Company: Bhagyanagar India Ltd

Sector: Metals/Recycling/Copper

Basic Details

• Market Cap: ₹500crores

• Current Price: ₹156 (as of March 9 / 2026)

Financial Highlights

• Revenue (Latest FY): ₹1626crores

• Net Profit: ₹ 14 crores

• ROE: 5.7 %

• Debt-to-Equity: 1.63

• Revenue Growth (3-year CAGR): 1.09 %

Business Overview

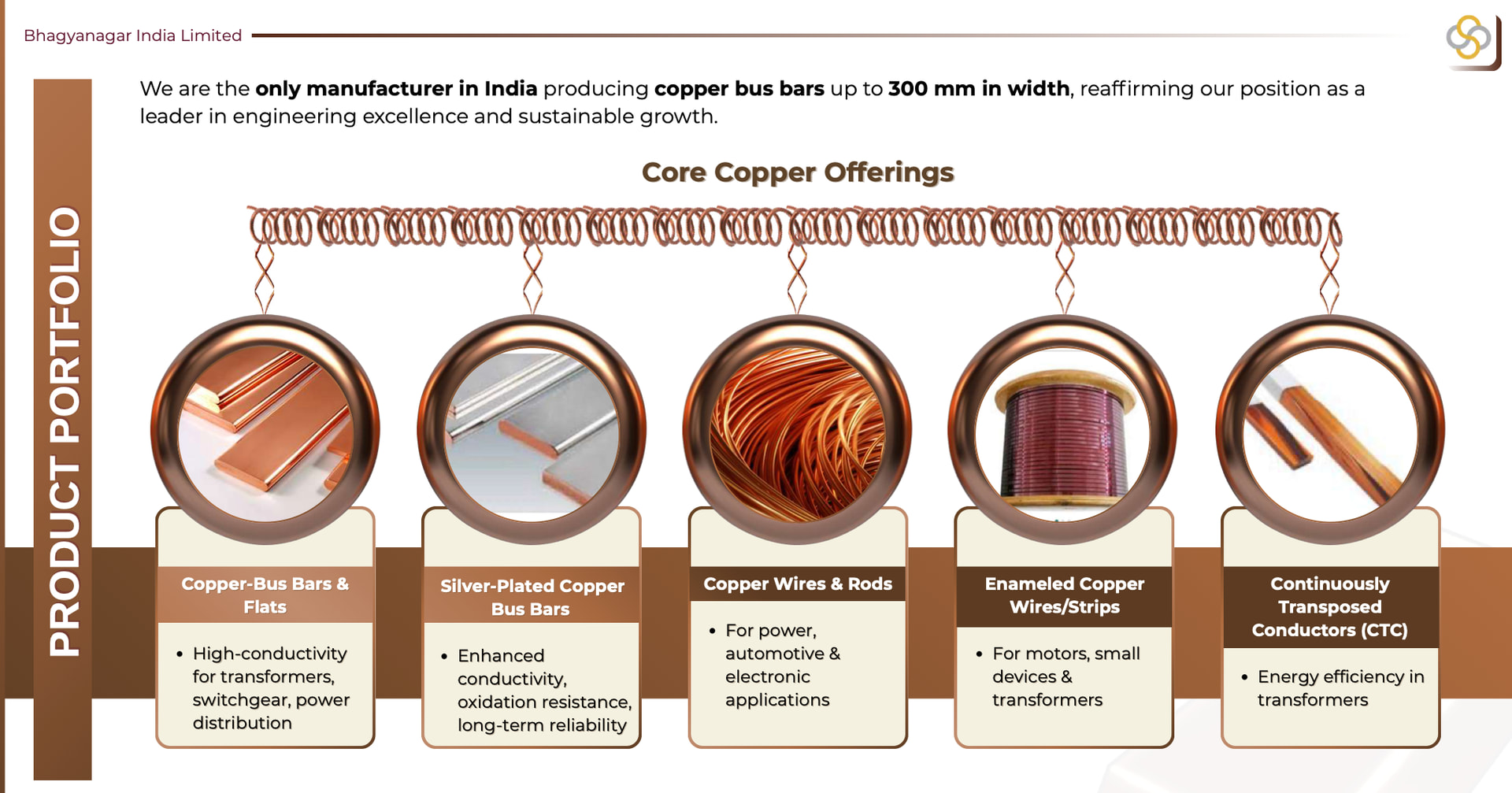

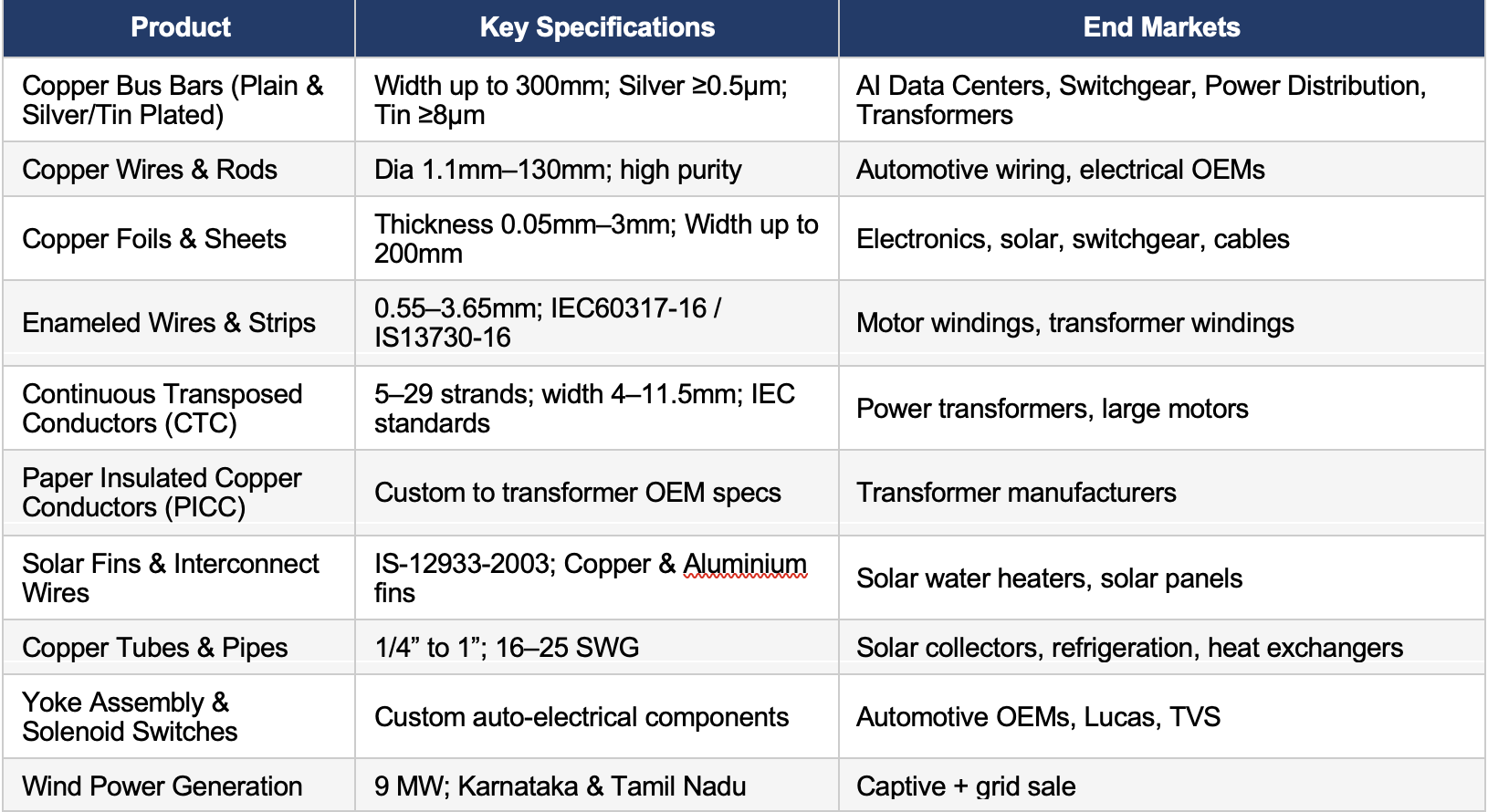

• Manufactures Copper products like Bus bars, Copper wires&Rods, Enameled Copper wires/strips ,CTC, PICC, Copper Foils and Sheets etc

