Introduction

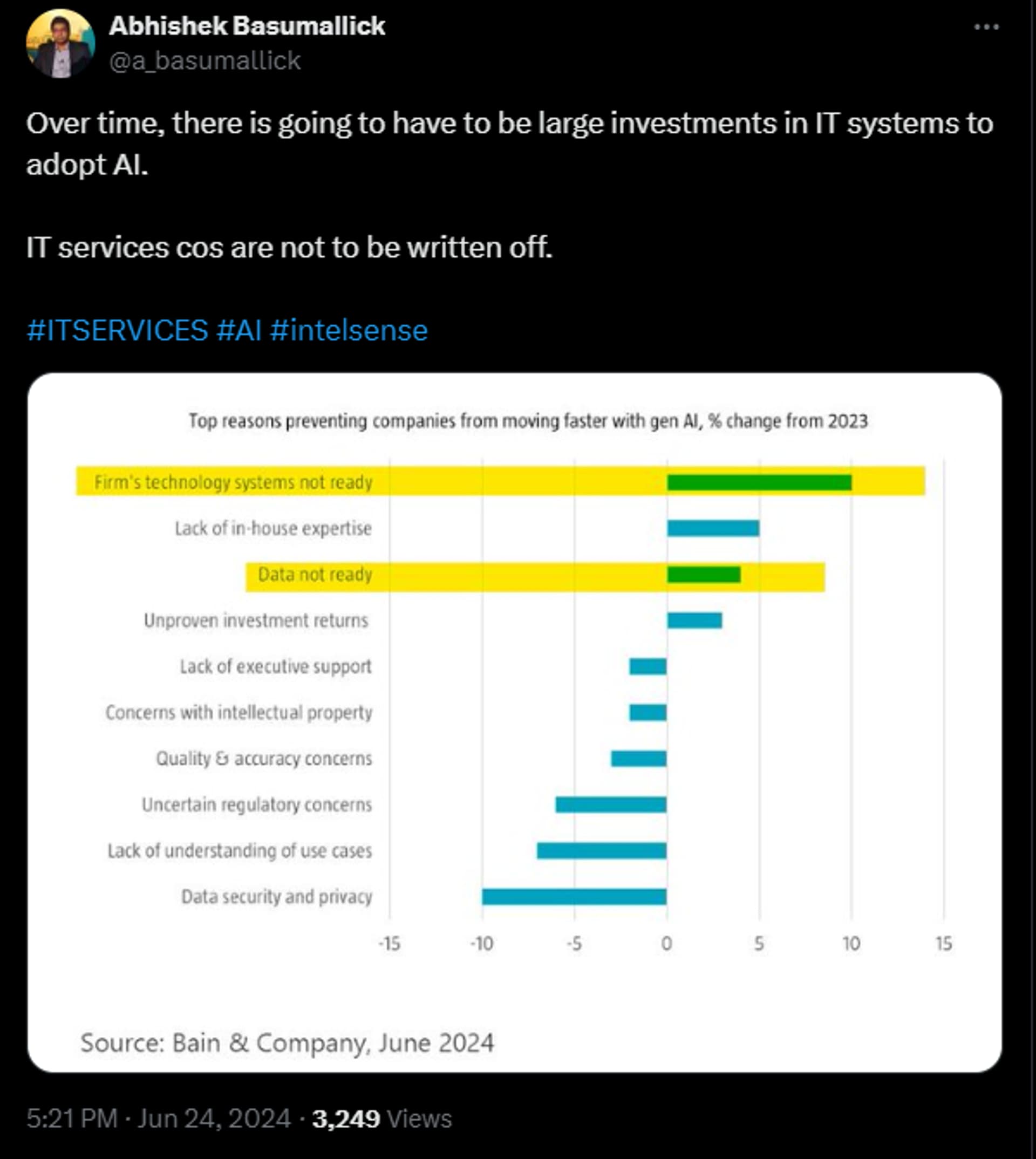

I recently came across this tweet by Abhishek Basumallick (@a_basumallick) that highlights the significant role of IT infrastructure in the world of AI.

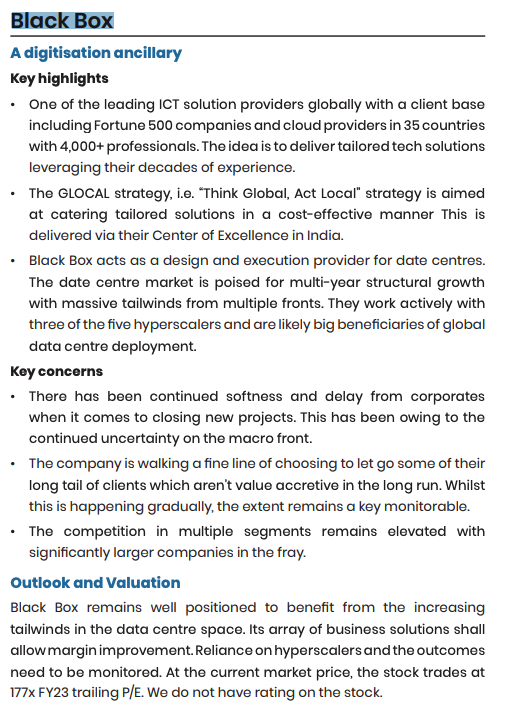

One such under-researched and under-owned (FIIs & DIIs combined, own <5%) IT infrastructure company in India with global presence is Black Box Limited.

