Sumarising my study of Blue Pebble Ltd.- an interior design company, focused on Office Space Designing contracts.

Numbers :

All numbers are from 2024 results from screener. (Crs)

MCap : 110

Sales : 22.06

Operating profit : 5.03

OPM : 22.80%

PAT : 3.75

PE : 21.6

ROCE : 73.11% (Somehow screener shows 147%, felt this was inaccurate hence calculated (op. profit)/ (debt + equity), will try to reason out the high ROCE and if it can be sustained below)

Order Book- 20 cr+ Revenue Guidance- 100%+ growth for FY 25

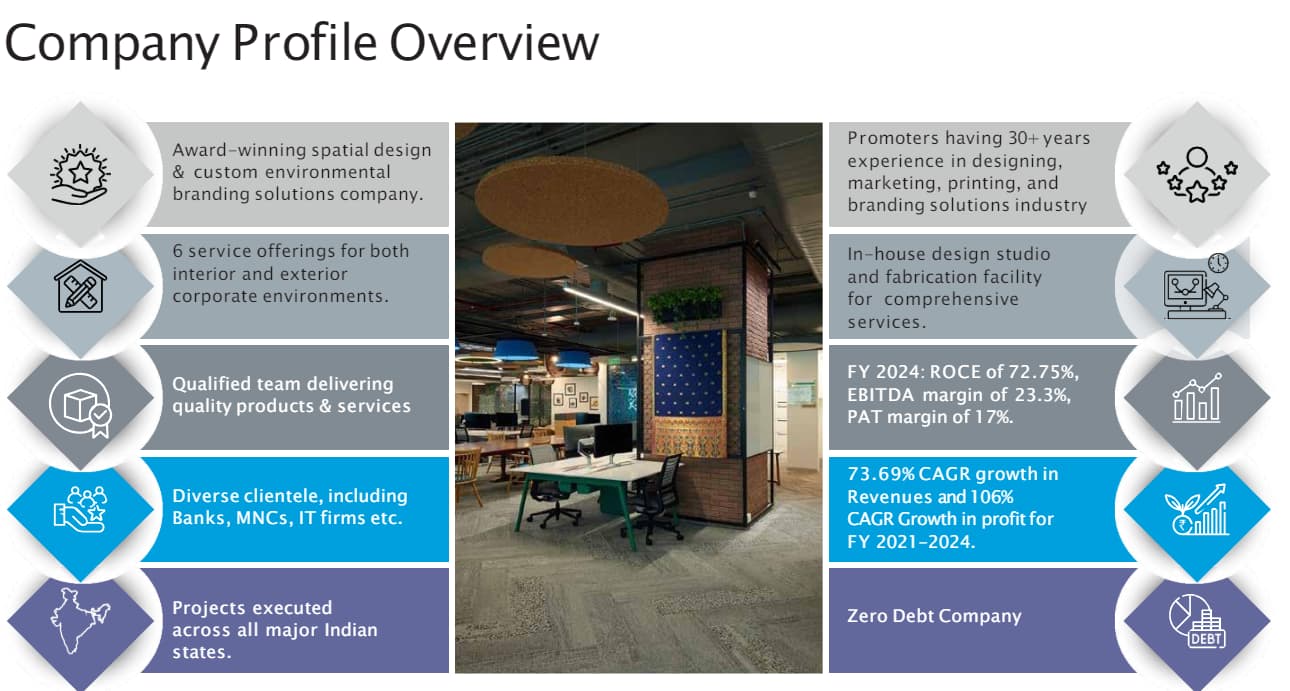

They are into business of creating/beautify office spaces for large MNC clients. First inference drawn can be this isn’t commodity type business and the their past work and its accolades will drive the growth. Also good perception (beauty lies in the eyes of beholder) of their work will give them pricing power to negotiate for quality work.