Market Position: Market leader in Copper Bus bars

• Key Customers: L&T, Lucas TVS, Medha, Racold, HBL, ReGen, Vguard, Toshiba

Management Quality

• Promoter Background: Mechanical Engineer, PGDBM, IIM Bangalore

• Promoter Holding: 65%

• Key Management: Sri Devendra Surana ,MD and Advait Surana , Business Development Manager

Investment Thesis

Positives:

-

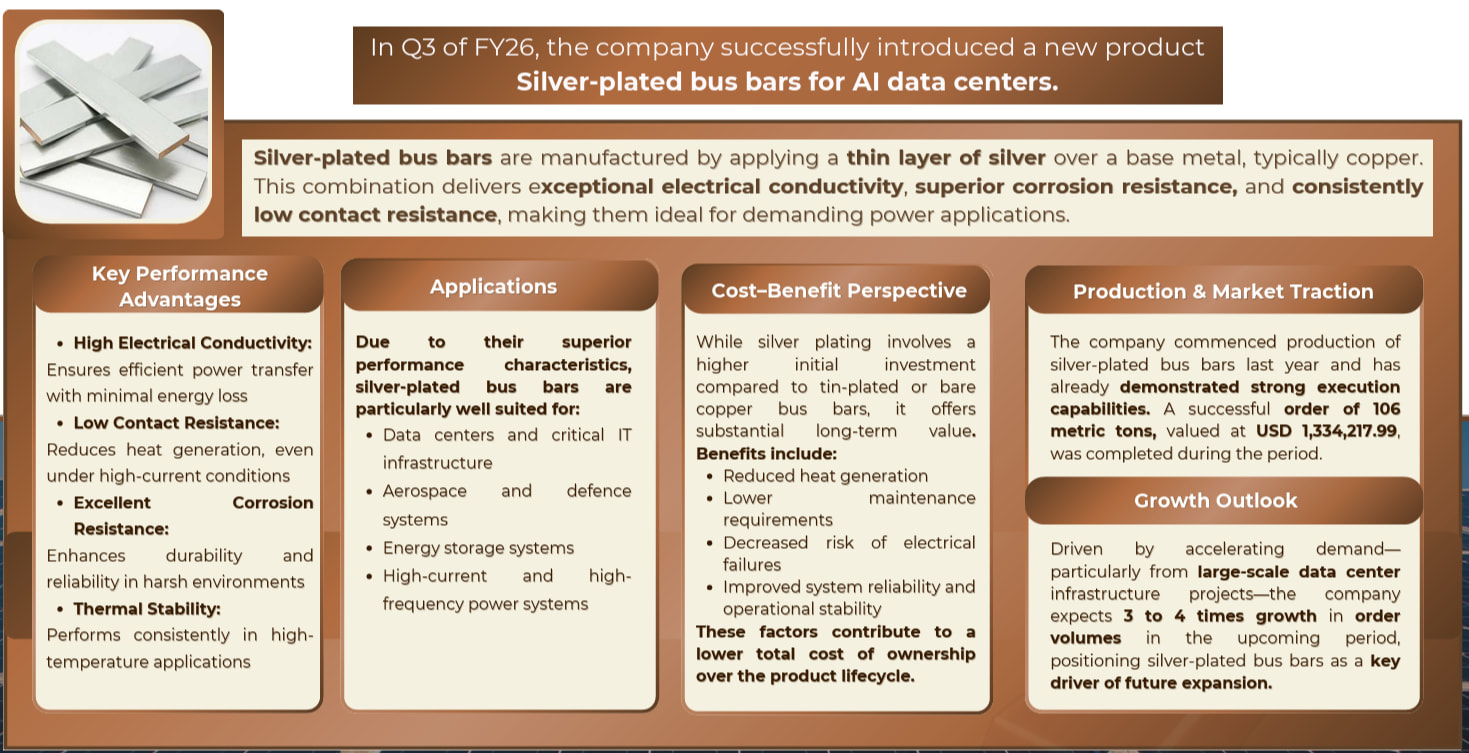

Bhagyanagar India Limited (BIL) sits at the intersection of three powerful structural megatrends: the AI-driven data center construction boom, India’s clean energy transition, and the industrial copper supercycle. Through its fully-owned subsidiary Bhagyanagar Copper Private Limited (BCPL), BIL is India’s largest copper bus bar manufacturer with unique silver-plating capability — positioning it as a high-margin supplier to the fast-growing AI data center market.