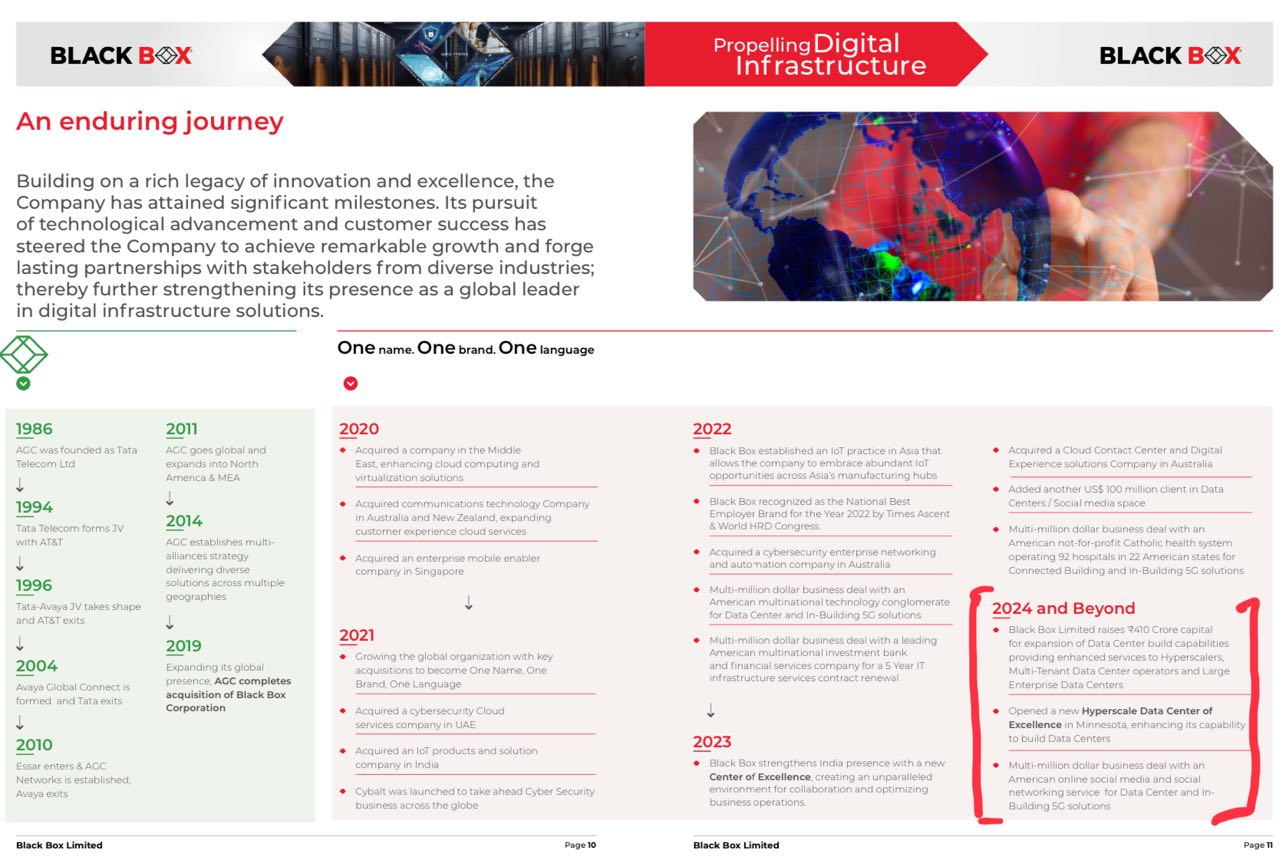

Originally a US-based company listed on Nasdaq (NASDAQ: BBox), Black Box faced financial troubles and was acquired by AGC Networks Limited (NSE: AGCNET), owned by the Essar Group, in 2019 for about $16.6 million (Rs. 121 crore) in cash. At the time, Black Box had revenues of $656 million, while AGC had revenues of $100 million.

Following the acquisition, AGC Networks renamed itself Black Box Limited, adopting the identity of its larger acquisition to establish a global presence. The company moved its backend operations to India, significantly reducing employee costs. This transformation helped streamline operations, reduce costs, and improve both gross and EBITDA margins, leading to significant improvements in the company’s bottom line.

