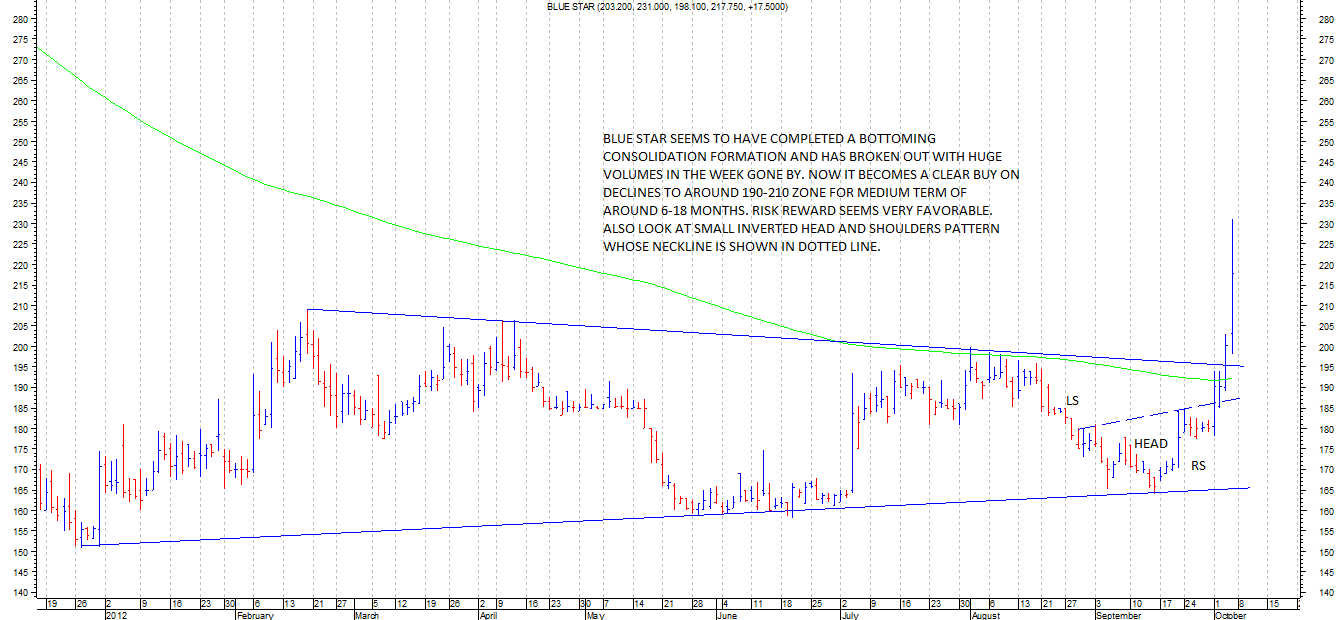

Blue star charts shows an intersting bottoming formation over a very prolonged period. usually bottom formation takes a very long time and ideally a breakout from such prolonged bottom formation would provdie a sustained tradeable upmove. Key remains to buy on dips rather than chasing momentum because one does not want to get trapped at higher levels in stocks that are turning around.

Posted here is the long term monthly candlestick chart of blue star which shows a great opportunity to buy the stock for bigger gains in the medium to long term. Charts seem to indicate that the company might in the near future come out of its woes which have been hurting the performance since past many quarters.

As mentioned in the earlier daily chart, the stock now is seeking support in the earlier mentioned range of 195-210.

blue star is now a turnaround company. go thru the fy 12 AR and chairman’s speech and you will understand why they got into a mess and what they are doing to get out of it.

numbers are negative because company made a loss in fy 12 at the net level.

Blue star continues its turnaround with its q2 fy 13 results.

Sales are marginally down from 590 crores to 573 crores, but company has made net profits of 7.27 crores as compared to loss of 20 crores in q2 fy 12.

half yearly net profit stands at 27.81 crores against net loss of 11 crores in first half of fy 12.

fy 13 could end up with modest profits but I think company will be in full form by fy 14.

If things fall in place as expected then I expect the stock price to touch the upper end of the parallel channel shown above in charts. So for those with a 1.5 to 2 year patience it could offer very good rewards.

