About the company

Established in 1946, Bharat Bijlee Limited is a leading electrical engineering company in India. The company has two primary business segments—(i.) power systems that comprise the transformers and projects divisions; and (ii.) industrial systems comprising electric motors, drives and industrial automation, and elevator systems divisions. It caters to an array of industries such as power, refineries, steel, cement, railways, machinery, construction, and textiles. Its project division undertakes turnkey projects (switch yards) and is well positioned to provide complete ‘concept to commissioning’ services. Headquartered in Mumbai, BBL’s sales and service network is spread across 13 regional offices in India. Its manufacturing facilities are on a 1,70,321-sq.m. campus at Airoli, Navi Mumbai, with a working area of approximately 63,000 sq.m. The company employs about 1,400 skilled personnel.

Key financial indicators

FY2022 FY2023

Operating income 1,265.7 1,418.5

PAT 55.6 83.2

OPBDIT/OI 6.9% 8.4%

PAT/OI 4.4% 5.9%

Total debt/OPBDIT (times) 3.3 2.5

Interest coverage (times) 3.6 4.9

Partnership

The Co/ has partnered with KEB of Germany for the distribution of their Variable Frequency Drives. KEB’s AC Variable Drives up to 900 kW are also manufactured at its plant. In addition, the company provides DC Drives, Servo system solutions, and an entire gamut of industrial automation solutions for enhanced precision, productivity and efficiency

