Very much agree. Feels like they bough the hotel for personal vacation at the expense of minority shareholders. Corporate governance has always been a sticky issue even with good businesses in India. I’m also invested hoping the duopoly in Visa business will overcome the monkey running a business situation as Charlie would put it.

3 Likes

3 Likes

so this means that the order because of which the price went down has been reversed?

2 Likes

YES!!! That is a big relief and will also help in avoiding a negative point while negotiating new international tenders. So all the best for all of us

DIS- INVESTED

4 Likes

Posting link to the order of the HIgh Court. Worth a read. Long story short

- This space is becoming very competetive. BLS was L1 in only one of the 26 tenders floated by the MEA mentioned in the order.

- MEA claims BLS has a “history of resorting to litigation when it does not win a contract”. There seems to be no history or information is lacking in this order- maybe if one has the timeline of the tenders issued, we can understand if this is a “practise” adopted by BLS or not.

- In at least one of the cases instituted by BLS, the L1 bidder has found to be ineligible and MEA subsequently withdrew the contract awarded to them.

- It appears that BLS has withdrawn at least three WP’s it had filed, post receipt of the SCN from MEA.

- Someone in MEA is not happy with BLS, the SCN and the decision of debarment is obnoxious and looks that MEA wanted to send a message to BLS.

- The ability to win contracts and execute them in this space, at least in contracts with MEA, requires to be in their good books.

Would like someone to add to this

Disclosure: Invested and concerned, reviewing whether to be nvested in the long term.

4 Likes

My take:

Courts rarely cancel government bans unless there are serious mistakes, which is what happened in BLS’s case.

The court accepted that complaints were extremely small—just 0.0008% of over 18 lakh applications—and called the penalty arbitrary.

This supports BLS’s legal and operational credibility.

Although relations with the MEA are strained, they are not broken.

BLS has worked with the MEA since 2008, showing long-term reliance.

The government still depends on private firms like BLS for visa services.

Using courts to defend contracts is normal in regulated industries.

The main remaining concern is reputation risk.

Disclosure: Invested and concerned.

5 Likes

The BLS debarment episode has been quite dramatic. I have tried to piece together the story hoping it will give me better insight into the company.

In Oct 2025, The Economic Times reported: “BLS International debarred by MEA from future tenders for two years”.

This was unexpected. Debarring seemed extreme as there had been no indications of trouble.

The MEA’s order was issued “on the account of allegations including court cases and complaints of applicants.”

This sounded odd: how can one be punished for “court cases’? I was under the impression that BLS had been sued by third-parties. And on the basis of these cases, the MEA was barring BLS.

I was mistaken.

A few days ago (Dec 2025), CNBC reported that the Delhi High Court had ruled in favour of BLS and removed the bar.

Thanks to @Anitha_Govindaraj I read the Delhi High Court order.

Based on the court order and limited information on the internet, here is the story. The parts in quotation marks are from the judgement.

Background

In Feb/Mar 2025, the MEA floated 26 tenders. Based on the lowest (L-1) bid price, BLS was awarded one out of 26.

In Mar 2025, BLS challenged 5 of the other 25 tender awards in the Delhi High Court. I will refer to these “Cases” again.

On 3rd Apr 2025, the Court passed Interim Orders that the award of contracts would remain subject to further court orders, i.e. it was considering the matter.

Around this time, MEA’s Mission in Norway imposed financial penalties on BLS for non-compliance. BLS paid the penalties but later took the matter to arbitration.

In Apr/May 2025, BLS filed a case with the Delhi High Court, questioning the award of a tender to Alankit Limited. Alankit Limited should have been disqualified for alleged criminal cases. The ED has filed cases against Alankit Limited and its director Ankit Agarwal.

Before the court could rule on this, MEA barred Alankit Limited for two years. The case was dropped. (As an aside, Alankit Limited is a listed company but it has not informed the stock exchanges about being debarred by the MEA. The only information I could find are some social media posts.)

