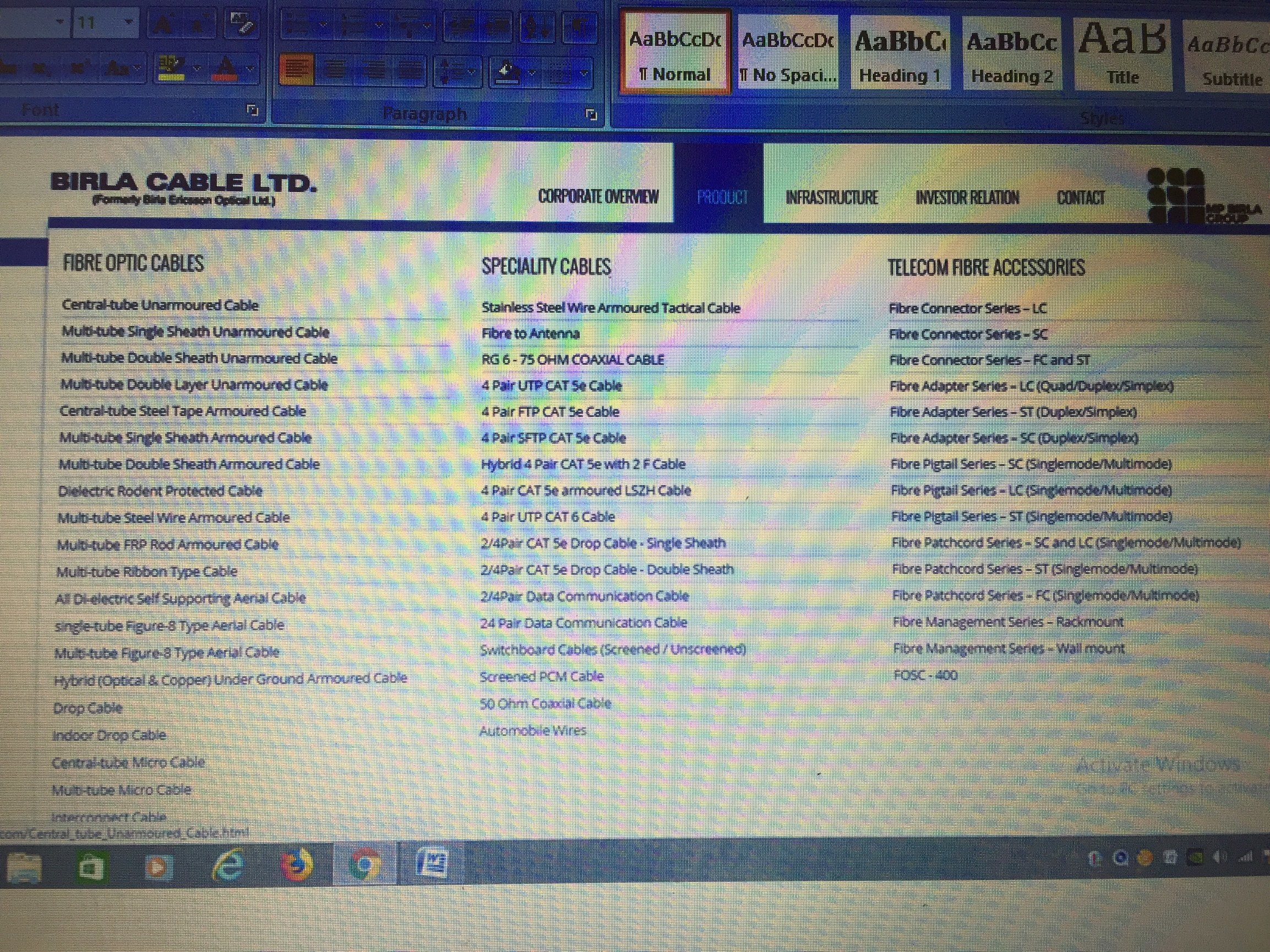

Birla Ericsson Optical Ltd.

http://www.screener.in/company/?q=500060

Market Cap: 188 Crores

Last quarter sales was 97 Cr and a net profit of 8 Cr

Birla Ericsson Optical Ltd (BEOL), is an ISO-certified company under the MP Birla Group of Industries . The company is into design and production of fibre optic cables in technical and financial collaboration with Ericsson Cables AB, Sweden.