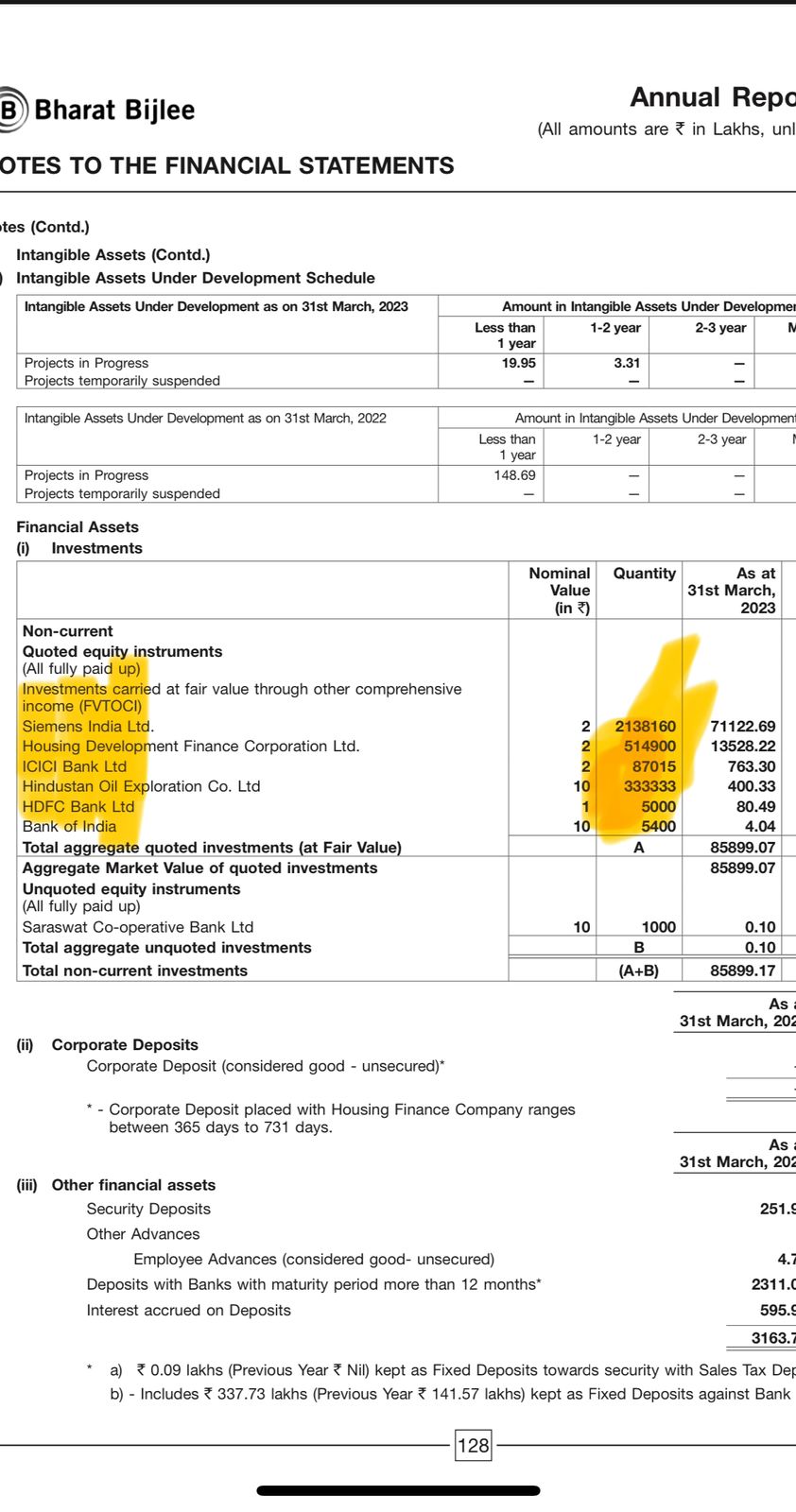

Current Mcap of company is 2379 cr Trading at 25 P/E. The Co. also has investments of ~Rs. 890 crores as of March 2023. These investments are mainly in the form of equity holding in companies like Siemens, HDFC Bank, ICICI Bank etc.

Can be beneficiary of Power sector theme

invested and biased.

Update from Automation Expo at Mumbai, Maharashtra

Bharat Bijlee’s servo drives leverage in import substitution

Bharat Bijlee has launched its synchronous AC servo drives and motors portfolio two years ago with its technology partner, Germany’s KEB Automation. BB is the first domestic company to offer an indigenized portfolio and aims to leverage demand arising from import substitution. It is used for cyclical applications that need accurate positioning. End-user industries are plastics, printing & packaging, metals, textiles and machine tools. It is usually priced at a 50% premium to the regular motors.

Bharat bijlee also showcased Synchro Connect – Smart IIoT (industrial internet of things) Gateway,’ strengthening its digital offering. It enables user to receive real-time data from machines, meters, and drives. Other highlights included Bharat bijlee’s IE5 category electric motors, which is one of the most energy-efficient motors range.

It is also important to highlight risk,

From latest credit report Operations remain linked to investments in power and capital goods sectors; exposed to intense competition in transformer as well as motor segments – BBL’s operations are inherently linked to strong revival of investment activity in the power andcapital goods sectors. Thus, such investments will remain critical for the company to ramp up its scale of operations in the medium term. Also, the demand–supply situation in the domestic transformer industry, remains challenging on account of

issues posed by the power sector in terms of large capacity additions (especially in thermal and gas-based units), leading tostiff competition, limiting the pricing flexibility for most players in the segment. Moreover, in the motor segment, the competition remains stiff, given the large MNCs as well as domestic players in the field, apart from more standard product offerings compared to customization available in the transformer portfolio.

Elongated receivable cycle due to slow payments from SEBs – BBL’s receivable days remain over 100 days due to elongated payment cycle from the SEBs. Nevertheless, the collection cycle has improved over the last two fiscals to 105 days in FY2023 compared to over 126 days in FY2021. This is because the company has started catering to more private players due to the relatively shorter credit period. Further, government has also taken measures to support the SEBs through various financing

schemes for timely payments to its vendors.

Susceptible to variations in raw material prices; events of any non-applicability of PVC or invocation of LD clause remain an ongoing challenge to profitability levels – Typically, ~70-80% of BBL’s contracts for transformers come with PVCs, while the rest are fixed-price contracts. For electrical motors, only fixed-price contracts are prevalent. This is because of the lower lead time for manufacturing these products and the large proportion of sales to retail segments. Although BBL is protected against

any raw material price increase in case of PVCs, it is sensitive to variations in copper and Cold Rolled Grain Oriented (CRGO) steel prices for fixed-price contracts. This is because BBL buys copper and CRGO steel in spot markets, where their rates are volatile, while immediate and full pass-on of the increase in costs to customers is not always possible.