Source: Screener.in

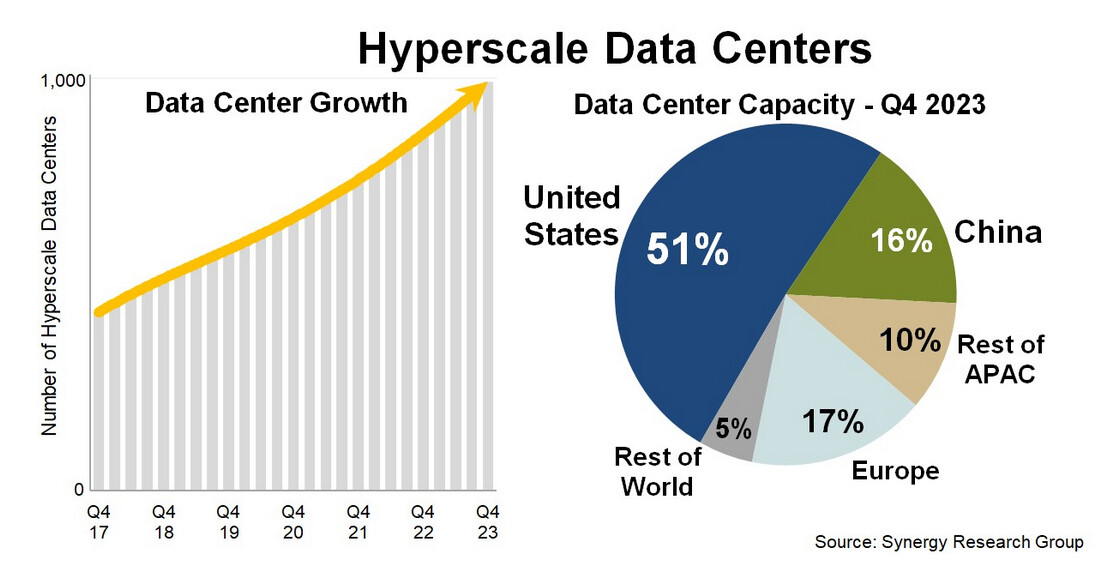

Today, Black Box serves major clients like Meta (Facebook), Amazon, Microsoft, Google, Intel and Bank of America among others. The company counts 250+ of the Fortune 500 companies and 3 out of 5 hyperscalers in cloud technology among its customers. Meta alone accounts for over $100 million in annual revenue.

Since the acquisition in FY19, Black Box has consistently delivered growth and improved margins. Management projects $2 billion in revenue within the next three years, with 10% EBITDA margins. For FY24, the company reported $756 million in revenue with an EBITDA margin of 6.8%. Company today has a market cap of little less than $800 million.

Black Box has two $100 million+ accounts and is strategically shifting to increase its share of large corporate clients while reducing its focus on smaller, less profitable ones. This approach aims to reduce long-tail costs and lower SG&A expenses and enhance profitability.

Acquisitions seldom succeed in delivering promised synergies, but Black Box is a rare success story!

