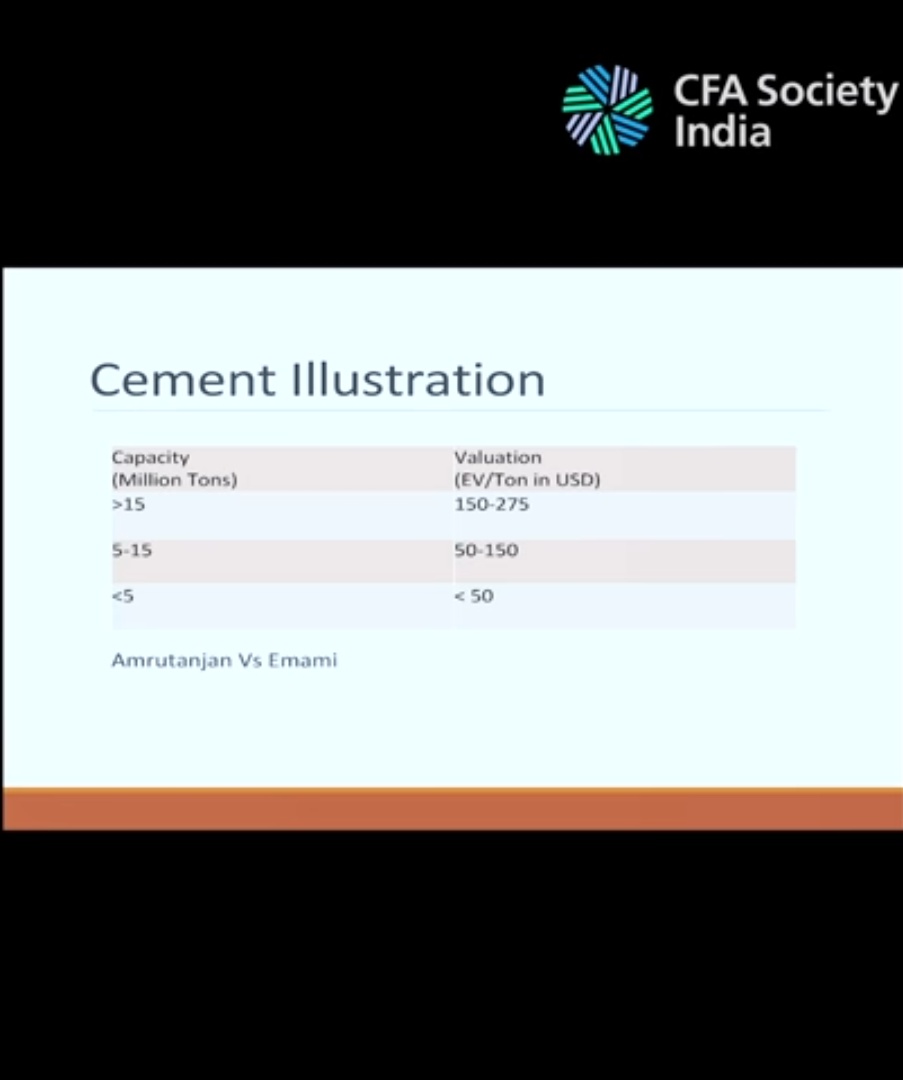

In his speech about his learnings in the stock market, Jatin Khemani mentioned that the market rates cement companies based on their capacity.

I checked the current valuations in terms of EV/EBITDA instead of EV/Ton to keep things simple.

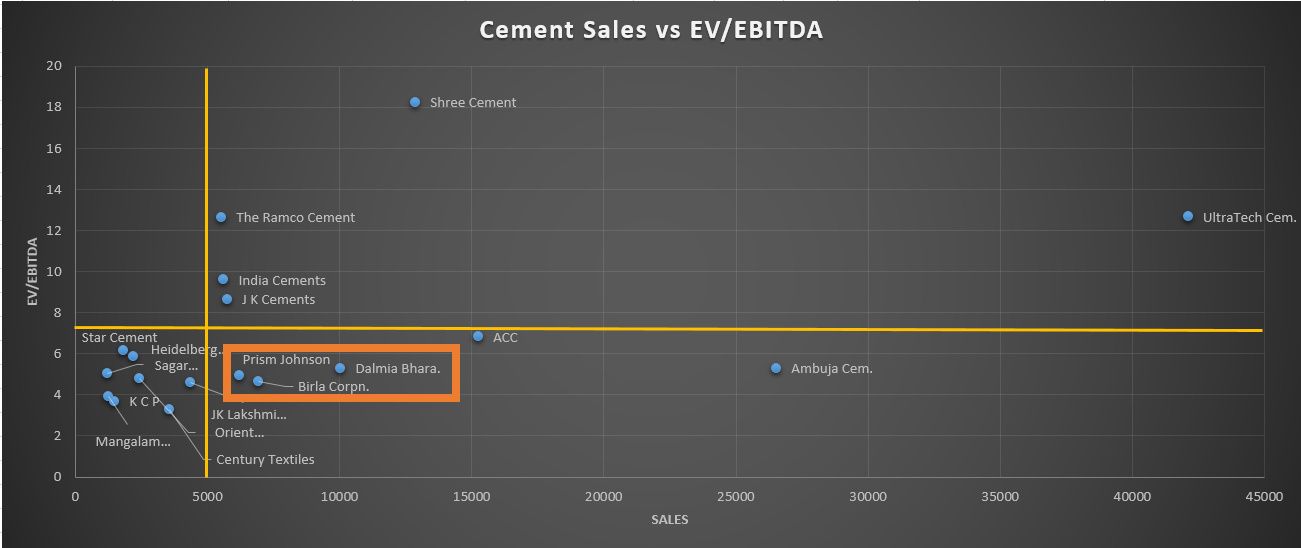

So the divide starts at 5000 Cr Sales. (5000 Cr / Realisation 5000 Rs per Ton) ~ 10 MT capacity.

The outliers are Prism, Birla, Dalmia, ACC and Ambuja. Prism has single digit Op Margin and huge debt. ACC and Ambuja have merger issues. The odd man out are Birla and Dalmia.

JK Cement, Ramco and even India Cements are trading at double the EV/EBITDA of Birla despite having lower Sales. By FY21 end, Birla will add 5.2 MT capacity. Re-rating has to happen?

Possible reasons for low pricing

- Debt: Birla’s Net Debt is 3500 Crores = 3x NOPAT

- Low PAT: Star Cement with 1/4th of Birla’s Sales had PAT of 300 Cr while Birla PAT was 250 Cr for FY19. Birla PAT increased to 500 Cr in FY20 aided by cost reduction. Still low because of Interest cost!

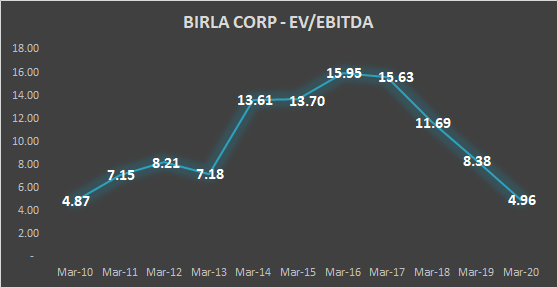

Looking at Birla’s historical EV/EBITDA, it is trading at the lowest level in the last 10 years!

10 Yr average is 10x, trading at 5x now.

A big mid-cap is trading at small-cap levels.

Disc - Small tracking position. Will add more.