Blue Star held its conference call on 23rdOct'12 and was addressed by Vir Advani Executive Director and B Thiagarajan President Air conditioning and Refrigeration products

Key Highlights

Blue Star reported 3% fall in net sales to Rs 574 core, Better OPM on y.o.y basis due to some provisions made in Q2 FY'12 as compared to Nil for Q2 FY'13, lower interest costs and Nil tax due to carry forward losses of last year ensured that the company reported PAT of Rs 7.27 crore as compared to loss of Rs 21 crore for Q2 FY'12.

The company has a carry forward order book position of Rs 1679 crore as on Sep'12, down by 22% y.o.y. Orders worth Rs 200 crore were de-booked during the quarter as a result of them being non moving. As per the management, efforts are made to improve the quality of new order bookings together with slower new order bookings has resulted lower order book.

During Q2 FY'13, order intake stood at Rs 620 crore, down by 8% y.o.y. Management continued to remain extremely cautious on order quality as tough competition continue to remain.

As per the management, things are very uncertain and a quarterly performance cannot be relied upon to determine the entire FY'13 performance. Tight liquidity resulted in higher capital employed during H1 FY'13. Some of the businesses like hotels, residential projects etc, competition was very high and so is the delay in execution while some sectors such as IT and ITES, commercial infrastructure in Tier 2 cities are performing well and comprised about 70% of order inflow in Q2.

Electro Mechanical Projects margin stood at about 7% as compared to negative margin for Q2 FY'12 due to better margin orders, no provisions or write-offs, better after sales and service income etc.

Cooling Products margin stood at about 4.7% as compared to 5.4% margin y.o.y due to unfavorable forex mix and loss in installation of accessories business. The Room AC market was infact down in value terms, although Blue Star grew by 15%. Commercial AC market continued to grow with demand of Refrigeration from Ice cream and Diary products continue to remain firm.

Outlook for cooling product business is also not great as uncertainty on forex front and tough competition continues to hurt the business.

The Industrial Product business and Agency business did not do well as slowdown in capex on infrastructure business and forex fluctuation hurted the business. Fixed costs continue to remain high resulting in lower margins. Outlook continues to be uncertain.

The current borrowings came down to about Rs 425 crore as compared to about Rs 615 crore for Sep'11.

The subsidiary in Project execution business continues to report loss due to some carry forward legacy orders, which are slow moving, and some forex related issues. The subsidiary for rest of the year will continue to report losses.

About 90% of the total carry forward order book is fixed price contracts and rest having some price variation clause attached to it.

On FDI in retail, management indicated that enquiry on Cold Storage business will start only after 20-24 months from now, as the plans currently are on drawing boards only. There is a potential of investment of about Rs 25000 crore in cold storage business over period of 5 years from whenever it starts and the company has all the necessary technology in this segment.

Overall, management is confident of better order booking in H2 FY'13 compared to H1 and most of the orders are expected from Infrastructure segment like Metros, airports etc.

As per the management it is difficult to give a future guidance given the uncertainty, but the endeavor is to bring the order book position to a flat level on y.o.y basis from fall of 22% in H1 and to improve the capital employed level to Mar'12 level.

I am enjoying your fundamental analysis and now your techno funda. Not that I know too much of it but have developed a little skill. It all began when I started reading Point and Figure Analysis by Thomas Dorsey. This is the ABC of technical analysis. However, today with computers and software available, not many are paying attention to this.

The reason for writing this is to share the knowledge i have on Point and Figure. If i receive comments and views on this I will surely begin giving a lot of links on this along with free book on Point and Figure.

So let me know your views as i wish to share knowledge. No one should have a patient on knowledge, the more you share the more you learn.

I have greatly benefited from Donald, Hitesh, Ayush et al. Today my main picks are Mayur, Ajanta, Atul Auto, Indag where I have truly profited from these investments. Thanks once again.

Here is a beautiful article on Blue Star on a blog called State of the Market by Deepak Singh. I am a avid reader of this site. Here is what he has to say:

As you can see in the chart above: Bluestar stock recently broke out above 201 on huge volumes. Now stock has pulled back to levels of 200 againa.opportunity? Doubtsa

Blue star has breached 200 DMA line? Is there a flag formation here? I am not a technical so just wondering whether this is correct or I am completely guessing.