More about Black Box

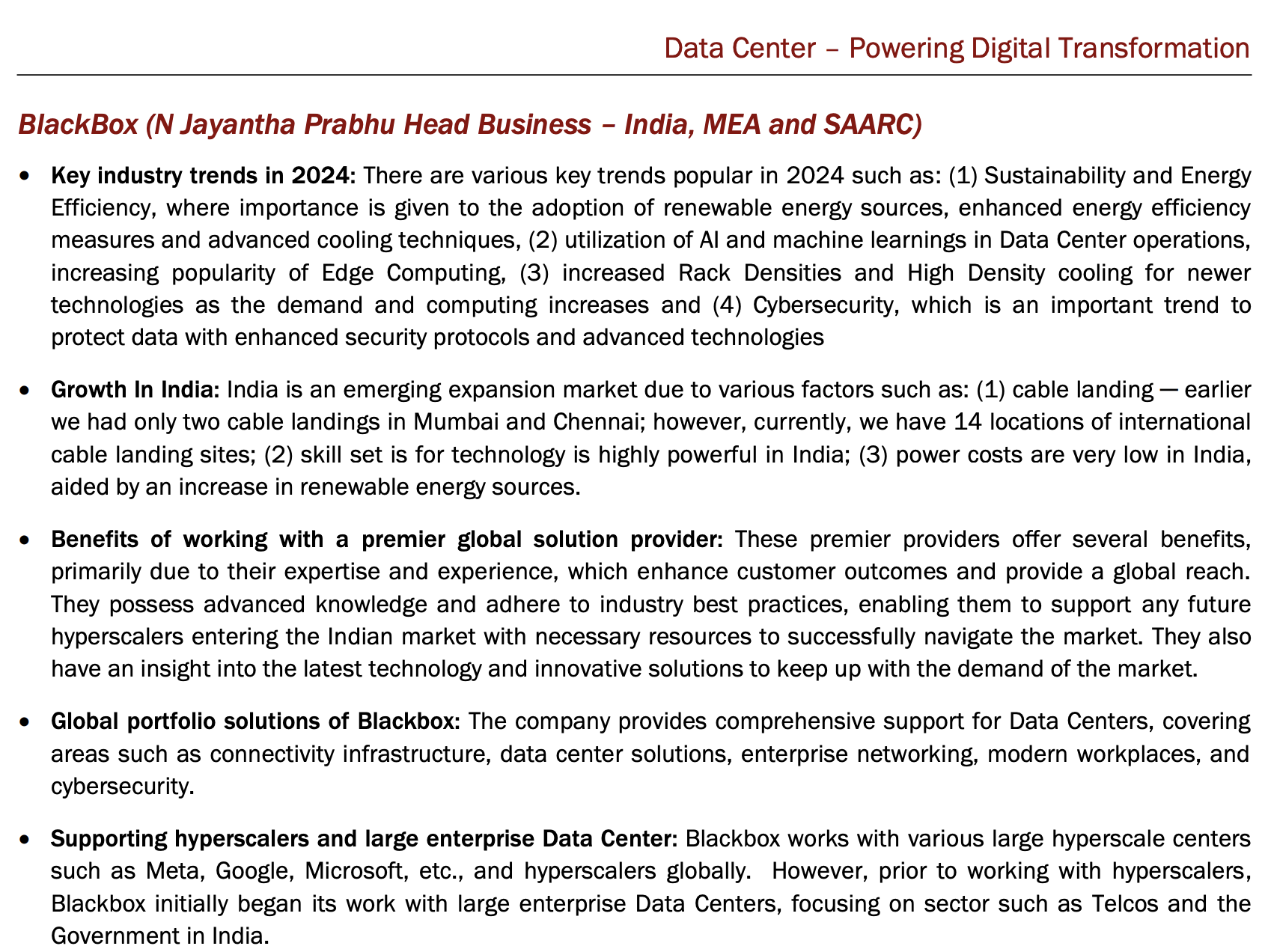

Black Box is a global digital infrastructure integrator offering connectivity and network

solutions, data center solutions, modern workplace and cyber security solutions and technology products to businesses globally across 35 countries in North & South America, Europe, Middle East, Africa, India and Asia Pacific regions with 85%+ business coming from North America.

According to Frost and Sullivan in calendar year 2023, Black Box is one of the leading solution integrators globally and in the US market with strong services offering in network integration, unified communications, collaborations, cyber security, digital infrastructure for connected buildings, data center solutions as well as AV solutions.

Black Box operates in two main verticals:

- Global Solutions Integration (GSI): In the GSI business, Black Box consults, designs, deploys, manages, and secures digital technology infrastructure for global customers. Their services include connected and smart campuses, digitalizing workplaces, data centers, ad networks, wireless and mobility solutions (including 5G and LTE), and cybersecurity. The GSI business contributed 86% of the total revenue in FY24.

- Technology Products Solutions (TPS): In the TPS business, Black Box sells and distributes technology infrastructure products to enhance customer experience through various channels such as online web platforms, distributors, integration partners, and value-added resellers. The TPS business contributed 14% of the total revenue in FY24.

Does Management Walk the Talk?

The company started hosting analyst concalls from Q1FY23. During this period, management guided for consistent 15-20% business growth and an expansion of gross and EBITDA margins, leveraging cost-cutting strategies by shifting work to a low-cost territory in India and improving per employee efficiency.

