Dear Friends, Kindly do not go for growth/theme/big hand/small hands in case of SMALL CAPS. We need to understand the psychology of SMALL CAPS. This counter is in a clear DOWN TREND for almost 1 year and we should always have rule based entry exit with Market sentiments/valuations in small cap investing. Never apply Main INDEX investing rules in small/micro caps. Looking back at 2018 and early 2020 was brutal & 2020-2024 was rewarding for small-cap investors.

Focus on Sentiment/Valuations with Fundamentals. If a company’s growth looks good still liquidity traps and negative market sentiment can keep prices depressed.

3 Likes

There are lot of corporate governance issues in bls international as well please be careful.

1 Like

Can you list out these corporate governance issues?

I’m invested in BLS because of its strong business model and consistently healthy ROE. Ahead of the quarterly results, the stock surged 12.43% today.

In my view, the company has handled the MEA issue in a mature and balanced manner, with no negative or unfocused business decisions so far.

Can we expect strong results this quarter, and could this mark the beginning of a renewed upward cycle for the stock?

Disc: Invested & may have biased opinion

Iam sharing all the data and links,you can analyse and conclude

1)X thread on auditor allegations

- Company pressuring there employees to overcharge the customers,they changed there model before someone else was operating now they only operate and in P&L there margins as well increased but at the cost of this

3)Many governance issues in this article

Main issues from the article if I remember correctly

i)sexual harrasment by promoter group family

ii)some government banned there service after poor service

4)Recent MEA ban on them,i some where I heard they are bribing somone to get the other companies visa contract bidding prices (for this i don’t remember the source exactly)

5)it was indirectly told as an example for siphoning of money ( buying their own unlisted company at very high valuations etc)

Basically there bls e service business somewhere around couple of years back they bought there own other promoter company at very high valuation.

6)1 more thing just a observation,I know there float is low promoter holds 70% and public holds 20%

No respected FII’s and DII’s invested in the company.

3 Likes

So some ill digested rehash of old hearsay allegations which has been very well discussed in the forum . Whats new and whats the point ? Any allegation and any hit job is better than a oligopolistic business at any cost ?

The “Fantastic Results”: For Q3 FY26 (reported Feb 6, 2026), BLS reported a 33% jump in Net Profit and a 43% increase in Revenue. They even declared a 200% interim dividend.

1 Like

https://www.bseindia.com/xml-data/corpfiling/AttachLive/8b4da1e9-a454-4d9f-831a-43a5e34db2d6.pdf BLS International reported strong Q3 FY26 results with a 43.6% YoY rise in consolidated revenue to ₹736.46 crore and a 33.1% YoY increase in net profit to ₹170.22 crore. The company declared a 200% interim dividend (₹2 per share). Growth was driven by visa/consular services and recent acquisitions, despite some margin pressure.

Key Financial Highlights (Q3 FY26 vs Q3 FY25):

-

Consolidated Revenue: Up 43.6% YoY to ₹736.46 Cr, from ₹512.85 Cr.

-

Net Profit (PAT): Up 33.1% YoY to ₹170.22 Cr, from ₹127.91 Cr.

-

EBITDA: Grew 25.3% YoY to ₹198 Cr.

-

PAT Margin: 23.11% (compared to 24.94% in Q3 FY25).

-

Interim Dividend: 200% or ₹2 per share.

Key Business Developments & Metrics:

-

Global Contracts: Secured a 5-year contract with the Slovak Republic for visa services across 80+ countries.

-

Expansion: Secured a new visa contract from the High Commission of the Republic of Cyprus.

-

Subsidiary Performance: BLS E-Services reported a 115.5% YoY rise in total income to ₹286.7 crore.

-

Key Risk: The auditor noted an “emphasis of matter” regarding the going concern status of a subsidiary, BLS E-Solutions Private Limited, following past contract issues.

The 9-month (9M) FY26 performance showed consistent strength with revenue growing 45.5% YoY to ₹2,183.65 crore and PAT rising 36.1% to ₹536.90 crore.

1 Like

Thank you for sharing these.

According to my Guruji, exiting an investment based on a wrong judgment can be very costly.

I would like to take risk and wait for more concrete evidences.