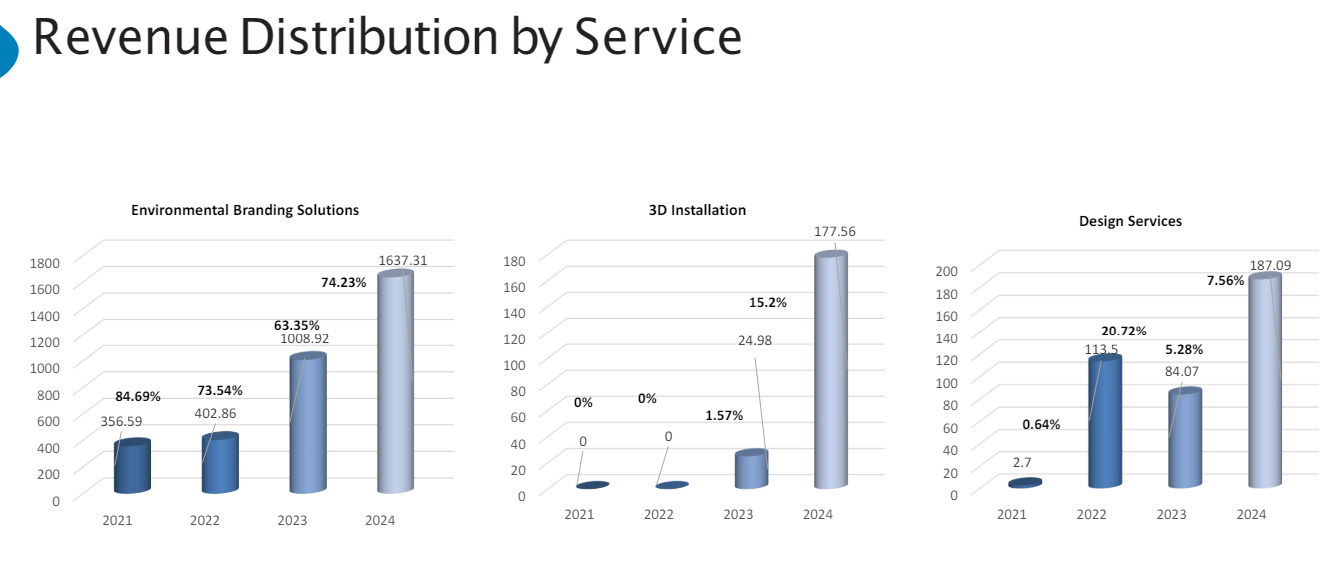

Business is divided into 3 sub cats. Environmental branding - Creates complete theme for the office space designs which is line with what company stands for. 74.23 % of the business 3D installations - Creates wall murals, props for space designs. 15.2% of the business. Design Services - Here company lends their design teams expertise to bring ideas into tangible realities, since the company already has senior designers on their payroll. 7.56% of the business.

Design Services is the segment with highest margins as confirmed by Nalin in one of the call. But I dont think it offers any moat since this can be done any freelance designer too.

2. Growth Prospects (GP)

Business up until now was to beautify the already created and furnished office space. However management is now foraying into creation of complete end product starting from bare shell office. 3M india is first of this kind of project confirmed by management. Here the margins would be thinner but will build a good competitve moat and a good product for MNCs who do not want to deal with multiple parties. Potential growth driver.

Management is planning to venture into hospitality industries, as they also have similar needs for decor and designing.

We know India is the back end office for the world, many MNCs are shifting there development centre to India. This is a growth driver for the company. They should be able to capture good market based on thier past work prospects and clintele list.

3. Management Quality (MQ)

KMPs have 25-30 years of experience(whole experience is not in the same industry). They look confident about the future prospects, we can infer they are smart enough since they have created and listed a positive PAT company within 6 years.

Much cannot be commented about integrity since it is a very new listing and time will tell us, but if they are smart enough an believe in the future they would maintain the integrity.

RISK POINTERS

Competitive space - The ability of the company to grab contracts remains vulnerable to a pricing war amongst competing agencies This can drastically reduce OPM as well. Current OPM at 22.8% for FY 24.

Biggest risk that I see is the growth stagnation in commercial real estate. The company is dependent on corporate infra expansion for future growths.

Lack for diversification currently- Company needs to expand to more service verticals to expand top line and also ensure they are not restricted to commercial Spacial design only.

4. Valuations and Numbers (VN)

Here the things are little interesting if you see above the ROCE is a whopping 73%, this can happen only if the business is very differentiated, unbeatable moat or IP. But i did not see any such thing, what i observed is their cash cycle.