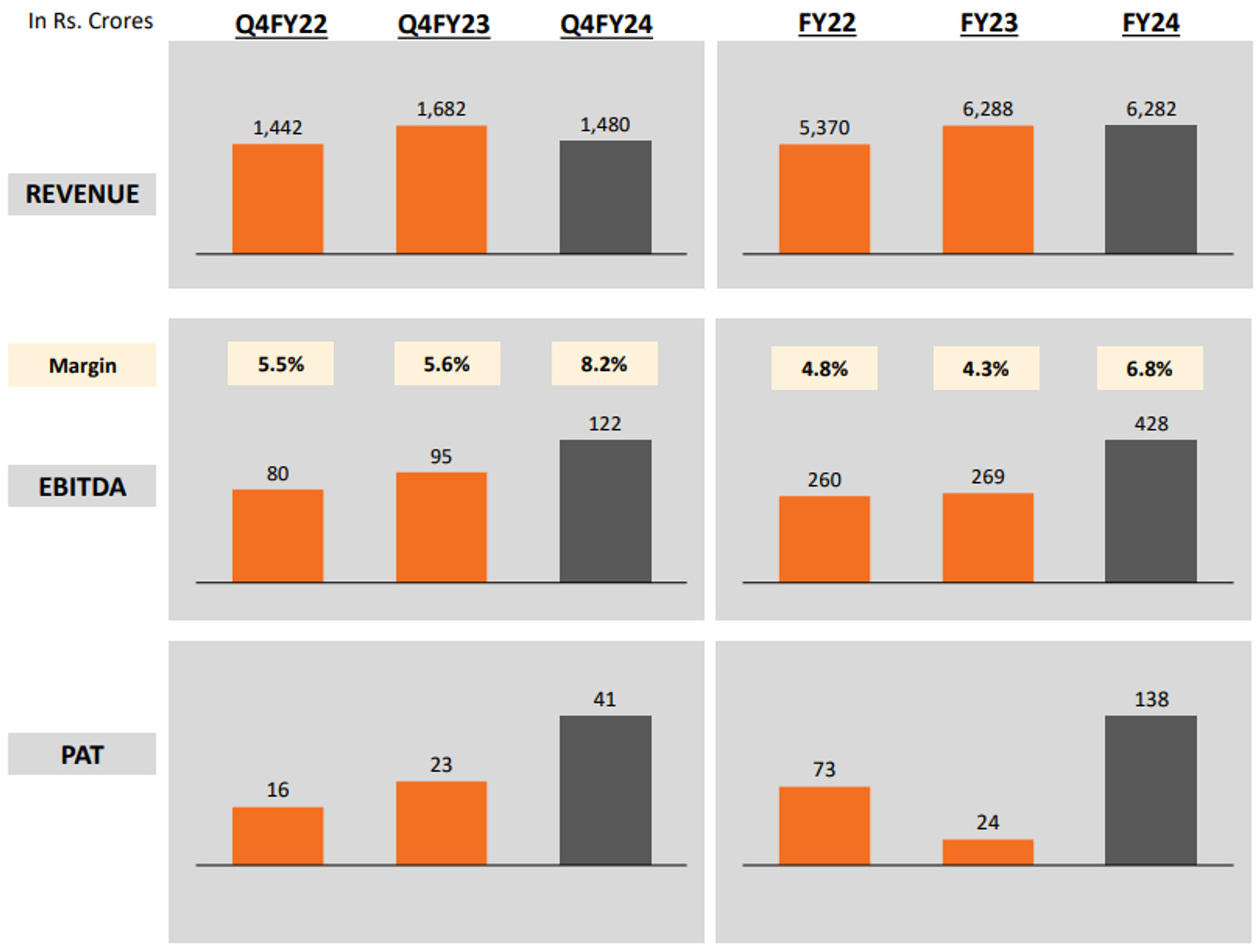

Throughout FY23, management consistently projected Rs. 6,000 crores in revenue and significant margin improvements in every concall.