PS : Invested & may have biased opinion

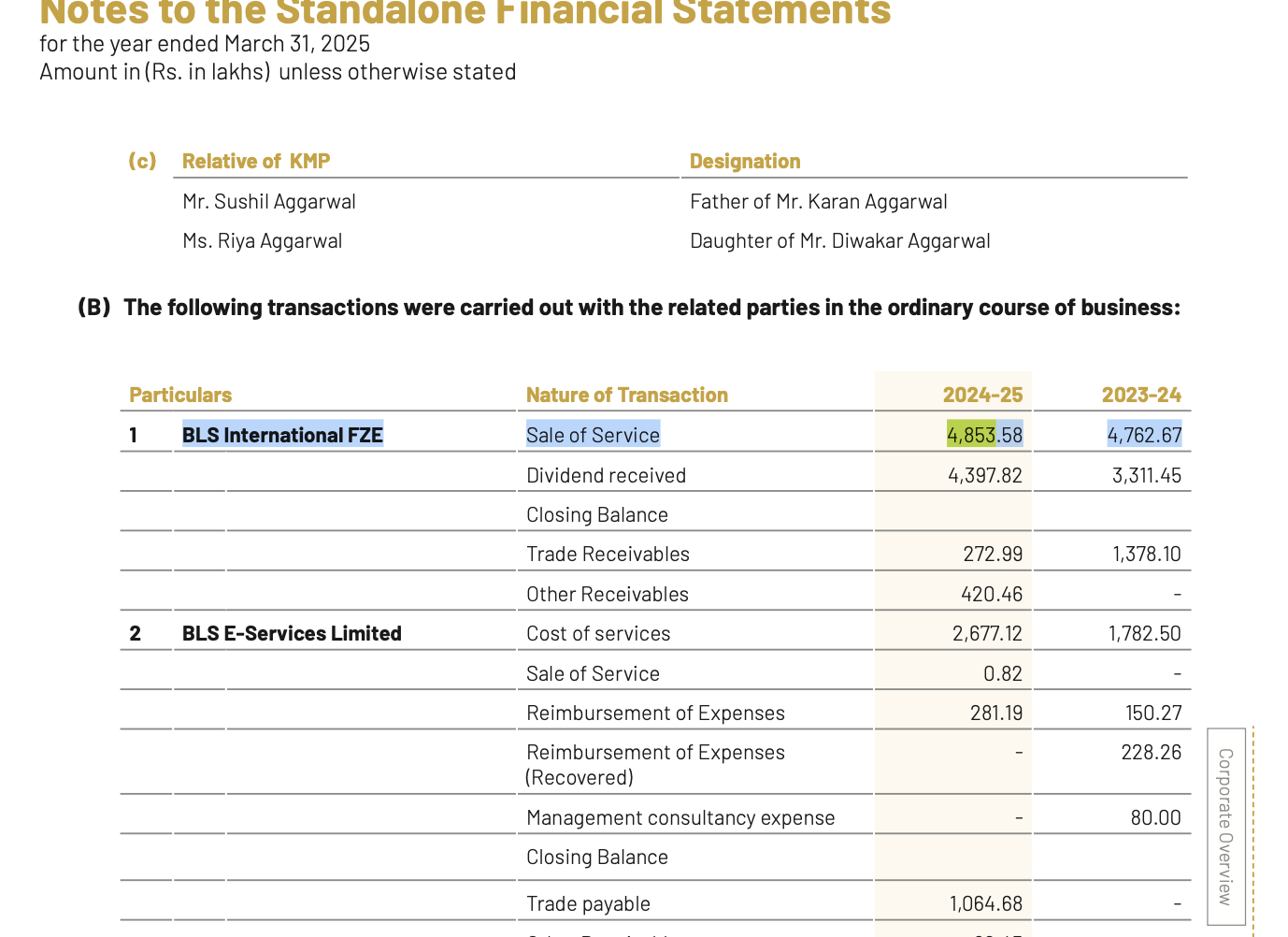

While browsing the RTPs in their 24-25 Financial report, Noticed very large sales to one related party (concentration) Sale of services to BLS International FZE = 4,853.58 (Rs. in lakhs) in FY 2024-25. This is a large chunk of the company’s revenue (standalone revenue = 13,848.63). See the RPT table in screenshot.

With very limited understanding of mine, it looked concerning to me on two fronts

-

Cash-flow circularity — if the listed entity is selling to the subsidiary and the cash is then recycled back as dividends (the report shows dividend received from BLS FZE = ₹4,397.82 lakhs), how to validate if cash was not being siphoned off to benefit specific parties at the expense of the listed entity’s minority owners?

-

high concentration of revenue through a single related entity raises margin shifting concern. the related sale could be priced in a way that shifts margin between entities?

I could not find much of the detail for this sale. If anyone has much deeper understanding, please do post.

Update: This may not necessarily be a red flag and may simply reflect the nature of the business. As I am new to the world of investing, I am approaching this with additional skepticism.

2 Likes

Company’s standalone revenue is minuscule (~6% of the overall revenue) as the company mostly operates through subsidiaries in various geographies. The 49 cr revenue highlighted is for the services provided by parent company to its Middle East subsidiary, which gets eliminated in the consolidated P&L. At a consolidated level it is only ~2% of the total revenue.

PS : Not invested.

1 Like

Any view or information, around the cash position and cash flows generated outside India. This balance is largely sitting in the Dubai subsidiary.

Does he have any plans to repatriate (which might be tax inefficient) / how to he plans to utilise the same.

Additionally, how to value this company in such case?

Consular Outsourcing BLS Services Inc., USA, a subsidiary of this Company is making losses over the last 3 years.

| FY 25 | FY 24 | FY 23 | |

|---|---|---|---|

| -5165 | -9.7 | -4.8 | |

| (*USD) |

I don’t understand why this information seems to be in the blind spot for the investor so far.

After weighing the risk and reward of the investment, I decided to invest in this company. But after digging this dirt from the AR FY 25, I am confused ![]() about the investment.

about the investment.

If this level of loss continues in the coming years, what is the point of these ongoing inorganic expansions or any other ventures?

Valid concern on BLS US sub losses (~₹166 Cr FY25) Its likely ramp-up costs for new contracts/tech integration in competitive visa market, common in inorganic expansions. Consolidated BLS remains robust.

1 Like