and their debt is still increasing.

I think AC as a category is an outlier among other consumer durables and home appliances segment in terms of growth and with now industry coming out of 2-3 years of low growth led by delayed summer/high competitve intensity, AC as a category should be an outlier among other segments

India’s AC market is HOT! Blazing summers & rising incomes = AC gold rush. Overtaking China by 2045? Ambitious, but not impossible. This could be a game-changer for the industry.

Supply chain woes continue to plague the AC industry. Copper & compressors are the main culprits. Domestic production is slowly improving but still heavily reliant on imports. Expect prices to stay high for a while.

New chillers for data centers & brine chillers mean they’re aiming for bigger fish in the market. Smart move to diversify & tap into growing sectors.

Blue Star Limited Q2 and H1 FY25 Earnings Conference Call Summary for Investors

This summary focuses on key takeaways from Blue Star Limited’s Q2 and H1 FY25 earnings conference call, particularly for investors considering a long-term investment in the company.

Overall Performance and Outlook

Blue Star delivered a strong Q2 with revenue growth exceeding 20%, operating profit growth around 22%, and net profit increasing by over 36%. [1] This robust performance is attributed to strong demand across key segments and a substantial order book. [2]

The company remains optimistic about FY25, projecting it to be another landmark year. [3, 4] They expect to achieve top-line growth between 25% and 30% in the unitary products segment, particularly in room air conditioners. [5]

Blue Star maintains its margin guidance, aiming for around 7.5% in Segment 1 and 8.5% in Segment 2. [6]

The management acknowledges uncertainties in the global economic environment but is hopeful that the slowdown in other industries won’t negatively impact the air conditioning sector. [7]

Segment Performance

Segment 1 (Electromechanical Projects and Commercial Air Conditioning) witnessed 32.6% revenue growth, driven by strong performance in commercial air conditioning products and services. [8, 9] Manufacturing and data centers are also contributing significantly to this segment’s growth. [9, 10]

Segment 2 (Unitary Products) experienced a 5.1% revenue growth, primarily driven by the room air conditioner (RAC) business. [11] The commercial refrigeration business faced challenges due to regulatory changes but is expected to recover in subsequent quarters. [5, 12]

Segment 3 (Professional Electronics and Industrial Systems) recorded a modest 3.8% revenue growth. [13] The management anticipates growth to revive in Q4 FY25. [14]

Key Drivers and Challenges

The RAC business is performing exceptionally well, benefiting from increasing demand, stable prices, and growing consumer finance options. [15, 16] Blue Star is focused on expanding its distribution network, investing in R&D and innovation, and optimizing its supply chain. [2]

The commercial refrigeration business was negatively impacted by regulatory changes related to water coolers and the delayed ramp-up of new deep freezers. [12] However, the company expects these challenges to be resolved soon, with normalization expected from Q3 FY25 onwards. [17]

Blue Star is actively investing in new product development, particularly in energy-efficient and decarbonization solutions for international markets like Europe and North America. [18, 19] However, the company is cautious about the slowdown in Europe and uncertainties surrounding the US market. [19]

Financial Position

Blue Star has a strong financial position with a net cash position of rupees 18,526 crores as of September 30, 2024. [8]

Working capital requirements have increased due to investments in components to ensure a robust supply chain for the upcoming summer season. [20, 21]

The company is continuing its investments in R&D, manufacturing capacity expansion, and digitalization. [8, 22]

Investor Considerations

Blue Star’s strong performance, positive outlook, and focus on growth segments like RAC and commercial air conditioning make it an attractive investment opportunity.

The company’s commitment to R&D and new product development positions it well for future growth.

Investors should be mindful of the potential impact of external factors like global economic slowdown and regulatory changes.

Further clarity on segment reporting, particularly separating commercial air conditioning from other segments, would enhance transparency and aid investor analysis.

This summary provides an overview of Blue Star Limited’s performance and future prospects. Investors should conduct their own due diligence and consider all relevant factors before making any investment decisions.

There was a filing to BSE with regards to dispute between the Company and WJT. The filing is about alleged claims brought by WJT.

WJT has put a case in the Dubai court against Blue Start and asking for a claim. But now, it has increased the claim amount from 223 Cr Rs to 460 Cr Rs from the company.