Blue star has breached 200 DMA line? Is there a flag formation here? I am not a technical so just wondering whether this is correct or I am completely guessing.

flag patterns usually dont entail too much price correction. it is essentially a time correction.

here in blue star correction has been deep so cant be considered flag. there seems to be a downward channel sort of formation.

but stock seems ripe for the picking as all the enthusiasm during previous upmove now seems to have gone out of it. always a good time in such situations to pick up stocks.

Blue Star held its conference call on 25thJuly 2013 and was addressed by Mr. Vir Advani, President-Electro Mechanical Projects Group. Mr. B.Thiagarajan President Air Conditioning and Refrigeration Products was not present this time.

Excerpts of the conference call by Capital Market

Order Book stands at Rs.1438 crore versus Rs.1418 crore as of end of March 2013. De-booked a lot of jobs in the corresponding previous quarter hence not comparable YoY.

Within the total order book Rs.250 crore is from Hotels and Hospitals cooling business

Lower Interest costs versus corresponding previous quarter were partially offset by cost on hedging of foreign currency debt

Electro Mechanical Projects and Packaged Air conditioning Systems (EMPS)

Macroeconomic environment continues to be challenging. Hotels, Healthcare, and Industrial biz showed some order demand.

EMPS segment revenue declined almost 7%; however margins were higher than comparable previous quarter. Margin expansion was delayed a bit due to delay in closure of low margin orders.

Increase in inventory and drop in collections observed due to tight liquidity on the client side.

Packaged AC and ducted ACs business has been flat and same was observed in Mar 2013 quarter.

EMPS order wins include JSW and Apollo Hospital Bangalore.

Chiller and Projects market is flat; however company growing in line with the market. 2013-14 is the third continuous year of flat growth.

Cooling Products

Room AC segment has shown good growth after two consequtive hot summer months. Early rains in June slowed down demand a bit.

Room AC segment registered 15% volume growth in the quarter. However input costs pressure was seen in this segment due to Rupee depreciation.

Freezer business grew 20% and Water cooler business saw a growth of 9% compared to corresponding previous quarter

Refrigeration business seeing good traction in Ice Cream makers. Refrigeration has many category of businesses and market share of the company varies from 15-30% across segments

Registered strong growth in Cooling Products segment and maintained both volume and value market share.

Plans to increase margins with increased advertisement and push high value products

Capital Employed in Cooling Products segment decreased significantly as inventory decreased due to good summer sales.

6% increase in price of Room AC was done this quarter to mitigate the impact of rupee depreciation as company imports a lot of components.

Cold storage business margins are the highest for the company but business is still small. Room AC and Refrigeration operate at almost similar margins.

Cold Storage organised market is estimated at around Rs.700 crore, while Blue Star commands 25-28% market share. Primary competitors are Carrier and Ingersoll Rand.

Professional Electronics and Industrial Systems

Agency business suffering due to rupee depreciation

System Integration business is slowing due to poor capex from target clientele

Industrial Products profitability suffered to overall slowdown

Other Management comments

Seeing more price stability in bidding from competitors. However Blue Star may opt out early in some cases of bidding as bid-margin target for the company is higher.

Pressure on liquidity is seen and ultimately squeezing working capital. Last 3 weeks have seen severe liquidity issues.

Not seeing adequate orders at target margins

Some of the manpower cost provisioning of last year charged in this quarter. Excluding the previous year provisioning, employee cost increased 3-4%.

Company is due to give increments to staff and this may impact profits in coming quarters.

Target to keep employee cost low, but it is a big challenge

Debt on the Balance Sheet as of end of 30 June 2013 is lower by Rs.25 crores compared to end of FY13.

Outlook for FY14

EMPS segment to continue to see a challenging business environment

Cooling products business may see rupee depreciation impact, however channel expansion to continue. 15% volume growth observed in Cooling Products may not sustain in coming quarters

FY14 revenue to be lower by 7-10% compared to FY13 due to lower order book.

FY14 operating margins to improve to 7%; this is an initial estimation of FY14 margins as of end of June quarter and may be revised in quarters ahead.

Target to bring down debt levels in FY14 by Rs.75 crore compared to FY13. But this target is looking harder to achieve as working capital issues remain.

85-90% of the net forex exposure is hedged. Borrowings in forex are fully hedged

Next quarter conference call will provide better outlook for FY14