Bharti Hexacom Limited

The Issue:

• GOI will sell 7.5cr shares (representing 15% of total share capital) at Rs570/share in IPO.

• Issue size: 4,275cr

Shareholding post IPO:

• Bharti Airtel Limited: 70%

• GOI: 15%

• Public: 15%

Valuation:

• IPO price: 570

• Market Cap at IPO: 28,500cr

• Net Debt: 7,500cr (F24 end)

• EV: 36,000cr

• EBIDTA (F24): ~3,600cr; EV/EBIDTA: ~10x

About Bharti Hexacom Limited:

• BHL is a communications solutions provider offering consumer mobile services, fixed-line telephone and broadband services to customers in the Rajasthan and the North East telecommunication circles in India, which comprises the states of Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland and Tripura.

• BHL offers their services under the brand ‘Airtel’.

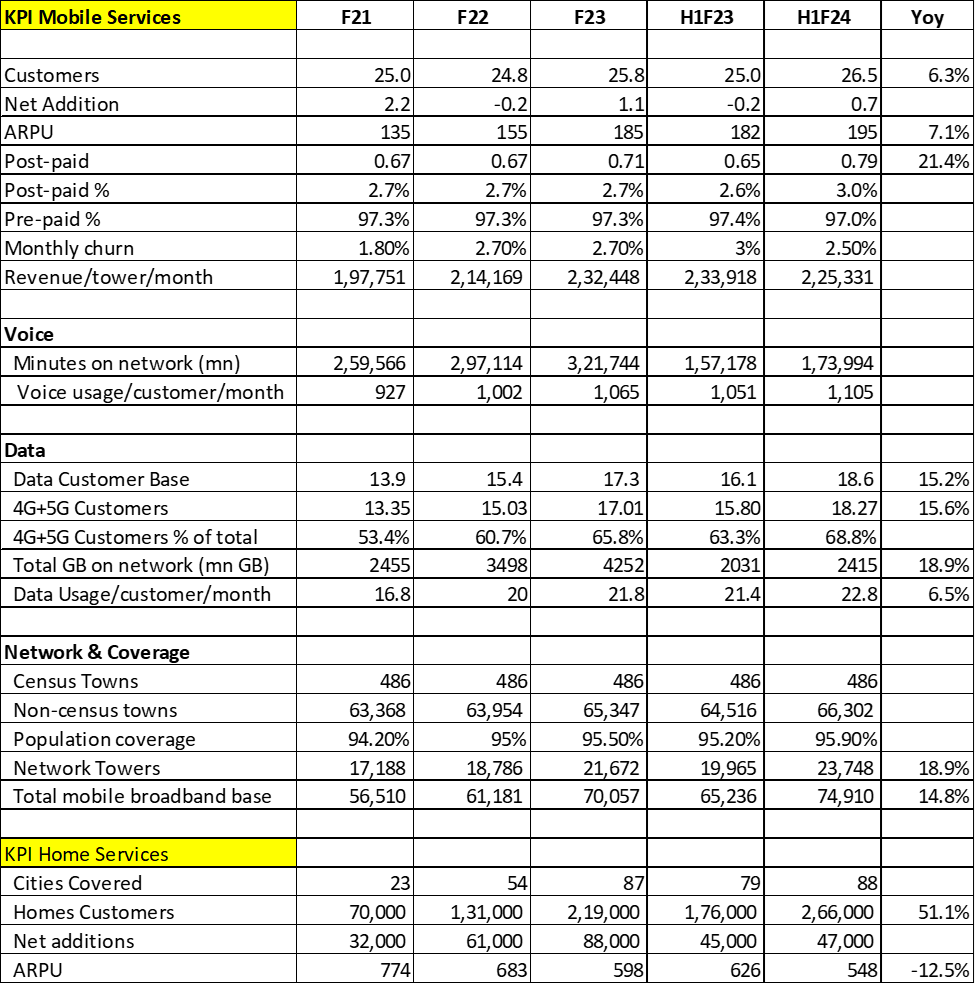

• BHL has ~27mn mobile customers as of March 2024 in Rajasthan and North East circles.

• Broadband is very small with total subscriber base of less than 3L connections in these regions. (Broadband contributes to ~2.5% of total revenue in F24)

• Revenue split: 80% Rajasthan + 20% North East.

Net Debt:

• Net Debt of approximately 7,500cr as of March 2024.

• Net external bank debt as of March 2024 should be close to 1,500cr + lease obligation: 3,000cr + spectrum liabilities: 3,000cr.

ROCE better than Bharti Airtel & JIO:

• BHL is asset light model vs BAL as the broadband fibre assets and other infrastructure are not housed in BHL and they use BAL platform for other services as well.

• Corporate, sales, marketing, certain network infra, vendor negotiations happens at BAL level which BHL enjoys.

• All these add up to lower investments by BHL which enhances their ROCE profile.

• F24 ROCE profile: BHL: 16-17% > BAL 12-13% > JIO sub 10%.

BHL pays BAL for using its platform:

• BHL uses fiber, go-to-market strategy of BAL.

• BHL thus pays BAL for all these services at an arm’s length basis.

• The quantum of BHL outflow to BAL for use of Airtel brand is undisclosed.

• Do not see any negative in the above related party transaction since BHL is owned 70% by BAL.

Spectrum and AGR dues:

• BHL will start paying the spectrum and AGR dues from F26 like the rest of the players.

• H2F26: Outflow of ~400cr and 800cr from F27 to F31.