On 1st Aug 2025, the MEA issued a Show Cause Notice (SCN) to BLS. The SCN proposed to bar BLS from future tenders because of:

(i) history of complaints and unethical practices;

(ii) financial penalties imposed on BLS;

(iii) BLS’ alleged impairment of fair competition;

(iv) monopolistic behaviour and pattern of misconduct;

(v) repeated tender challenges targeting other L-1 bidders ; and

(vi) the public interest impact of such acts committed by BLS.

The SCN said the complaints received by the MEA included:

(i) lack of transparency in the service fee;

(ii) overcharging applicants;

(iii) poor response to applicants’ requests;

(iv) exploitation of blue-collared workers by charging hefty prices for services; and

(v) compelling applicants to pay extra charges for Value Added Services.

The SCN gave details of fourteen complaints but said that “hundred of complaints” had been received.

MEA claims that BLS “stalled the tender process and destabilized the newly discovered L1 price by filing frivolous litigations against the L1 bidders.” This was seen as anti-competitive behaviour and an attempt to create/maintain a monopoly.

BLS claims it was “informally asked to withdraw” the Cases, “failing which its response to the SCN would not be considered”.

The MEA has not pushed back on this. The judgement makes a passing reference to it saying that the Cases “were withdrawn by the Petitioner, after issuance of SCN … and under threat of debarment.”

BLS withdrew the Cases, hoping perhaps that the MEA would show leniency.

The company responded to the SCN on 14th Aug 2025. There was a personal hearing as well.

On 9th Oct 2025, the MEA barred BLS for two years.

BLS took the matter to the Delhi High Court and made the following claims:

(i) the MEA gave no justification for imposing the two-year debarment which is the maximum possible under the Government Procurement rules.

(ii) of the over 18 lakh applications processed between Jan 2024 and Jul 2025, the MEA showed/relied upon only 14 complaints for this order.

(iii) litigation cannot be seen as anti-competitive as defined by the Code of Integrity in Government Procurement rules.

(iv) only the courts can determine if litigation is frivolous. The Delhi High Court had passed an interim order in the Cases - that were prematurely withdrawn - indicating there was some merit to them.

(v) Debarment should be used as a measure of last resort.

(vi) Monopolistic intent must be established by the Competition Commission of India and not by the MEA.

In court, among other points, MEA contended that

(i) it had received numerous complaints. But “attaching all of them would have made the SCN voluminous”. Moreover, BLS “never requested copies of the complaints cited in the SCN”.

(ii) Many embassies had imposed financial penalties on BLS. BLS paid off penalties in March 2025 at the last minute to be eligible for the open tenders. And then tried to get the penalty amount back through arbitration once the tender closed.

(iii) it reiterated its views on frivolous litigation and anti-competitive behaviour.

(iv) and that “the Courts [should] only examine the decision-making process of [the MEA] but not the decision itself.”

The Judge found the following:

- Debarment or blacklisting is an extreme step and must not be taken lightly.

Blacklisting is like “civil death” as it “sets off a domino effect” - the entity is not able to bid for any government or PSU tenders.

“a mere breach of contract or a contractual difference/dispute is not enough to warrant a debarment/blacklisting action. There have to be strong, independent and overwhelming [reasons] … given the drastic consequences”

“Once the final order blacklisting the Contractor is passed then the Contractor is left with no other option but to go to the High Court… This again would lead to unnecessary litigation in the High Courts. The endeavour should be to curtail the litigation and not to overburden the High Courts”

“if a contractor is to be [blacklisted] … the nature of his conduct must be so deviant or aberrant so as to warrant such a punitive measure. A mere allegation of breach of contractual obligations without anything more … does not invite any such punitive action.”

-

As the matter is one of debarment or blacklisting, the Court will review not just the process but also the decision.

-

The MEA should have shared all complaints (not just fourteen) it used as the basis of the debarment. And it should have given BLS the opportunity to respond.

-

The court asked MEA to provide “data pertaining to the number of complaints received in respect of other service providers engaged by it for the calendar years 2023-2025 … [The court found] that complaints have also been received against other service providers. However, there does not appear to be any Standard Operating Procedure or guidelines which prescribe a threshold number of complaints that would justify debarring or blacklisting action.”