Looks like Company had a joint venture in Oman with WJT as Blue Star Oman Electro Mechanical Company in 2015. The details are mentioned in the below link:

Not able to know the full details of the reason. Can someone throw more light into this?

Market share of Indian companies are shrinking rapidly and these giants are entering Indian market with their inhouse tech, yet these Indian companies are not interested in manufacturing compressors and keep doing design and nifty changes in the name of R&D.

The last post on this company was in May 2025. Is it time to take another look at it? Also, the thread on cooling may be showing a way to us.Cooling May Be India’s Next Big Infrastructure Theme ⚡

I am writing this before its Q1, '27 quarterly results. As per the last results, the company was catering to three segments.

As per the company, it caters to three segments.

Let me confess that my attention to the company has been drawn by videoes which mention Blue Star as one of the major cooling companies into Data Centres. So, much of what I find and see is likely to be affected by confirmation bias. My particular reason for looking into it is because its main competitor, KRN Heat Exchanger is going at a PE of 118, which makes Blue Star, though expensive at 68, cheaper in comparison. KRN Heat Exchanger manufactures customised heat exchangers and related products for the Heating, Ventilation, Air Conditioning, and Refrigeration sector. KRN has a B2B business model, supplying mainly to original equipment manufacturers (OEMs) like Schneider Electric and Blue Star.

Report dated February 02, 2026 by Mirae Asset-Sharekhan in the wake of the last quarter results has highlighted that the EMP Segment recorded a growth of 9% to Rs 1,696 crore but orderinflows has declined by 16.5% y-o-y. It also noted that, “Growth was aided by execution of projects from several sectors such as data centers and manufacturing. Order inquiries were strong, led by continued demand from factories, data centers, and healthcare sectors but order finalizations were muted. The commercial air conditioning business saw healthy order bookings on strong demand.”

Aluminium prices may affact the current quarter’s performance.

Here are some relevant factors about its role in Data Centres:

Revenue Contribution: The company expects data centers to contribute approximately 10% of total revenue in the coming years (roughly ₹1,500 crore when total revenue hit ₹15,000 crore).

Order Book: As of early 2026, Blue Star holds an order book of approximately ₹1,500 crore specifically for data center MEP projects.

Technological Shift: The company is expanding beyond traditional AC units into high-margin precision chillers and liquid-cooling solutions tailored for the AI-driven data center boom.

Many analysts had downgraded the stock as it had reached the PE of as high as 91 in Jan '25. In February this year it touched 76.8. Blue Star currently holds significant market shares in key equipment required for data centers:

Ducted Systems: ~50% market share.

Scroll Chillers: ~45% market share.

VRF & Screw Chillers: ~20% (holding the No. 2 position).

As per Mirae Sharekhan report of Feb this year, “Blue Star is well-placed to leverage on the opportunities in the domestic RAC and the

commercial cooling and refrigeration industry. The company also plans to exploreexports opportunities in countries like the US and Europe. We expect revenue/adjusted PAT to post a CAGR of ~13%/~14% over FY2025-FY2028E. At CMP, the stocktrades at ~48x/40x its FY2027/FY2028 EPS, respectively. We maintain a Buy rating and value the company on segment-wise SOTP basis on FY2026E EPS for a PT of Rs.2,100.”

The Motilal Oswal report of 17th April 2026, says, “From a medium-to-long-term perspective, the company is entering into a favorable phase marked by improving competitive positioning, benefits from backward integration, and a robust, diversified order book across infrastructure, commercial real estate, and data centers. It has strategically focused on high-margin verticals like factories, data centers, hospitals, and organized retail, driving faster execution and better client quality. Management’s consistent focus on execution discipline and capital allocation further reinforces earnings visibility and return ratios. We raise our EBITDA estimates by ~5% each for FY27 and FY28. We forecast a CAGR of ~17%/24%/32% in revenue/EBITDA/PAT over FY26-28, fueled by healthy growth across UCP and MEP & CAC businesses. We estimate OPM to expand ~50bp/30bp in FY27E/FY28E, led by positive operating leverage and cost-saving initiatives. At CMP, BLSTR trades fairly at a P/E of 54x/43x on FY27/FY28E. Our SoTP-based TP stands at INR1,950 (valuing UCP/EMPS at 45x each and PES at 25x FY28E EPS). Reiterate Neutral.”

Disclaimer: I have made a small investment in it.