• This will be paid from internal accruals.

CAPEX:

• F24 CAPEX is elevated at ~2,000cr.

• It is expected to reduce from F25 onwards – similar commentary given for BAL as well.

• Potentially, CAPEX can be around 1,500cr p.a. from F25 onwards.

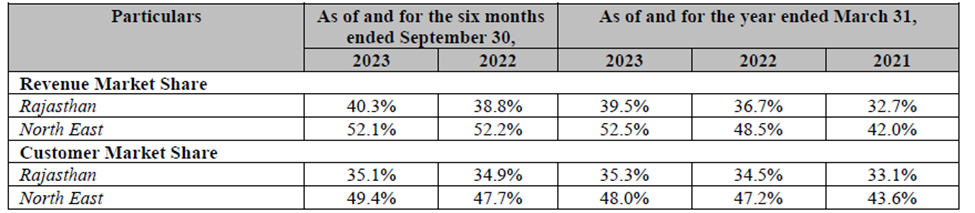

Revenue market share:

• BHL is number 2 in Rajasthan and the gap has narrowed in last 3 years with leader with ~40% RMS.

• BAL has market leadership in NE with ~52% RMS.

Synergy with Bharti Airtel:

• BHL derives significant synergies from relationship with Airtel and its affiliates, including through Indus Tower’s infrastructure, inter circle roaming arrangements, its national long distance network and corporate functional support.

• The relationship helps drive growth, optimize capital efficiency and maintain competitive advantage.

• BHL is able to obtain better terms from vendors and other third parties due to the scale of combined operations.

• They also derive operational efficiencies by centralizing and sharing certain key functions across our businesses such as finance, legal, information technology, strategy, procurement and human resources.

Strong network infrastructure:

• BHL relies on a robust network infrastructure with a mix of owned and leased assets.

• As of September 30, 2023, they had 23,748 network towers, of which they owned 5,005 towers.

• They have a spectrum portfolio with varied pool of mid band spectrum (1800/2100/2300 MHz bands), which has enabled to offer 5G Plus services on the widely chosen non-standalone network architecture and at a low cost of ownership.

• This has enabled to save a significant amount of capital towards sub-GHz spectrum for 5G roll out and additional capital expenditure required to be spent on network infrastructure to deploy the same.

• None of the existing spectrum expires before the year 2030, the validity of our spectrum pool ranges between the years 2030 and 2042 and we do not expect to incur any significant capital expenditure towards spectrum acquisition until the specific spectrum band expires.

5G ready:

• 5G Plus services are deployed on the recently acquired 3500 Mhz band in non-standalone mode with dual connectivity.

• The non-standalone network utilises dual connectivity of 5G and 4G spectrum to extend the 5G coverage for a given service level without the need of dedicating sub-GHz spectrum in 5G, thereby providing higher coverage at lower cost.

• Non-standalone network deployment has lower capital expenditure requirements, low cost of ownership, reduced environmental impact due to lower overall power consumption on account of fewer 5G radios and has been the widely chosen network architecture with approximately 85% of telecom operators worldwide initiating 5G deployment based on such architecture.

Premiumization strategy similar to Bharti Airtel Limited:

• BHL has a distinct strategy to premiumise their portfolio by acquiring and retaining quality customers and deliver an experience to them through our omnichannel approach and use of data science.

• They have a gamut of digital offerings to enhance customer engagement and differentiated customised offerings through family and converged plans under Airtel Black proposition, which has resulted in the continuous improvement of revenue market share during the last three Fiscals.

Cost optimization an ongoing process:

• BHL undertakes prudent cost optimization measures to improve their profitability and maintain an efficient capital structure with a comfortable leverage position.

Investment in network:

• BHL continuously invests in network expansion, technology advancement and judicious spectrum investments.

• As of September 30, 2023, they had invested 20,300cr in capital expenditure in future ready digital infrastructure.

Distribution:

• BHL has set up 18 retail outlets and 8 small format stores to reach 88 cities, as of September 30, 2023.

• Their distribution network comprised 617 distributors and 88,586 retail touchpoints.

BAL acquired 70% stake in 2004:

• Company was originally incorporated in 1995 as ‘Hexacom India Limited’.

• In 2004, the name of the Company was changed to ‘Bharti Hexacom Limited’ when Airtel acquired a majority equity interest in the Company.

• BAL acquired the stake from Shyam Telecom.

Broadband strategy:

• Strategy for fast paced network coverage expansion , network deployment and having an asset light business model has been backed by partnerships with local cable operators (“LCO”) in most of the regions we operate.

• Such arrangements led to faster roll out of fiber home passes, shorten time for go-to-market beyond larger towns and accelerate revenue growth.

• This has enabled BHL to provide high speed and reliable broadband connectivity to customers

Key Risks:

-

Concentration risk as BHL operates in Rajasthan and size states of North East.

-

Regulatory risks – relevant for the entire industry.

-

Change in CAPEX policy with parent resulting in higher CAPEX for BHL.

Conclusion:

-

Tariff hikes are imminent in the sector.

(India’s ARPU to GDP per capita is ~1.0% in FY23 vs 1.5% before FY15) -

BHL can pay for CAPEX, upcoming spectrum dues and dividend from internal accruals and it will be left with surplus.

-

Healthy cash flow surplus expected which will reduce net external debt of the company.

-

BHL ROCE can improve beyond 20% in next 2 years.

-

Potentially, BHL can double its PAT in next 3-4 years.