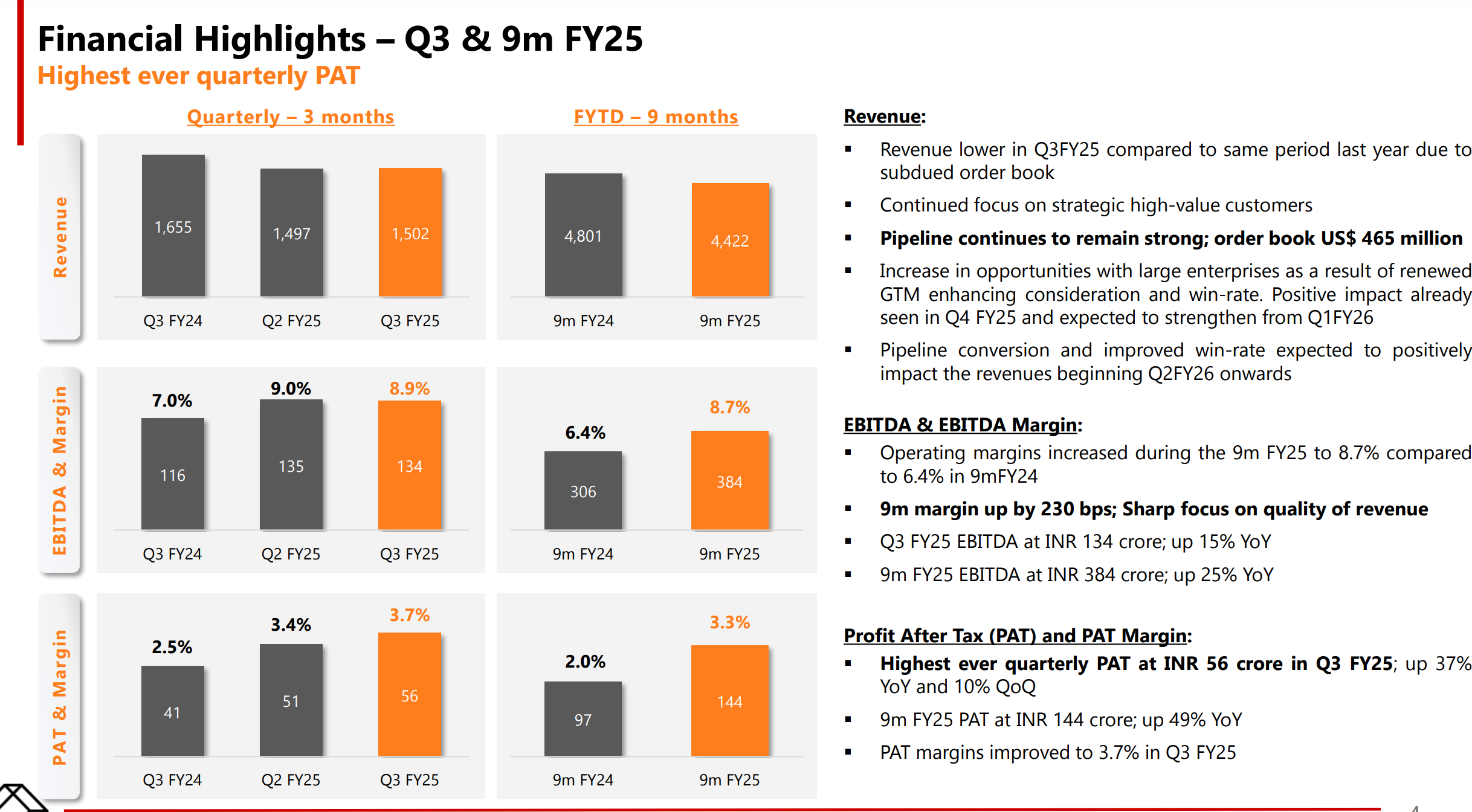

Black Box delivered on its promises, recording revenue of Rs. 6,288 crores in FY23, representing a YoY growth of 17%. EBITDA margins improved from 3.9% in Q1FY23 to 5.6% in Q4FY23. The management successfully adhered to its guidance for FY23.

Source: Q4FY23 Investor Presentation

Management Guidance across FY24:

”As we grow from here our yield of margin is expected to get better progressively quarter after quarter. So, now the answer is we have more juice left. We would expect to go to 7%-8%-9%-10% operating margin progressively and there is enough to be done here. [Q1FY24]

On how the margins will increase - So, there are 3-4 factors. Number one of course growth itself is a factor. We expect to grow reasonably in mid double digits. So, when we grow, we expect certain of our fixed costs to get amortized in a better manner. Fixed costs are not linear in nature so therefore it wouldn’t go. So, that’s one. The second of course we’re expecting our global delivery model to mature better as we move forward. And that comes at a slightly lower cost for us, so therefore better margin. As we scale up from here, we expect some efficiency with respect to our procurement strategy as well which will allow us to get some traction on that. And as we build scale from there, we are still in the process of working through, implementing and focusing on our service now and ERP systems, allowing us to serve our back office in a more robust manner from offshore. So, a mix of growth, a mix of ability to deliver from a global delivery model, our ability to procure better on scale and more productivity or more offshoring initiative that we have left to do over the next couple of quarters. A combination of these four gives us a good chance to start to move that 6 more towards 9 and double digit figure progressively over the next several quarters. [Q1FY24]

We are confident of our guidance pertaining to this year to EBITDA targets which is northwards of INR 400 crores to INR 450 crores. We are confident of our guidance give for PAT northwards of INR 140 to INR 170 crores range. [Q2FY24]

We remain optimistic about sustaining the profitability momentum. We are confident of remaining within our stated EBITDA and PAT guideline range for the year. [Q3FY24]