Debtor days: 113.03

Inventory days: 42.35

Payable days: 165.76

They basically have negative inventory cycle and the business is also very asset light.

Asset turnover ratio: 2.52

This implies they dont need very high working capital to grow exceptionally well. Once the profits starts pouring in internal accruals should suffice machinery and new employee hires.

From linkedin we can see there is 9% growth over past 6 months for total headcount, showing management conviction for future growth.

Topline is growing at 74% 3 year CAGR

Current valuations of 21.6 PE looks to be fairly valued with little margin of safety for a fairly new listing.

Competition

I could not find any other listed player in the same space. Mangement confirmed there are not many players who do end to end work and MNCs require this type of agency where they get one stop all solutions.

Management mentioned there are 2-3 players in Mumbai region and 3-4 in Bangalore region.

Surfing over the net i could find one unlisted player - https://www.phidesigns.in/. Though could not find much information on their size since they are unlisted but their past projects also looks good.

Discloser- Invested and tracking for more investments

Interesting. Where did you find the Auditors fees mentioned?

Planning on writing a mail to them in case this arises as a concern.

Also, I might visit to their office in case they allow. Would love to see their set up and meet the team which has produced some genuinely high quality work.

@VibhavB How do you plan an office visit? Do companies allow investors to meet, I always thought you should be a large player to meet the company for investing.

The Auditor fees seem to have increased from 25k to 1 lac in FY 23 (last year). Can be because of extended services requirement for their recent IPO.

Frankly,1 lac seems to be on a lower end?

I agree that 1L in absolute terms is low however, the percentage rise is quite staggering. I am also wondering what exactly the auditor audited, before IPO so their fee goes up by 4x?

In the Annual report FY20-21, the company lends money to 2 people Nalin Gagrani & Manoj Tiwari each 18L. and declared a bad debt of 4L. Am I reading it right that promoters took the debt from their company and defaulted on it?

Related party transactions have also increased 2 fold. looks like the promoters are buying inputs from themselves. Not a great practice to continue and it’s going up and up. would love to have your thoughts on this as well.

Regarding Blue Pebble, agree with MOATs mentioned in the article

For Anti-thesis pointers, would like to add attrition risk in the design team. They have a fantastic team, but such team can be easily poached in the industry by competitors.

Agreed! Any business too dependent on a individual human talent (or that of a particular team), this risk, i believe, would always exist… They may even have a high bargaining power, may all come together and decide to leave and start their own firm (similar to Blue Pebble) etc…

but the question is are there ways we can gauge about how likely this is to happen?

For me, biggest risk would be non-scalability. As their current teams are pretty small, it would be interesting to see how they scale up their team as they grow.

Another concern is customer concentration. Top 10 customers account for roughly 80% of current revenue.

i think if we ask about how the design compensation has been linked is it via ESOP, something that directly linked with company growth means then we can be reasonably assured of attrition of their core design team.

May be some of us should ask the same in next con-call

The design and build business is more of a contractor business wherein you execute the whole end to end project. Its focused on retail and commercial fitouts work ranging from civil n interior, hvac, electricals, etc.,

This business has no entry barrier and you have to block your working capital to churn revenue. If you are ready to invest in Working Capital then you can take as much business as you want.

Project completion and handover is the other critical issue wherein the customer never gives timely clearance and you’re taken for a ride to recover your own money. Snags list from client is forever coming and an usual 3 months project is fully completed in 5-6 months. Also, the retention of 5 percent on all contract is another blocker.

In short, this business will not command a high PE multiple as compared to a niche business or a consulting business.

Agreed that their growth is and probably will be dependent on their order book only! But why do we need them to command a high PE in the first place when growth in the stock price can come directly from the growth of the business itself? Their current order book (as on June 30th) is almost equal to what they did in the whole FY24. And the duration of completion of all the orders is 3-6 months. This would mean that what they did in the last full FY, they would do in the H1 of FY25 itself (which is why they’ve been guiding on an 80-100% revenue growth in this FY).

Moreover they are also actively expanding their presence in the ‘Design and Build’ category which is a high volume/revenue business. Also looking at the tailwinds also we can reasonably assume that the company is poised to do well in the coming years…