Performance in H2 FY20 to be even stronger, driven by new launches and availability of new capacities, helping both revenue growth as well as margin profile Full impact of new launches and additional capacities should reflect in FY21 P&L with substantial full year growth projected over FY20E FY22 expected to build upon FY21 with expected launches of Insulin Aspart and Bevacizumab

Exciting time for Biocon and shareholders. Share price has rallied 40% since the lows in October. Growth in the next 6 months will come from peg-filgrastim and trastuzumab sales in the US. Also expecting growth from Canadian and Australian markets.

Hopefully glargine will be approved in the US before March 2020.

Discl - continuing to accumulate, 28% of my portfolio

I have been invested in the company since 2015 and currently it forms about 25% of my overall portfolio. I am unable to understand why company is lacking in growing its business when compared to peers like NATCO, ALEMBIC. Any input here?

True North has acquired about 3 per cent of Biocon Biologics India Ltd (BBIL), a wholly owned subsidiary of Biocon, for $100 million, valuing the unlisted arm at $3-3.5 billion (Rs 25,000 crore)

The same investor has earlier bought stake in earlier opportunities with Kiran Shah, and seems to have a good relationship. I would want to have another investor take stake at similar valuation for additional comfort.

In the era of Ubers/Wework/ flipkart/Zomato/ Swiggy…where profit is far fetched…valuations are 15X to 20X type or even higher.( X being sales)…we see marquee investor lining up…Here we have a proven biz and profit making…mkt potential is huge globally…start itself is conservative…

It is likely that relationships leverage is at play( earlier in biocon listing, but why set a low benchmark of 10X type( 2500 cr annual conservative est for current FY).

I think the fall had more to do with the fear that, post biologics listing, biocon will be reduced to a holding company with the associated 60 to 70 % holding company discount. Moreover, instead of giving proportional shares in biocon biologics, KMS will short change the minority shareholders of biocon by giving only a preferential allotment (re syngene), which is peanuts compared to the risk and uncertainity that the investors faced in last few years with multiple CRLs, missed timelines, FDA 483s and GMP issues.One silver lining is, by the time biocon biologics comes out with IPO ( 12 to 18 months), glargine, bevacizumab, rh insulin and aspart story in US would have played out taking the biocon share price by 2 to 5x, giving a good window for risk averse to cash out. I will most likely continue to hold biocon, hoping that the best scenario happens, where biocon share holders will get proportional shares in biocon biologics.

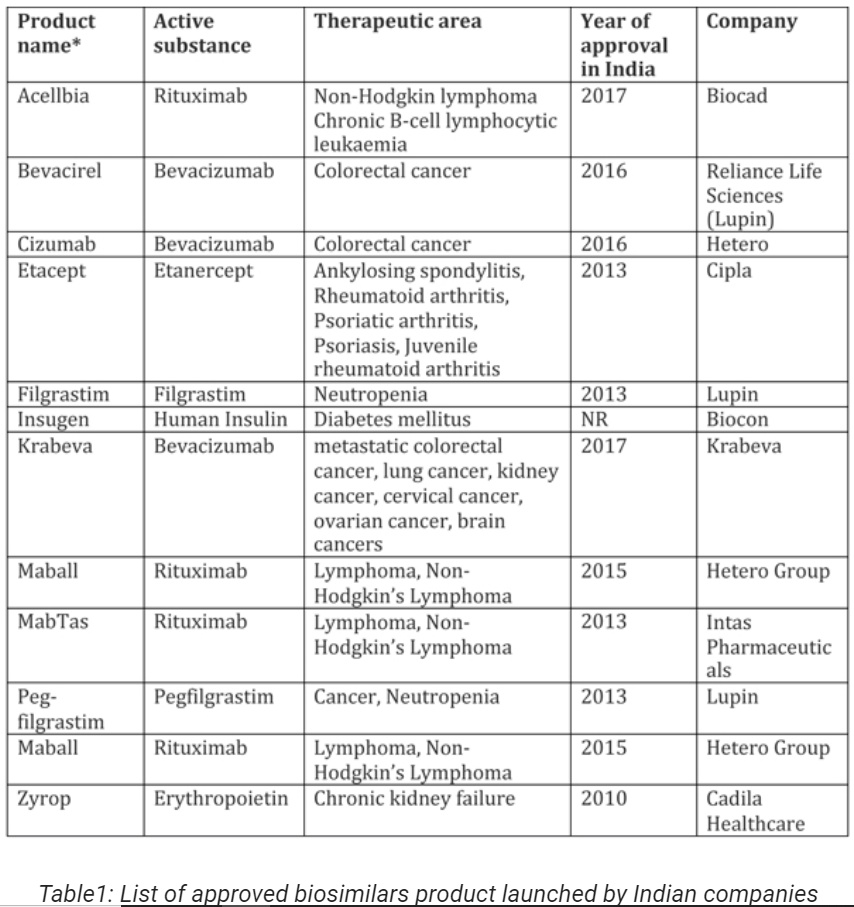

Biocon’s specialty seems to be in targeting the US and other developed markets, since it seems to me there are several biosimilar pipelines in India. This article counts more than 10 such companies.

The moat here seems to be due to two things and 70% derived from point #1 below:

The inability/non-interest of most pharma (not considering non-Indian MNC) to launch such products in developed markets.

The inability/non-interest of most pharma (not considering non-Indian MNC) to make such product varieties.

Is this a sustainable moat?

The article in the post above gives a 3-5 year boom time-period and then steady performance for a longer time-period.

drmithunraj in his post also indicates the same thing, predicting good part of the boom to play out within 2 years.

I would agree with the expert judgement.

Biocon Malaysian Insulin facility gets only 3 Form 483 observations.

Disc: tracking, no holdings, was invested previously but consolidated portfolio/reduced holdings, does not fit my mental pattern/investment style, yet.

Biosimilars sunrise is about to happen.

Continue holding - do keep an eye on the listing of their Biosimilars arm (due next year). It shouldnt happen that value from Biocon gets migrated to the Biosimilars entity.

Biocon has been a consistent performer. Since 2015 (when the price was in the range of 75), it has given more than 30% cagr. That’s pretty decent in my opinion

@NauticalTwilight@rks00

What is the biocons addressable market size w.r.t their products in biosimilars? small molecules?

How much of this they would be able to capture?

Coming to biologics IPO- I believe the process will be same as syngene IPO. As per my understanding market was largely positive towards biocon during syngene IPO. It might be due to (valuable)biosimilar entity in Biocon.

Now, Incase of Biosimilars IPO - Can we expect similar response towards biocon? or will it be treated as a holding company? Do you expect good potential in left over entities?

Please provide your thoughts