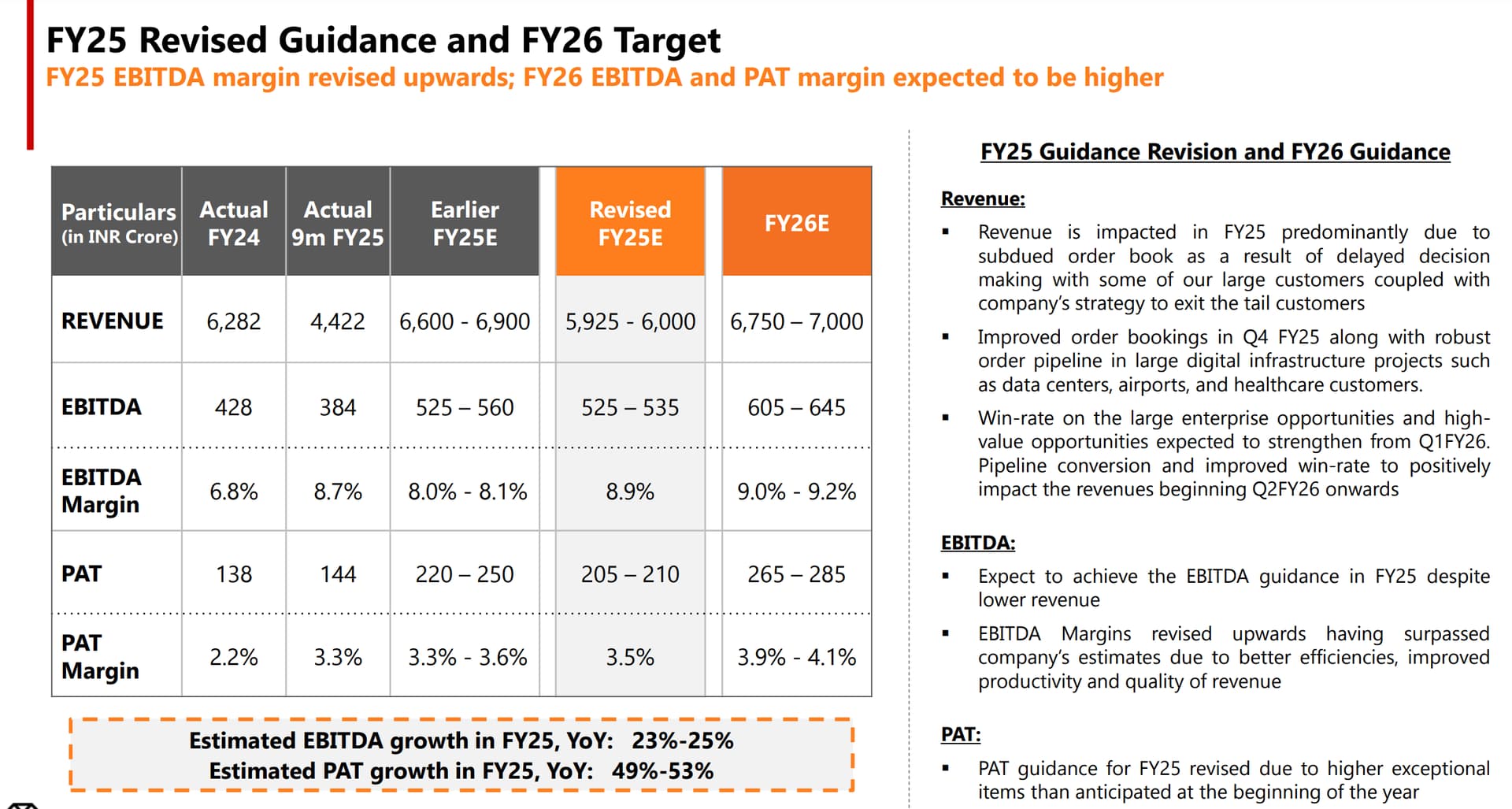

However, in FY24 Black Box faced headwinds from customers, leading to delays in execution and lackluster topline growth. Revenue for FY24 remained flat at Rs. 6,282 crores, falling short of the Rs. 7,000 crore guidance. Despite these challenges, management achieved its promise of enhanced gross and EBITDA margins. EBITDA increased by a robust 59% YoY to Rs. 428 crores, with EBITDA margins growing by 250 bps YoY to 6.8%. Although the PAT guidance for FY24 was missed slightly due to higher than anticipated finance costs, profit after tax increased by 5.8x YoY to Rs. 138 crores, just shy of the lower end of the guidance of Rs. 140 crores.

Source: Q4FY24 Investor Presentation

In conclusion, despite encountering some execution delays and missing the topline guidance, Black Box successfully delivered on margin improvements and demonstrated significant EBITDA growth, showcasing the effectiveness of their strategic initiatives.

Future of the business

Black Box’s transformation is driven by two key strategies. Firstly, the company is increasing its wallet share with large customers by letting go of smaller, less profitable ones, allowing it to better focus on and grow its order book with major clients. Secondly, it is further enhancing margins by negotiating better contracts and effectively managing costs through the utilization of low labor costs in India.

-

Growing order book -

Black Box has consistently expanded its order book over the years. Management remains optimistic about future growth, citing ongoing discussions with customers that are nearing $2 billion. Management is confident of achieving consistent double-digit growth, driven by the rapid adoption of new technologies like AI and 5G.

Year Order Backlog (US$ Mn) YoY Growth Mar 2021 87 Mar 2022 148 70% Mar 2023 209 41% Mar 2024 470 125%

-

Increasing wallet share of large customers -

Black Box is currently evaluating its customer base, focusing on yields and potential growth. The company aims to optimize profitability by either increasing prices for low-yield customers or exiting those relationships if the potential for growth is minimal. The company is gravitating towards high-value customers, which is expected to have a positive impact on margins, gross margins, and overall profitability.

Black Box is also working with other top cloud providers, aiming to elevate these relationships to the $100 million level. Black Box has achieved $100 million in revenue with its latest customer in just 24 months, compared to the 10 years it took with the first customer. This marks the company’s second customer generating over $100 million in revenue. This achievement highlights their increased efficiency in expanding high-value relationships.