Effectively the court said that given that the MEA receives complaints about several service providers, there needs to be a standard process of determining whom to blacklist on the basis of these complaints.

The court pointed to the debarment guideline issued by the government that requires specific complaints and not "generic reference to the ‘persistent repetition of identical issues’ and to ‘hundreds of complaints’”

- The court did not attribute malice to either the timing of the payment of penalties by BLS, or to the arbitration to contest the penalty.

In the matter of the Norway Embassy/Mission penalty, the court said: “… it is pertinent to note that although the [MEA’s] Mission/Post at Oslo, Norway imposed penalties upon [BLS], the record reflects that no complaint was ever received by that Mission against [BLS], thereby rendering the basis for such penal action unclear.”

- The court recognises “that the extensive litigation initiated by [BLS] may have caused considerable inconvenience to the [MEA] and may have disrupted the tender process/es, [but] such conduct … cannot be treated as conclusive evidence of” bad intent.

“Debarment on the ground of ‘litigiousness’ would create a chilling effect, dissuading the bidders from questioning tender conditions even if they are arbitrary or discriminatory. Such an approach would foster unquestioned executive discretion”

Permitting the debarring of an entity for frivolous litigation would “legitimise retaliatory action by the State in the form of ‘debarring’”

- On BLS’ anti-competitive behaviour: “legal proceedings by [BLS], even if directed against successful L-1 bidders, cannot by itself constitute ‘anti-competitive behaviour’ … the right to access courts is a constitutional right”

“Anti-competitive behaviour” includes “collusion” and “bid rigging”, but cannot include exercise of legal remedies.

- The MEA “has failed to furnish any justification for prescribing a two (2) year period of debarment”.

And “the imposition of a two-year debarment appears to be mechanical and arbitrary”

- The debarment is removed. But the MEA is permitted “to issue a fresh show cause notice in case it is sought to debar [BLS] on the ground of alleged substandard quality of work/services.”

=================================

Thoughts:

-

BLS has won the battle but the war may not be over. The MEA can reissue the SCN.

-

Based on this judgement, and the information provided by the MEA, it seems unlikely that it can bar BLS unless the complaint volume is truly overwhelming especially in comparison to other service providers.

-

There is stiff price competition for BLS in the MEA tenders. The fact that it won just one of 26 tenders is concerning. But if there is a race to the bottom - with everyone slashing prices - losing some tenders and waiting for the other guys to implode is a better strategy, particularly if you have staying power.

-

BLS lost the battle for the 5 tenders it filed the Cases for. But given the Alankit Limited case, and the interim court order in the Cases, BLS is right to contest these tenders. The company is on its toes vis-a-vis competition.

-

With this skirmish, there is/will be bad blood between the MEA and BLS. But as ministers and bureaucrats change, the relationship may improve.

-

Warren Buffet views management integrity as a key issue when investing in a company. Reading the judgment, at no point did I feel that the BLS management were the bad guys in this drama. Of course, absence of evidence is not evidence of absence. However, best to assume that one is innocent till proven guilty. BLS has conducted itself well under pressure.

34 Likes

Hi,thanks for putting up in the concise manner.

3 Likes

Hi Amit

Appreciate the detailed study and summarizing it so well that even a layman can understand the developments. A big thank you for sharing this information.

Now as a follow up thought, MEA is stalwart ministry in current government so change of minister and or top official handling this should be ruled out and thats the reason I guess market has not responded well to favorable ruling by court.

So how does it work out for BLS? Managing Government is a key competency in the business at which they are struggling.

We all know that India business ( Indian MEA) is 12-15% but having a weak footing on home country does not bode well. I heard VFS is also planning to come up witj IPO. So in the 25 tenders opened this year any idea how many were won by VFS Global?

Regards

1 Like

how is this different or same as BLS E-Services Ltd? I see posts here that seem to talk about e-governance services AND visa processing. are they being done by the same company or split between the 2. am even more confused by screener’s BLS E-Services Ltd being called a subsidiary of BLS international

Can someone clarify on the relationship between the 2 and whether investment options are to be done on both or just one(am NOT asking for a recommendation to buy, just asking which one does which services)

Here is the corporate structure from this IDBI note.

