Thanks @ankitgupta and others for contributing to the post.

Have been trying to study the business and industry for the past few days and here are some of the things I noted:

-

Limestone shouldn’t be a problem for the company for the next 10-15 years or so (I checked the notes to previous Annual Reports and the amortization for the mining right is about 5-7% every year)

-

FY20 has been a good year for the industry due to increased demand and favorable factors like lower price of pet coke and freight cost etc and many players’ key metrics like EBITDA/ton have seen improvements, and is not specific to Birla Corp.

-

New management seems to be doing a really good job-working to improve efficiency in logistics, installation of solar plants, securing coal mines, launching new products (wall putty and water repellent premium cement) building railway siding at Kundanganj plant etc.

Few of the things which I’m unable to understand (and I would be really thankful if someone can help me out here ![]() )

)

-

Where exactly is growth going to come from for the company? (Although the company plans to increase it’s production capacity by 33%, we don’t know if the demand will increase)

Since there is no ‘new market’ and price can only be increased marginally (in the retail segment), the company will have to increase its market share and dislodge competition- my question here is, is the branding/consumer trust for Birla Cement so strong that consumers will not prefer other companies’ cement? And that other players in the retail segment can’t beat Birla’s competitive advantage? -

Since forecasting demand is pretty tough in cement industry (now, the added covid impact just makes it more tough), it feels like the industry is a bit opaque in terms of judging quantitatively about- how many tons of cement can the company sell next year/what will be the % of realization etc and hence, further making guesses about the ‘potential’ of the company, valuation etc

Is there any way to go about this? -

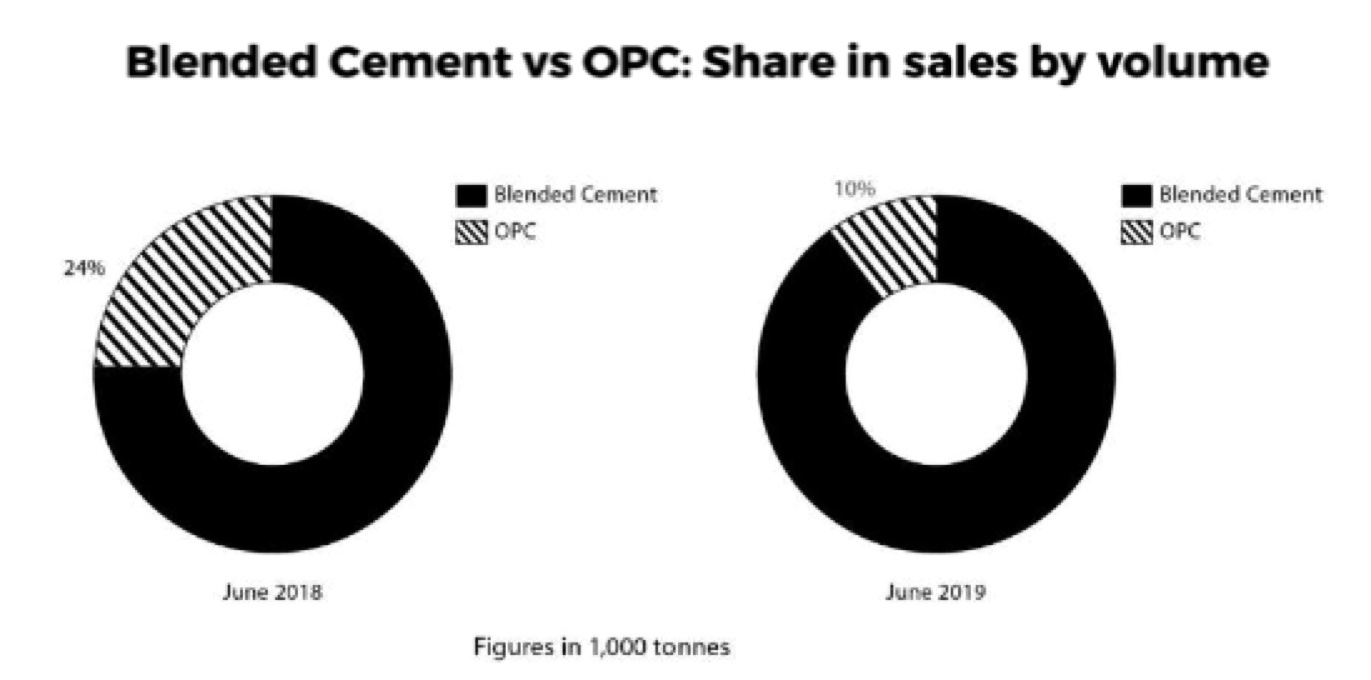

Can anyone explain a bit about ‘Blended Cement’? (Is it a kind of OPC? Does it have higher price? Does it create a difference in demand between trade and non-trade segments?)

(Source: Q1FY20 Report) -

Is high debt the main reason why the company is a bit discounted by Mr. Market? (on metrics such as EV/EBITDA)

Looking forward to some guidance for going ahead with my analysis ![]()