http://www.bloomdekor.com/products/ is the website of the company. With that out of the way, Lets look at the ratios and take some confidence before I introduce you to the nature of the business.

Market Cap.:

₹ 19.83 Cr.

Book Value:

₹ 25.40

Stock P/E:

8.16

Dividend Yield:

2.07%

Face Value:

₹ 10.00

Enterprise Value:

₹ 48.20

EPS:

₹ 3.55

Graham Number:

₹ 45.04

EBIT:

₹ 6.63 Cr.

EVEBITDA:

5.09

PEG Ratio:

-1.23

Debt to equity:

1.81

OPM:

15.22%

Return on equity:

4.25%

Return on assets:

8.07%

Average return on equity 5Years:

0.37%

Dividend Payout Ratio:

59.42%

Exports percentage Now:

0.00%- It used to export earlier

Exports percentage 5Years back:

21.58%

Promoter holding:

52.02%

Piotroski score:

7.00

Altman Z Score:

1.86

Profit growth 5Years:

-6.62%

Profit growth:

248.17%

YOY Quarterly profit growth:

176.36%

CROIC:

14.13%

OPM 5Year:

8.58%

Sales growth 3Years:

5.40%

Operating cash flow 5years:

₹ 27.45 Cr.

Average return on capital employed 10Years:

7.11%

Average return on capital employed 3Years:

8.59%

Return on invested capital:

12.03%

Investing cash flow 10years:

₹ -24.79 Cr.

Cash from operations last year:

₹ 3.95 Cr.

Inventory:

₹ 32.34 Cr.

Days Inventory Outstanding:

193.58

Profit growth 3Years:

6.37%

Market Cap to Sales(Kenneth Adrande metric):smile:

0.32

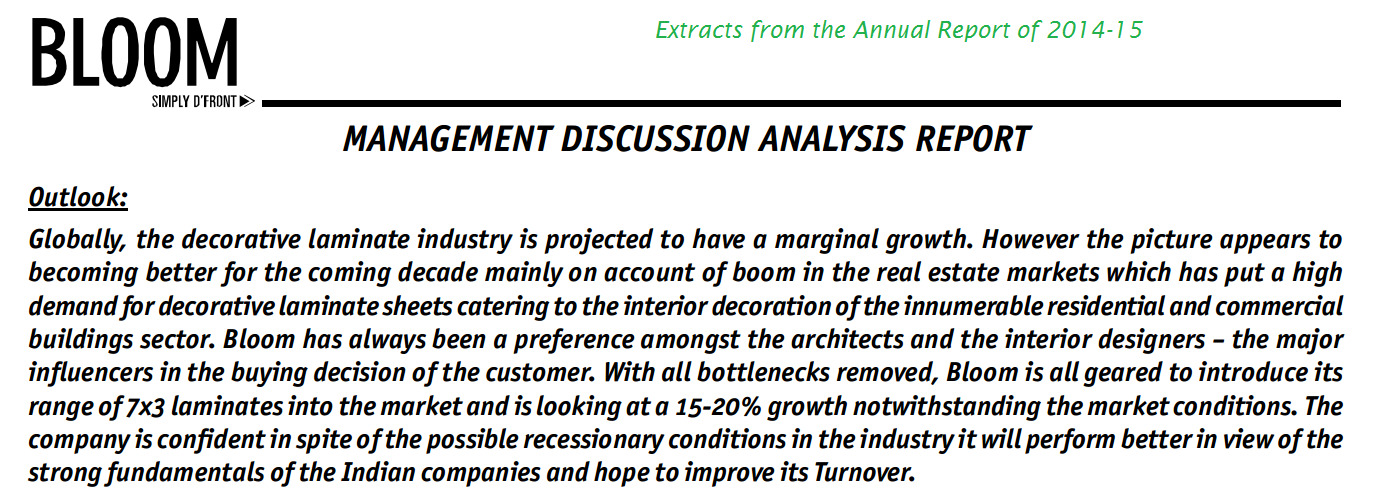

Now the funny thing is Times of India has a holding in this company. It has been doing well for itself as the above ratios state and most of all its a small company, so small that price action can make it hit either circuit filters on Index. Its known to a few as a door making and a designer company. It is involved in e-commerce and selling advise online. Its brands are Bloom and Olive. They are a company from Gujarat and have a solitary plant where they make the products from wood and its wastes. It has branches in all major metros.