Broadly, an investment in BLS E-Services gives you exposure to the India-focused part of the business and excludes the consular services.

With BLS International you own the consular services and half of the e-services business.

If you want to get into the weeds, the IDBI note (link above) is a good source.

2 Likes

Thank you very much, that clarifies things.

1 Like

Re your second question, I have struggled to find data. Here is some dated information from Jul 2025.

BLS had 6 contracts. VFS had 7.

1 Like

Reasons Why BLS International Stock Has been Suffering Since January 2025 (Crashing 40%) And a Possible view upon when can Stock Recover ?

Slowed Growth in Revenue & Profits

Although the company has delivered exceptional growth in the past, such an extraordinary growth trajectory is unlikely to continue in the near term. This is primarily due to the relatively small scale of acquisitions undertaken during the current year and the fact that the base year has already become significantly high. As a result, growth is expected to continue, but at a more moderate and normalized pace.

At this stage, valuation becomes a key consideration. The stock has corrected sharply, and current valuations appear attractive even when benchmarked against the slower growth outlook guided by the management. This creates a potential opportunity; however, meaningful upside will likely require confirmation through strong volume participation.

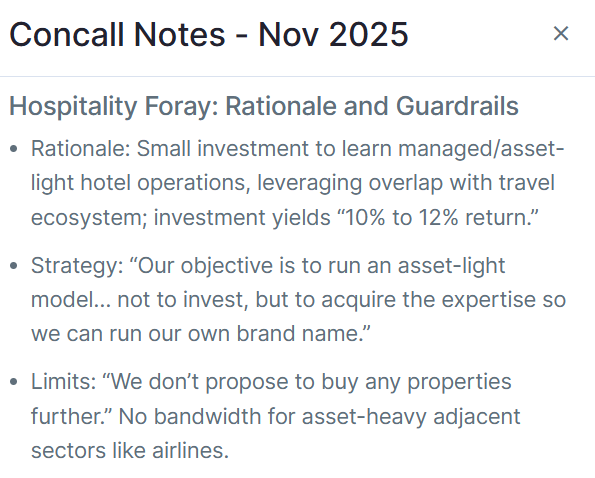

Investment in Hotel Business

One additional factor contributing to investor anxiety is the company’s decision to enter the hotel business. The long-term outcome of this diversification remains uncertain and will be determined over time. If the hotel business underperforms but the core visa services business continues to execute well, the stock can still deliver reasonable returns. Conversely, if the hotel business starts contributing positively over time, it could act as a strong growth catalyst. However, if it fails to perform, it may become a drag and potentially dilute management focus from the core business.

At present, the scale of investment in the hotel segment is relatively small (approximately ₹83 crore) when compared to the size of the company’s core operations. Hence, the immediate financial risk appears limited. The impact would become more material only if the investment scale increases meaningfully.

While investor concerns are understandable, companies often take strategic decisions to diversify. The key factor to monitor is whether such decisions have any adverse impact on the company’s core visa services business. As long as the core business remains unaffected, the downside risk appears contained.

Worsening Relation With Government of Home Country India

We are seeing from january since BLS has initiated litigation against MEA in court for MEA not giving BLS the orders and Assigning orders to the new L1 bidders. Since then series of events have shown that how this relationship has worsened overtime.

But Given the valuations stock is trading at: There can be a huge opportunity if : Stronger volumes may emerge, and that will happen when, there are visible signs of improvement in the company’s relationship with the Ministry of External Affairs (MEA), which should be closely tracked through ongoing news flow. Alternatively, a change within the MEA—such as the transfer of officials who previously had strained relations with the company—could also act as a sentiment trigger.

Additionally, any significant overseas acquisition could be a major positive catalyst, particularly if it reduces India’s contribution to overall revenue from the current ~12% to around 4–5%, thereby further de-risking the business model.

4 Likes