-

KEY INVESTMENT CATALYSTS

① Silver-Coated Bus Bar for AI Data Centers — unique product with high-margin niche and rapidly growing demand

② Structural Demerger (Tieramet) — copper business to be separately listed, unlocking significant holding company discount

③ Revenue Inflection — H1 FY26 revenue ₹1,065 Cr (+37% YoY); PAT ₹25 Cr (3.5x YoY growth)

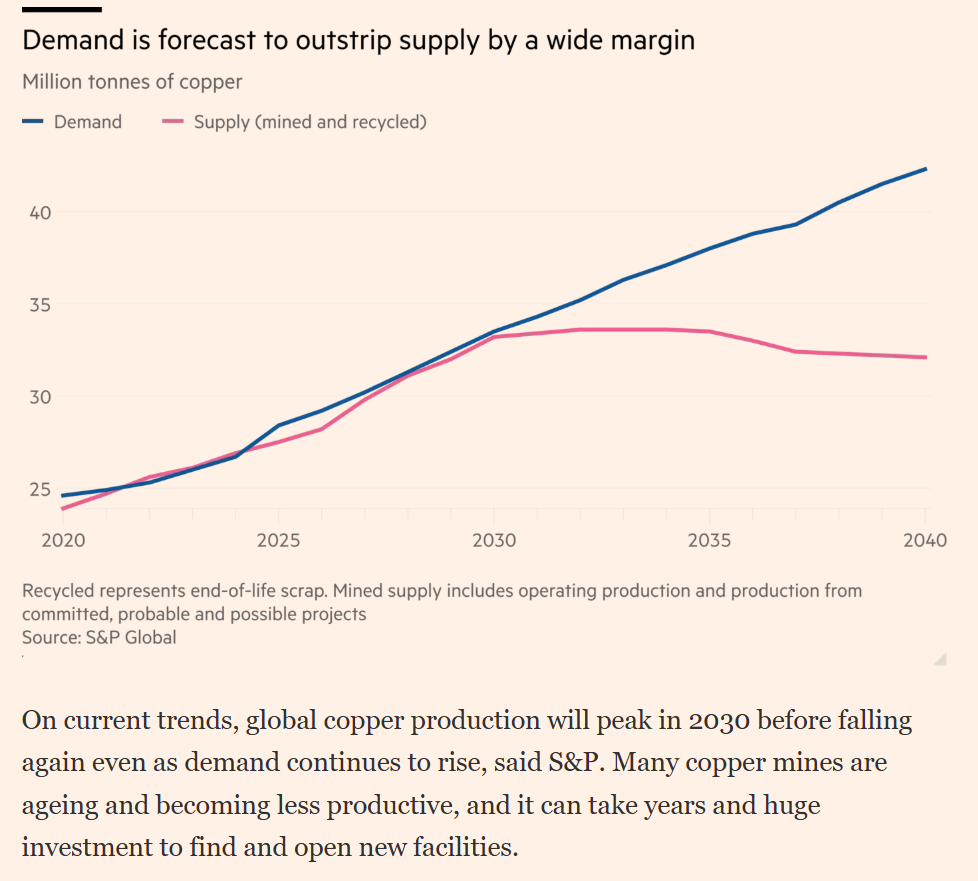

④ India’s Copper Supercycle — demand growing at 2x GDP; BIL well-positioned with 30,000 MT capacity and scrap recycling capability

⑤ 40-Year Profit Track Record — uninterrupted profitability and zero defaults to any creditor since inception in 1985.