On the plant, this is what they say:

A long awaited continuation of the prelude, a brand new collection with the same values.

Elegant and contemporary, yet reminiscent of the classic. Authentic

wood-grains offer immense warmth and satisfaction. Interiors of today

demand a fresh look, where one’s eye is always in search of the

not-so-seen.

URBAWUD collection intends to address this need, to assist designers

create contemporary interiors for the existing urban lifestyle and

tastes.

Bloom Dekor is proud to present this special range of Laminates that

also include improvised colour tones of authentic wood-grains.

Address:

Bloom Dekor Limited

2/F, Sumel, S.G. Highway, Thaltej,

Ahmedabad – 380 059,

Gujarat (India)

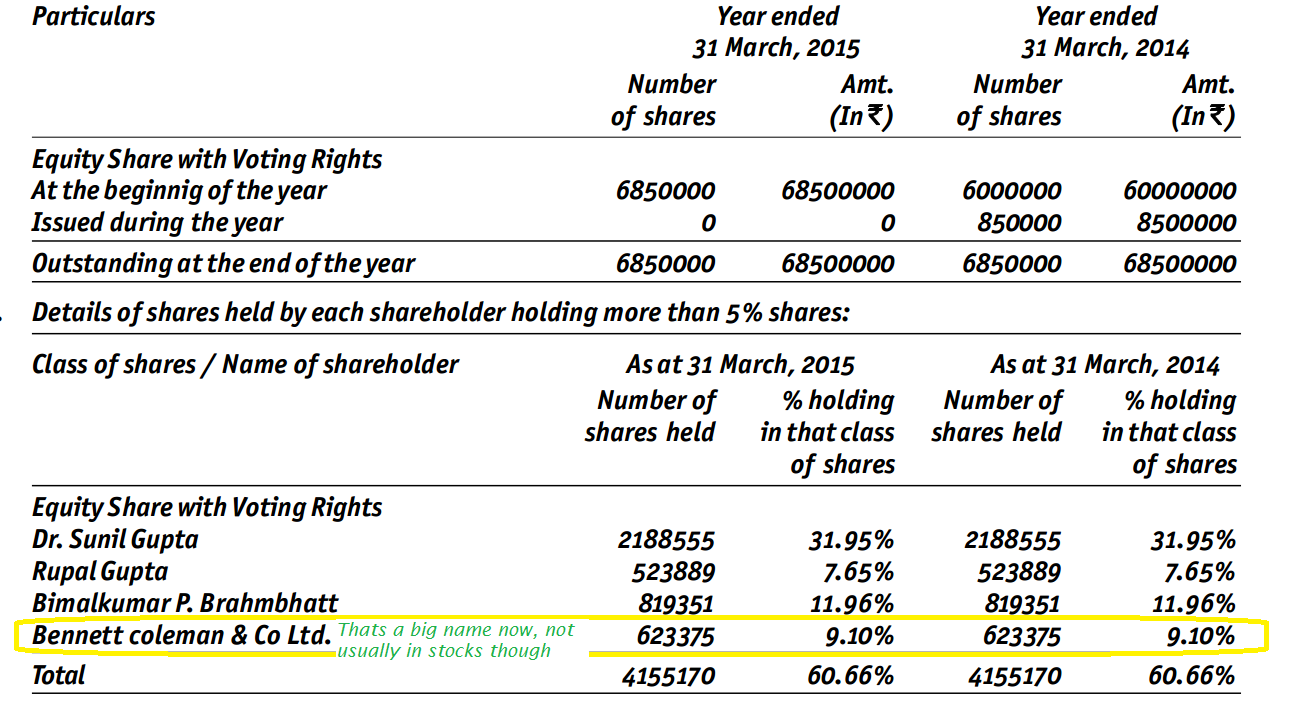

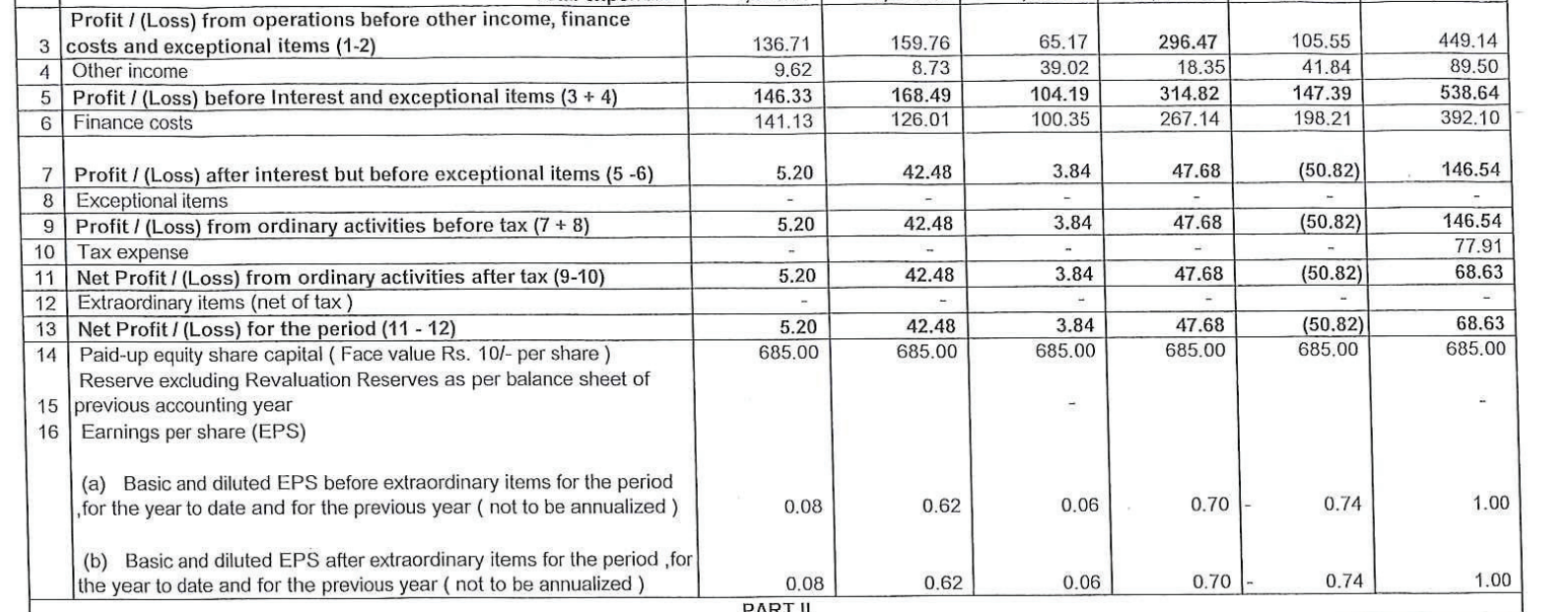

Big news is that, it pays dividend and quiet frequently. Its also growing its OPM very consistently and generates cash flows.5262250315.pdf (2.7 MB) Take a good look at this awesome looking design of Annual Report and pass comments on the quality of it. What Bennet and Coleman knows that we dnot know, lets find out?

