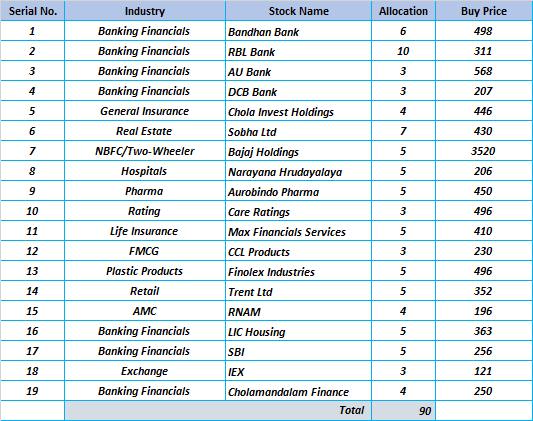

The pf looks heavily concentrated on banking/ financials/ Insurance. This may adversely impact returns. However if you have deep knowledge of the sector, and have high risk appetite then you may have an edge. Intriguing to see despite concentration on banking/ financials, there’s no HDFC bank. Any particular reason? Professor Bakshi shared his presentation on a similar subject, which is worth going through. It can be accessed here https://fundooprofessor.wordpress.com/2019/10/13/non-ergodicity/ . There’s is also a very nice thread on capital allocation frame work, which you might want to go through. Towards a Capital Allocation Framework!

Would had been better with 10-15 max total no of stocks . Diversification is good but excess is not good.

Lacks sector leaders except bandhan Sobha. Retail should always have sector leaders.

Hdfc bank Bajaj finance can be trimmed but sold off completed may be a mistake.

Care and Max interesting bet.

Pf lacks focus I.e. trying to bet on every sector like MF. Sorry to be critical but it’s my view and I have right to go wrong.

Discloser. I have hdfc bank Bajaj finance Bandhan Trent in pf

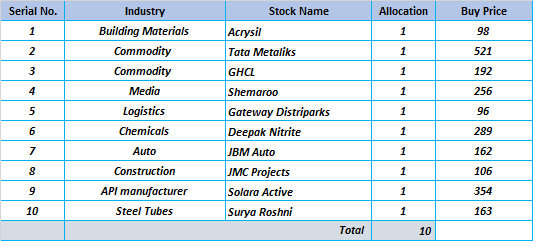

I exited to enter Zee entertainment which also has OTT and valuation has corrected a lot. I will wait for the promoter overhang to get cleared which I think would eventually be done as lenders might exit and sell most of the promoter stake which is pledged to recover dues.

I also dont like shemaroo management entering into food business which is already very competitive. OTT and content business in itself is so huge where many players had made it very large in the world. Somehow management wants to enter in some business where they will have competition from even unorganised sector.