Black Box is also working with other top cloud providers, aiming to elevate these relationships to the $100 million level. Black Box has achieved $100 million in revenue with its latest customer in just 24 months, compared to the 10 years it took with the first customer. This marks the company’s second customer generating over $100 million in revenue. This achievement highlights their increased efficiency in expanding high-value relationships.

- Continued improvement in margins -

Management remains bullish on operating margins, consistently guiding for continued improvement. Over the next 2-3 years, they project margins to increase from 7% to 9-10% on the back of double-digit revenue growth. This margin expansion is expected to drive a disproportionate increase in operating profit.

”I think we are over the next several quarters we intend to improve our operating margins and heading towards more towards 8%, 9% and 10% goals. I think that’s what our objectives are. For the next three years’ time, we do expect to be exiting upward of 9% closer to 10% and I think with scale we believe that is the possibility for sure whether we can do much better than that the time will tell, but for now, over the next two years to three years’ time, we expect to move from 6.5%. I think we expect to exit this year northwards of 7%-7.5% and therefore I think we expect over the next couple of years to be able to go to the 10%.” [Q2FY24]

“so we have 3-4 levers to focus on margins. So I think one of course is our ability to sell better, renegotiate our contracts when it comes up for renewal, which we are doing. The second of course, our ability now to have our Center of Excellence in India support us because it’s mature now we put the investment for the last 2 years time. So, we are able to get better productivity from our Center of Excellence in India that allows us to have better margin. Third, of course, our better relationship with our technology vendor partners allows us to negotiate better. And we are focused on ratio centricity across our various cost blocks, both from a cost of goods perspective, our G&A perspective. So therefore, a combination of selling and negotiating better contracts, ability to get better productivity from our Center of Excellence in Bangalore, India, which is now maturing, and also our ability to negotiate better terms with vendor partners and start focus on our G&A cost. A

combination of all this has helped us to expand our margin, as Deepak said, by over 250 basis points.

We expect that momentum to continue. Our goal is to reach about 10% operating margin, and we are clearly focused over the next couple of years to get there.” [Q4FY24]

Risks in the business

-

Subsidiary Risk: Black Box has 70+ subsidiaries, which could lead to undisclosed related party transactions, potentially increasing financial and compliance risks. Managing a large number of subsidiaries increases operational complexity and the potential for oversight issues, leading to inefficiencies and increased administrative costs.

-

Client Concentration Risk: 47% of revenue is derived from the top 10 clients, indicating heavy reliance on a few key customers. Any loss or reduction in business from these clients could significantly impact revenue and profitability.

-

Geography Concentration Risk: 77% of revenue is generated from North America, exposing the company to regional economic downturns, regulatory changes, and market saturation. Over-dependence on a single geography limits diversification and increases vulnerability to localized risks.

-

Strategic Shift Risks: The recent strategic focus on gaining wallet share of bigger clients may exacerbate client concentration risk, further tying the company’s fortunes to a few large clients. This strategy might limit growth opportunities with smaller clients and reduce market diversification.

Financials

Link to financials - Link

Valuation

Time and again, management has emphasized in concalls that their business represents non-discretionary spending for customers, ensuring strong pipeline visibility.

Conservatively assuming management can achieve a modest 15% topline growth for the next three years—reaching Rs. 9,500 crore (against the guidance of $2 billion)—and increase EBITDA margins to 9% (against the guidance of 10%), compared to Q4 EBITDA margins of 8.2% and full-year FY24 margins of 6.8%, EBITDA would increase to Rs. 855 crore, doubling from EBITDA of FY24.

| In Rs. Crore | FY24 | FY25e | FY26e | FY27e | FY27e - Mgmt Guidance |

|---|---|---|---|---|---|

| Revenue | 6,282 | 7,200 | 8,300 | 9,500 | 16,000 |

| Growth% | 15% | 15% | 15% | ||

| EBITDA | 428 | 576 | 705 | 855 | 3,200 |

| EBITDA Margin | 6.8% | 8% | 8.5% | 9% | 10% |

| Growth% | 35% | 23% | 21% |

As of 3 July, 2024, Black Box has a market cap of Rs. 6,300 crore and an enterprise value of Rs. 6,474 crore. It is currently trading at 15x trailing EBITDA and less than 7.5x FY27e EBITDA. (This is after the stock price is up 45% in last one week, without any news!)

These projections are relatively conservative and present an upside potential.

If management achieves its guidance of $2 billion (~Rs. 16,000 crore) in revenue and 10% EBITDA margins, the stock’s performance could be extraordinary.

Black Box could be an ideal investment, especially with the anticipated decline in US interest rates, which is expected to trigger a new investment cycle among US corporates.

Disc - holding