I invite @Donald@ayushmit@MoneyWorks4ME@vml@pratyushmittal and others in making the case easy for me and others to understand this business, and if as I feels its just another company or its a opportunity in the future if it starts showing any growth and develops a model

Bennet & Coleman has stake in a lot of cos where they take stake in lieu of advertising and what is called "paid news " . Can anyone point out if they indeed paid cash for their stake .

Indian Plywood Industry - Value Migration On The Way

The

Indian Plywood industries is at the cusp of a new era. Over the last

few years, the organised players (Century Ply, Green Ply, Kitply etc)

have been growing at double the rate of the overall industry. This

signifies that there is value migration happening from the unorganised

unbranded products to the organised branded ones. The overall organised

sector is growing 20-25% CAGR. Organised sector is 30% of the overall

plywood sector.

The overall plywood

industry size is Rs. 180 billion (source: Greenply AR 2015). The MDF

industry size is Rs. 13 billion growing at 15-20% over the last 5 years.

MDF

is engineered wood made from wood (fibres), glued together using heat,

resin and pressure. It is also a superior substitute for cheap

unorganised plywood. It faces competition from imports. Demand in

this sector is driven by ready-made modular furniture, modular kitchen,

ready-to-move into offices/retail outlets, a need to substitute low

quality plywood, affordability, increasing awareness of customers of

better alternatives and shortage of time.

The

Indian govt has imposed a ban on new licenses for manufacturing due to

the environmental impact. This will help the existing majors.

Growth Levers

GST & its impact

• Remove inter-state tax anomalies

• Remove differential with unorganized sector hence a value migration from unorganized to organized players

Other growth levers

• Home renovation cycle is declining

• India’s per capita income rising along with disposable income

• Rising urbanisation and aspiration levels amongst people

• Govt focus on “Housing for All” – Rs 22,407 crores allocated by

FinMin for 2015 to create 6 cr (2 cr urban + 4 cr rural) complete houses

by 2022

• Government Announcement regarding construction of 100 smart cities

• Focus by HFCs on Tier-2, Tier-3 locations

Over

the short term (< 1 year), the industry may have moderate growth

owing to the subdued demand in real estate sector. However, the growth

levers are likely to kick in over the medium term (2-3 years). The

industry looks to have bright prospects over the long term (10 years).

It would be interesting to keep a watch on Century, Green and any new

player in this space.

Please check this link which is a SEBI document which talks of promoter violations of regulation 11(1) read with Regulation 14(1) three times during the year 1998-2000

I am from Ahmedabad; so i am aware that Bennett & Coleman stake in the company is in lieu of the advertisements in the newspapers. Locally I have many times noticed half page ads of Bloom decor in TOI. They have lots of stake in such companies so nothing much to be take from that.

as per screener,in last 3 year sales cagr is 5.4% and pat cagr is 6.37% and ROE 0.5% . I think we must also see if sales get cannibalised to suncare traders ltd a pvt ltd co where Mr Gupta is also a director.

what are its reasons for them to give stake in the company instead of giving them cash. Its not wise for ToI to accept shares in a company if its not good. Next point is that you are saying that there are big ads in News paper, thats a sign that they are focusing on growth and want sales and marketing is a way they want to achieve it. I never saw any ads, so you tell me what you @manish26 think about the brand, the respect it has and if people buy these products and visit their decorated website

Just for the records, Bennet Coleman had a stake in now bankrupt Vishal Megamart and Edserv SoftSystem. They are very liberal if the company is ready to give them a stake in lieu of advertisement and don’t analyze companies strengths and weaknesses.

@suns Bennet Coleman having a stake is no positive in itself. Infact it could be more a negative because of most of the places i have seen their name going up. They famously used to subscribe to Karuturi Global shares in preferential allotment at 5x the market price in 2010. See where it has got them. Apart from TOI, if you see some fundamental change happening its ok but Bennet Coleman should be irrelevant in your analysis. That i can say from my personal experience

Can anyone put a fresh insight on this stock? Is there anything substantial in the stock that one should invest in it? It is trading a Suncare Traders on BSE.