1.BBL have implemented a business development program a few years ago to increase non-tendered

business from customers. This effort has borne rich dividends and has enabled us to grow our unexecuted order book by almost 50% (in Rupee terms) as compared to the previous year. The order book now stands at its highest ever

2.The Motor business has grown 16% over the previous financial year. Our drive to expand geographically has bolstered sales in many new territories

3.In the Drives and Automation topline is up 38% over the previous financial year.The division has procured some breakthrough orders with e-bus manufacturers and these orders are under execution. Our in-house developed IIOT (Industrial Internet of Things) solutions cater to the areas of predictive maintenance and OEE (Overall Equipment Effectiveness). OEE is a measure of how well a manufacturing operation is utilized as compared to its full potential

4.The Magnet Technology Machines division has grown by 39%.A smaller range servo motor is under development; this will cater to industries like textiles, packaging and printing.

The successful in-house development of these motors has been a great achievement.

5.The Magnet Technology Machines business exported during the year its first 3000 Nm direct drive motor for a special printing press to our technology partner Permagsa in Spain. Engineered in association with Permagsa, the air-cooled motor, has a modified PM rotor, with special hollow shafts and end shields for increased efficiency.

6.The Company has not entered into material related party transactions as defined under Section 2(76) of the Act and Regulation 2(1)(zb) of the Listing Regulations, during the Financial Year under review.

Seems post Covid it got opportunity to work with Private partners who were earlier happy with Chinese imports. With Demand Supply Gap it commanded premium as well same can be seen in Operational parameters and Working Capital , Inventory and debtor days.

Question is can they Continue the trend and become less dependent on SEBs ?.

Any new product in line to take legacy business to next level and improve OPM ?.

Fundamentally it’s a decent company but growth is what drives Market value.

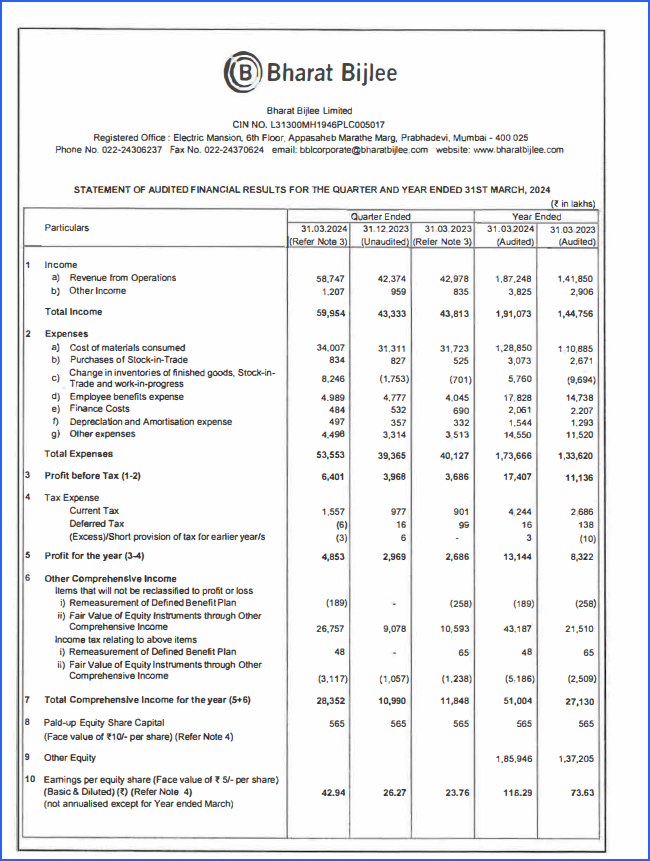

Transformer sector is one of the hot sectors these days due to shortage and strong demand from conventional and renewable sector. Bharat Bijlee is one of the lesser discussed names in the whole theme but a consistent performer. The company has posted very strong Q4FY24 results, possibly, the highest growth in the listed transformers’ space.