Hello Bimlab,

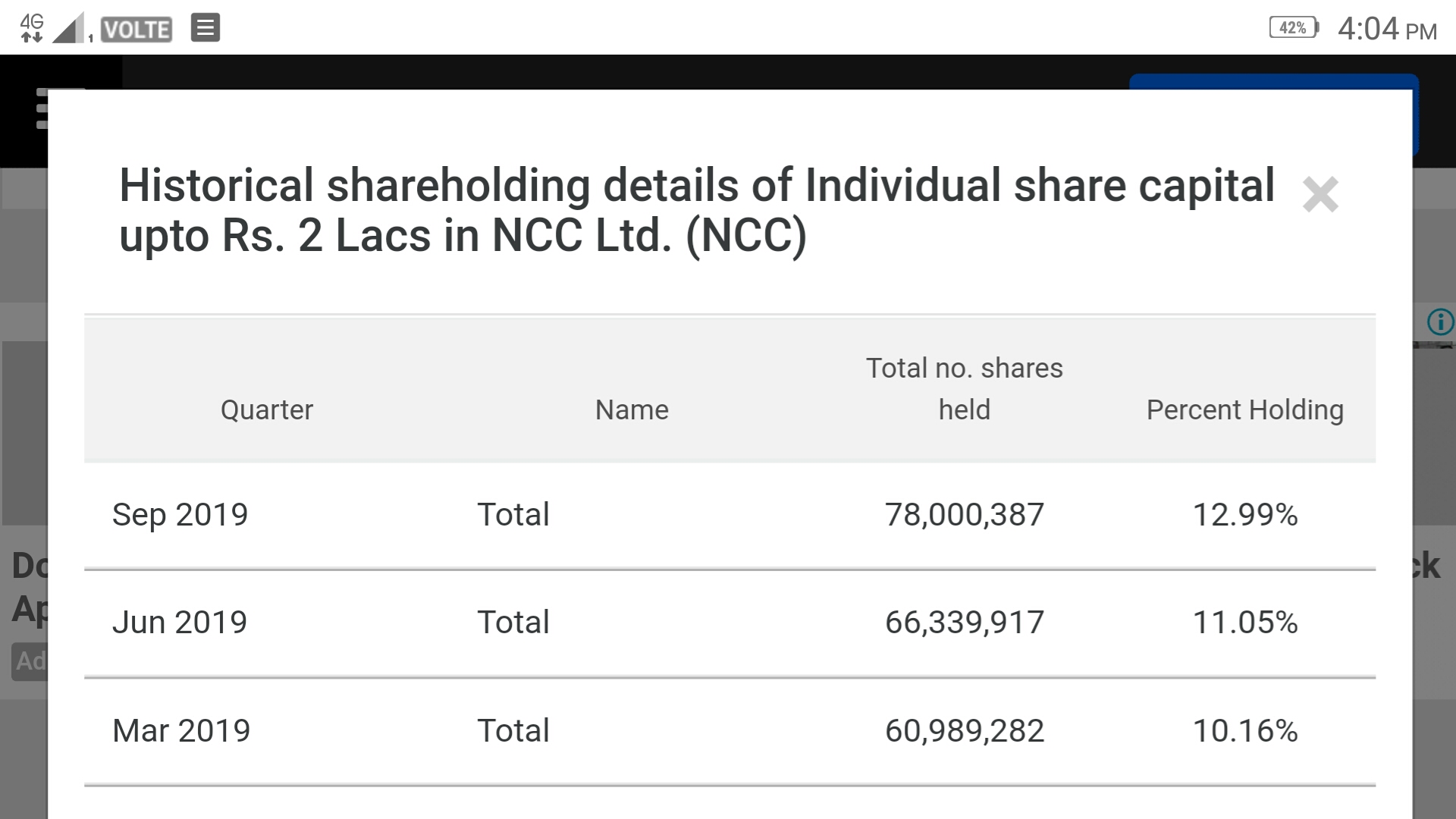

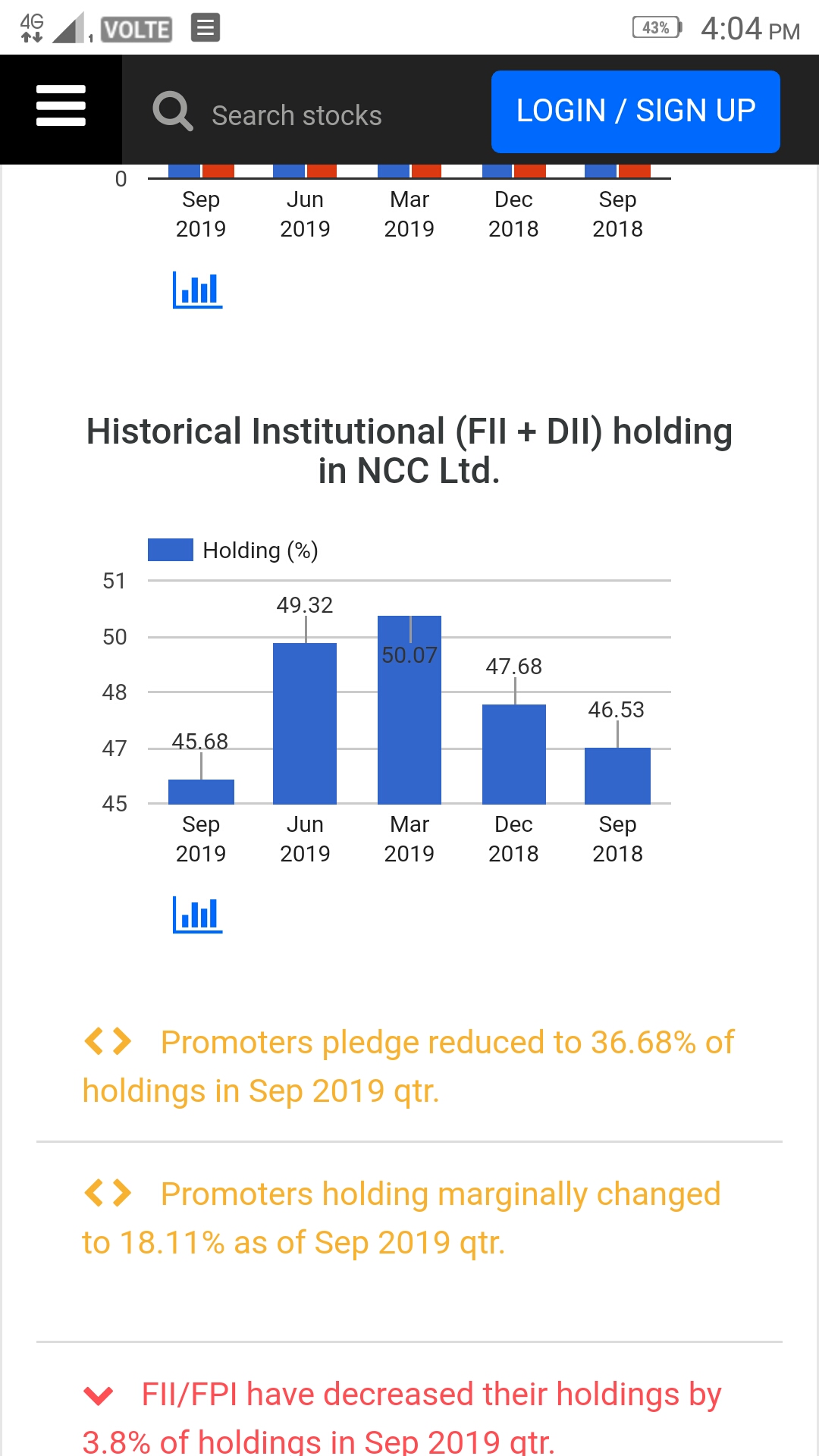

The shareholding of retail shareholders has increased substantially and fii+dii decreased in last three quarters. Doesn’t that mean we are betting against the big guys and with the novices.