BigBloc Construction Limited, wholly owned subsidiary - Bigbloc Building Elements Private Limited started a trial run of machineries for Greenfield Project of AAC Blocks at Wada in Palghar, Maharashtra. Commercial production from the plant is expected to commence by end of March 2023. At full capacity, Wada plant is expected to generate revenues of Rs. 200 crore per year.

Total capex for the Wada project is estimated to be around Rs 65 crore for setting up the 5 lakh cubic meter (cbm) per annum plant at Wada, Maharashtra for manufacturing AAC blocks. Company has invested Rs 48 crore in the project so far for the commercial operations of Phase I. Company is eligible for 60% subsidy from the state government for the project and expects to generate 1 lakh units of carbon credits per annum from the Wada project. (i.e One carbon credit represents 1 tonne of CO2e that an organization is permitted to emit).

Post completion of the expansion, company’s total capacities will increase to 13.75 lakh cbm per annum making it the largest manufacturer of AAC block in the country. Company also expects to generate around 2.5 to 3 lakh units of carbon credit every year post the expansion.

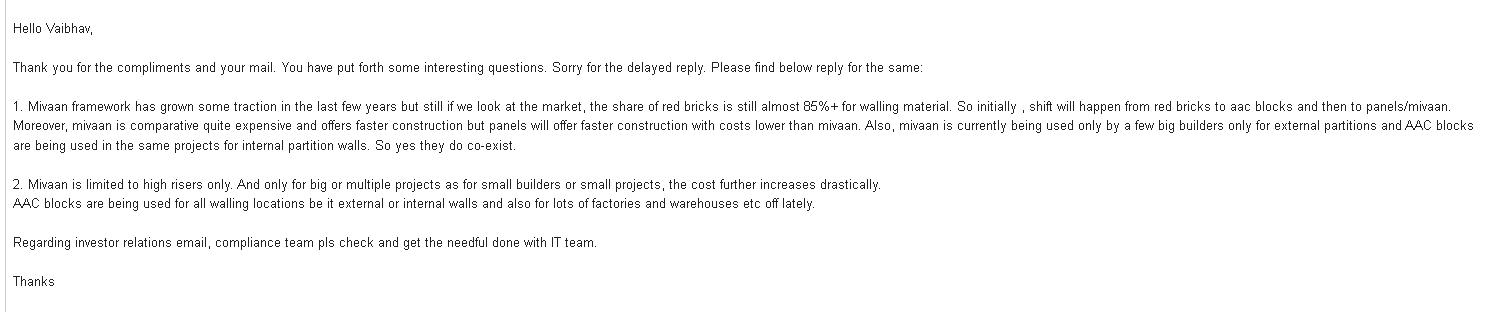

Can anyone close to construction market pls give their 2 cents on - future of AAC blocks in light of Mivan picking up big time?

As per my research, most high rise builders in NCR, Pune, Blr etc. are using Mivan technology for construction. I am unsure if both Mivan and AAC blocks can coexist - for instance, AAC blocks for internal walls and Mivan for external framework.

The aluminum framework used in Mivan is expensive but due to faster (50%) construction times, leads to cheaper and quicker large scale projects. On the other side, unsure if its a cost-effective option for smaller/residential housing or smaller apartments?

Did some scuttlebutt too: a retired chief engineer in rajasthan govt said that AAC blocks are being used for government enclosures too and they are mandated due to lower cost and being environment friendly.

Looks like AAC blocks has a future. On top of it management is talking about getting into more green materials in future.

I have seen recently many investors getting Gung-Ho on this company but I somewhat don’t feel comfortable with this company due to multiple reasons.

1- Reasons of Bad Q4 -due to Holi vacation- shortage of Labour in both construction site and plant.

In Q3 concal, they mentioned → there was a volume reduction in q3 due to extended monsoon.

I personally could not digest these reasons. These all reasons are quite insane to be given and how can a investor buy those reasons without thinking twice? All thanks to the price movement in stock which actually give them the confirmation bias make them bullish unnecessarily thinking it’s all good.

Holi was there in Q4 last year also. Then why such issue this year? (As mentioned above by another investor)

2- Percentage increase of Sales- 14.20% and 21.57% in March 2023 and March 2024 VS percentage Increase in Receivables- 18.35% and 67.90% in March 2023 and March 2024 respectively. Parallelly Percentage increase in Inventory- 75.20% and 46.19% in March 2023 and March 2024 respectively which makes me suspicious about their sales numbers.

3- Their EBITDA margins are almost double of their competitors even from the largest player in the industry which again makes me more suspicious without any strong justification for the same that how are they able to operate on such a high margins catering to B2B clients that too in a Real Estate sector.

4- Also CFO/Ebitda is 56% and 35% in March 2023 and March 2024 respectively which is considerably low, which again is alarming.

5- If their ROCE is north of 30% then why their is still rise in Net Debt I know one will argue that they are in expansion phase even considering that the debt shouldn’t increase if the ROCE is north of 30% there are companies who have executed the expansion without increasing the Debt to this level considering their ROCE was also in line with this company.

I know I’m making this contra perception and many won’t agree to this but feel free to share your opinion and kindly correct me if I’m wrong somewhere in my analysis.

There are many regional players but HIL ltd is one of the leading listed manufacturer of AAC blocks that too with Pan India player vs BigBloc who is more regional dominated.

On Bigbloc I have a concern:- they have debt on their books (1.37 debt to equity as of March 2024).

When I read the Crisil ratings report, it says “non-cooperation by the issuer”.the report is from August 2023. The earlier one also says the same.

Why would they not be cooperating with Crisil? I mean a good report from a ratings agency should be a good sign especially to give lenders some comfort.