Optical Fibre Cable (OFC) is mainly used in long distance networks and generally forms the backbone of all telecom networks.

Theme of investment:

The company has reported good numbers for past 3 quarters and looks like a good case for turn-around story to unfold.

The key drivers for OFC deployment in India include the growing demand for broadband services, proliferation of next-generation broadband technologies, increasing OFC deployments in last-mile connectivity (FTTx), and availability of low-cost smartphones and tablet PCs.The deployment of fourth-generation wireless networks in India is likely to propel growth of OFC in the Indian subcontinent. In addition, several state-level e-governance projects funded by the central government and state govts will include OFC networks as a key component.

Main players in the industry:

In the order of their size:

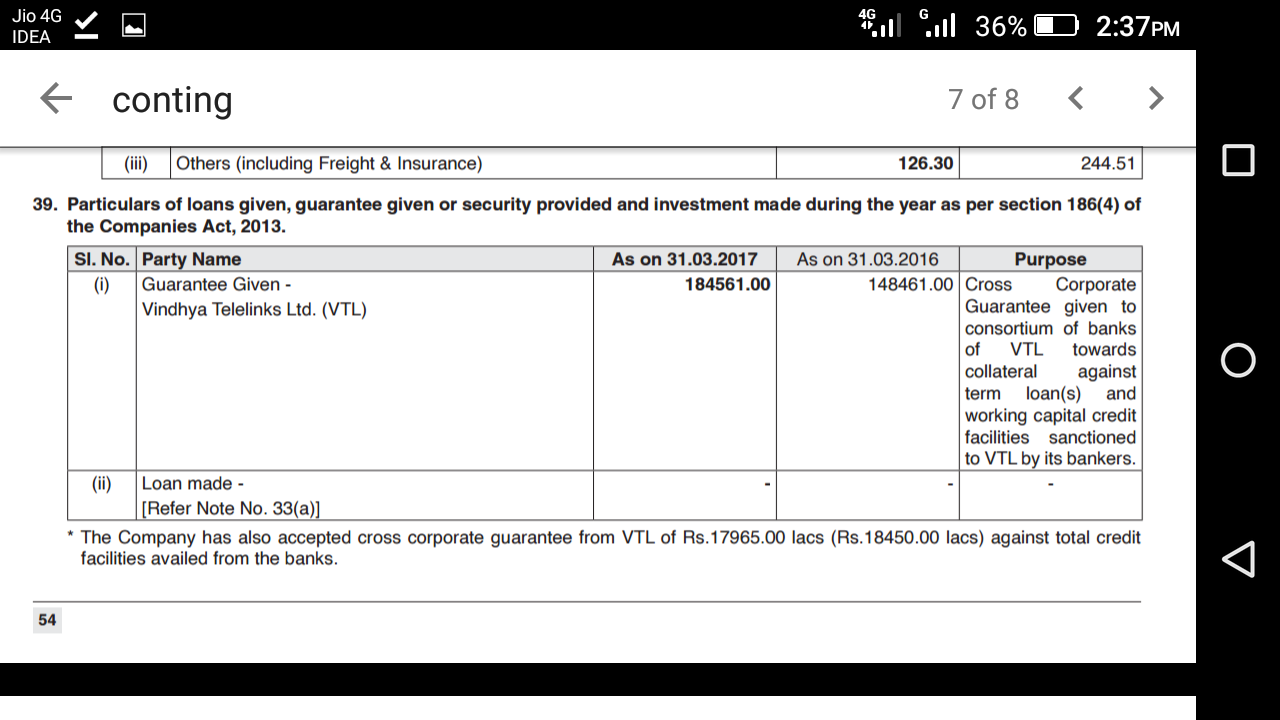

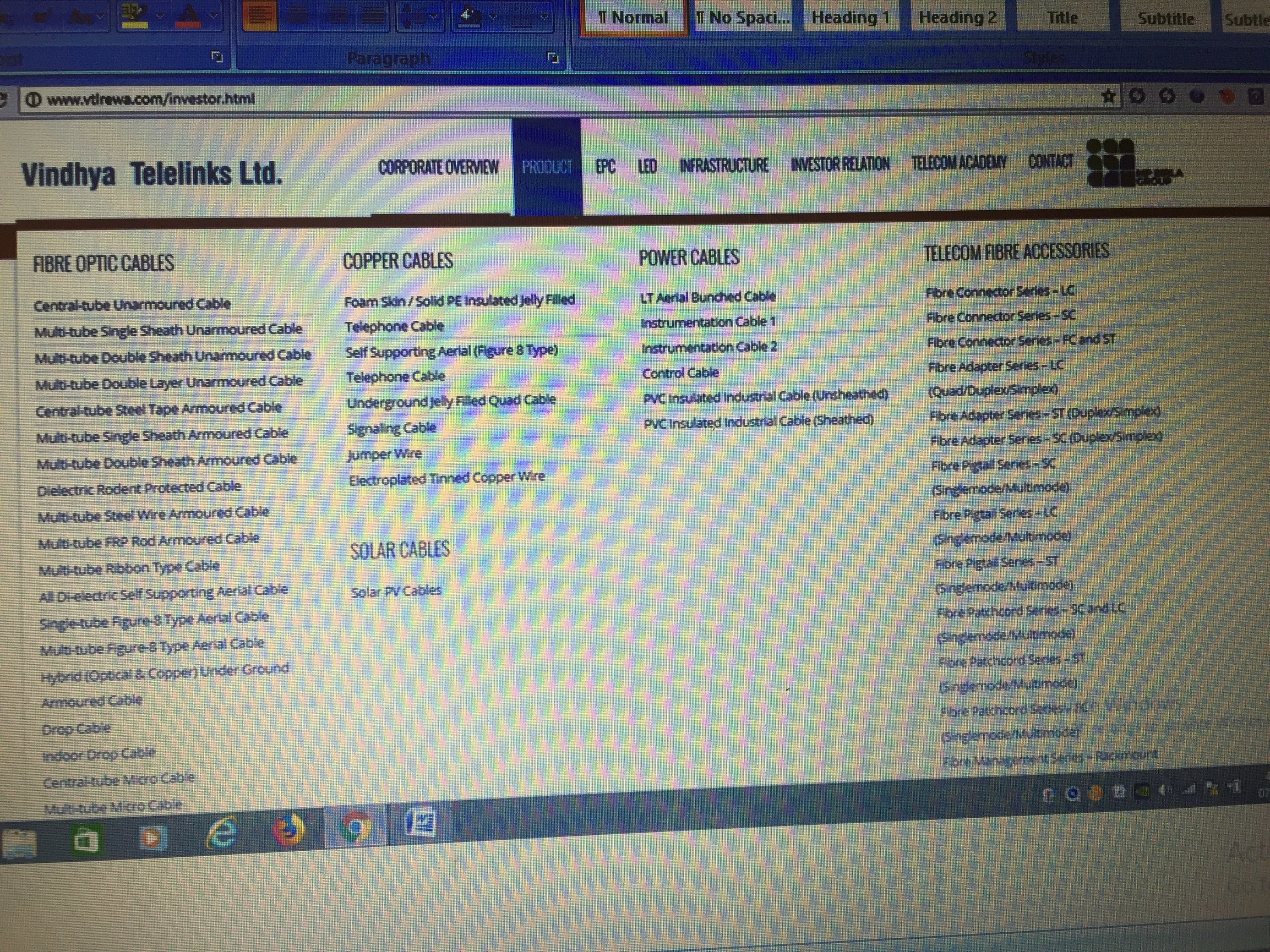

Sterlite Technologies,Finolex Cables,Vindhya Telelinks Limited (also part of the MPBirla Group)Aksh Optifibre,Shilpi Cable,Birla Ericsson Optical Limited

Finolex and Shilpi are already extensively discussed in the forum.

Sterlite is the biggest player but sits on a debt of 2770 Crores!

BE has installed capacity for producing 36414 Optical Fibre Telecommunication Cable Km. per annum . BE has facilities to manufacture all the internationally accepted cable constructions.

BE also has the capability to produce specialty cables for use in medical equipment, computers and Local Area Networks, Cable TV Network or any other type of special fibre optic cables based on customer specifications.

They export OpticalFibre Cables to Sri Lanka, Middle East, European countries and other African countries. Exports have been consistently increasing.

Key Risks:

- This is more of a turn-around story. Company has in the past failed to provide consistent, quality earnings.

- Being a small company, there is very little information out in the open

- The Competition is getting fierce and there are possibilities of emergence of certain integrated overseas players

Disclosure: Invested in Birla Ericsson Optical (from lower leves) and hence my views may be biased

Information sourced from annual reports/company website/other open forums