Company 1:

KOVAI MEDICAL CENTRE & HOSPITAL

Sector: Healthcare

Industry Overview:

-

Currently, healthcare is highly underserved as compared to other nations, and as well the WHO recommendation of having 4.9 mn beds for India (currently 2 Mn beds only)

There is a huge demand-supply mismatch in India as the World average of hospital beds is 29 (per 10000 population), and India has only 15. -

Along with this, Indian hospital chains have undergone consolidation for the past few years, growing at just 2% CAGR FY17-24 and are expected to catch up speed at CAGR 10% by FY27E

-

Insurance Penetration is also rising in India, and has one of the highest out-of-pocket expenditures as compared to the rest of the world

-

Lastly, medical tourism is coming back to pre-covid levels, which is a positive sign for the sector as India is a hub for affordable medical destinations for at least nearby countries like Bangladesh

Promoter Overview

- Highly experienced promoter and management with decades of experience and doctor by profession

Business Overview: All their centers are located in or around Coimbatore; they

- KMCH Main Centre: This is their primary revenue stream, contributing 70-75% Rev, one of the largest Tertiary Care Hospital in south India

- Investing highly in deploying the latest tech in orthopedics, neurology, oncology, etc streams which have higher ARPOB

- Medical College : Rev contribution is 7-9%, focused in providing affordable healthcare,lower ARPOB

- Rest are satellite centers focussing on diagnostic centers and primary care

Key Metrics:

- ARPOB: Back to pre-covid level, although their ARPOB from the main center is way higher, around 28,479, as compared to 20,173 at the group level due to affordable healthcare

- ALOS: Reduction in this to 4.06 (lowest in past 4 years) is showing good signs of higher churning

- INPATIENT & OUTPATIENT : Both growing at a decent rate of ~10% CAGR

- Occupancy Percentage: Back to pre-covid levels of 60% (can be improved)

I NEED TO KEEP TRACK OF THESE METRICS EVERY QUARTER

Key Triggers / Variant Perception/Thesis

- Capacity Expansion in Main Hospital - assuming 250 beds to be added (hostel being shifted will contribute ~100, and new block coming up ~ 150 (functional from Q4); will generate 135 Cr. need to keep track

- New Hospital in Chennai: Bough new piece of land in Aug in Chennai; assuming 250 beds, 180 cr impact from FY27 need to check again

- PG Programme: Start of PG Programme, ~ 3Cr. impact on Rev

- Board approved purchase of 1.11 Acre land on 18th Mar 2025, need to know more details

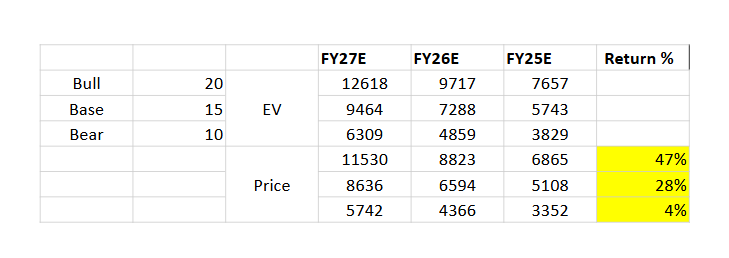

Valuation Analysis

Keeping in mind the above developments and assuming 10-11% Growth from existing revenue streams, attaching my calculations, * WILL REVISIT THIS ANALYSIS EVERY QUARTER*

Key Risks

- Geographical Concentration: Currently concentrated in Coimbatore, need to keep track of Chennai expansion closely about how it turns out

- Lots of competition intensity

- Regulatory risks- a cap on the price of treatments, etc

Will add more to it once Q4 FY25 results are out