Net profit up 80.3% at ₹48.5 cr vs ₹27 cr (YoY)

Revenue up 36.7% at ₹587.5 cr vs ₹429.8 cr (YoY)

EBITDA up 58.5% at ₹61.5 cr vs ₹38.8 cr (YoY)

Margin at 10.5% vs 9% (YoY)

Net Cash flow from Operating Activities ₹241 crores

Dividend ₹35 per share (post split)

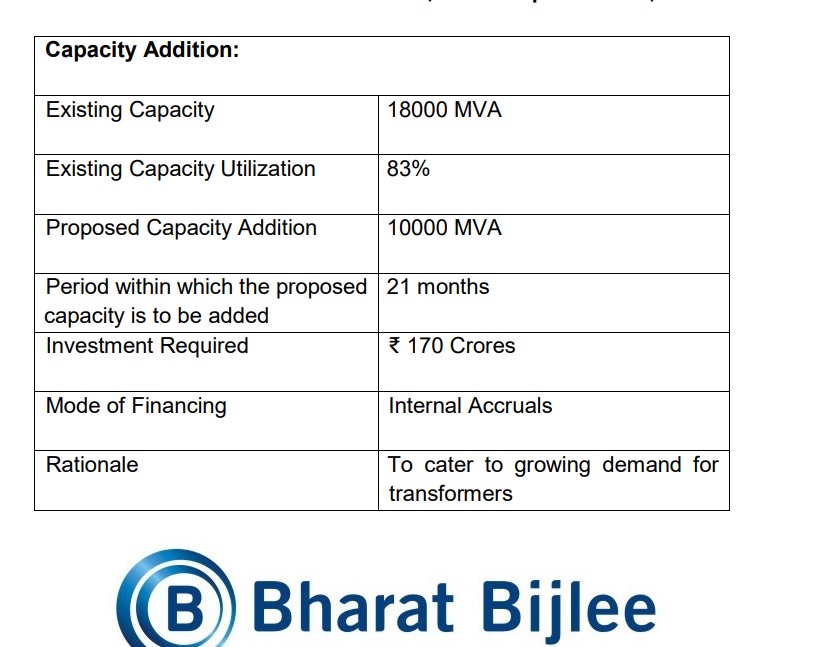

Company also announced capacity expansion from 18000 MVA to 28000 MVA for transformers to be funded through internal accruals

Current Market cap of the company is ₹4182 crores with a debt of Rs. 150 crores. Cash and cash equivalents stands at ₹380 crores as on 31st March 2024.

Interestingly, they have large equity investments, majorly in Siemens Limited and other listed companies which are valued more than ₹1700 crores as on today. They own more than 21 lakhs shares of Siemens Limited. So cash and investments are almost ₹2100 crores which is more than half of the current market cap. Enterprise value comes to around ₹2200 crores at EV/EBITDA of 12.

It is puzzling that with this much cash available what is the need of debt. It is also not clear as to what company plans to do with this much cash. Let’s hope company clears the air with better communication with the shareholders through concalls and presentations. With the growth and demands in the sector, Bharat Bijlee Limited seems to available at pretty cheap valuation when peers are trading at exorbitantly high multiples.

Considering the Capex announcement and now a little correction its available at EVEBITDA

21.4. Can this be still a good investment at this level. What bothers is no con call or disclosure from management. Any latest update would be appreciated. Anyone tracking this business?

I think EBITDA can be low if we deduct liquid investment and cash in the book. Considering that, in my opinion it is cheapest reputed transformer company in the market. Can be a value buy and will be cheap on more correction.

Is Anyone tracking this company?

Looks to have better FY26 numbers as transformer capacity addition to flow in by Q1FY26 from 18,000 MVA to 28,000 MVA.

More Details from latest Credit Report:

Happy Investing,

Karthik

Disclosure: Not having any position. Interested to learn more due to attractive valuation and future growth prospects.

Bharat Bijlee’s employee costs are almost 2.5x those of peers like Voltamp, despite operating at similar capacities. This higher cost base is also visible in its operating profit margin and PAT, where the gap with peers is evident. The key question: is this structurally higher cost weighing down long-term profitability, or is it a conscious investment in capability that will pay off ahead? Would be great to hear the community’s tracking and views on this