Bhagyanagar India Limited, formerly Bhagyanagar Metals Limited, was incorporated in 1985 by the late Shri Gulabchand Mangilal Surana. It is the flagship listed company of the Surana Group, based at IDA Nacharam, Hyderabad. The company is among India’s largest pure-play copper fabricators with an annual turnover exceeding ₹2,000 crore. It operates through two segments: Copper Products (~99% of revenue) and Wind Power (9 MW in Karnataka and Tamil Nadu).

-

Corporate Restructuring — Tieramet Demerger

In FY24, BIL transferred its copper operations into a wholly-owned subsidiary BCPL, effective January 1, 2024. The NCLT Hyderabad Bench approved a composite demerger scheme on January 29, 2026. Under this scheme, BCPL will be amalgamated back into BIL, and the combined copper business will be demerged into a new listed entity, Tieramet Limited. BIL shareholders receive Tieramet shares at a 1:1 ratio. The remaining BIL will hold wind power, real estate, and other assets. Stakeholder meetings are scheduled for March 14, 2026.

-

CORE BUSINESS & PRODUCT PORTFOLIO

BIL (via BCPL) is India’s largest manufacturer of copper bus bars up to 300mm width — a natural moat in the premium bus bar segment. The company serves 500+ OEM customers across auto-electrical, solar, switchgear, and transformer industries. Key customers include Lucas-TVS, Amar Raja Batteries, BHEL, and Crompton Greaves. Over seven years, management has strategically shifted from commodity copper (~2% EBITDA) to higher-value-added products (~6-12% EBITDA margins).

BIL’s Positioning — A Rare Indian Supplier

From BCPL’s official product brochure: the company offers silver coating on copper bus bars with a minimum thickness of 0.5 microns and tin coating with a minimum thickness of 8 microns, both per customer specifications. BIL is already the only manufacturer in India capable of producing copper bus bars up to 300mm width — a dimension specification directly relevant to high-current power distribution runs inside data centers.

Notes from the Concall

- Bhagyanagar upgraded the technology by importing equipments from the best of the world viz : Outokumpu , Finland as early as 1988.

What is the Outokumpu Continuous Upcast (CCU) process?

Outokumpu (Finland) invented the Continuous Upcast (CCU) casting technology in the 1960s, and it remains the global gold standard for producing oxygen-free, high-conductivity copper rod and wire directly from molten copper cathode.

How it works — the physics:

Traditional casting pulls molten copper downward (gravity casting), which causes oxygen and impurities to settle unevenly, creating micro-porosity and inconsistent conductivity. The Outokumpu CCU method does the exact opposite — it draws molten copper upward through a graphite die into a water-cooled crystallizer. The upward pull, combined with the absence of atmospheric oxygen exposure, produces a rod with:

Oxygen content < 3–5 ppm (vs. 200–400 ppm in conventional casting)

Virtually zero porosity and no inclusions,A perfectly uniform, fine-grained crystalline structure.Conductivity rating of 101–102% IACS (International Annealed Copper Standard) — essentially pure electrical-grade copper.

-

The company added backward integration and started scrap recycling facility outside Hyderabad with a capacity of 25000 MT /Annum.

-

Current capacity is 30000 MT/Annum by Q4 the capacity is to enhanced by 5000 MT to 35000 MT/annum.

-

They are also getting into plastic recycling since they get around 800 tonnes of plastic along with the copper scrap .

-

Both copper and plastic recycling would help them to garner EPR credits .

-

They collect copper scrap from across the globe .

-

Bhagyanagar India is going to be demerged to “Tieramet “- which will house the copper business and the debt where as Bhagyanagar India will house the land parcels in and around Hyderabad along with the wind power assets with a book value of Rs 30 cr.

-

The management clarified that the land parcel is around 4 lakh square ft in the eastern side of Hyderabad where city is expanding, the conservative valuation of the land parcel is 200-300 cr that they are holding.

-

Post demerger the shareholders of Bhagyanagar India will get 1 share each of Teiramet and 1 share of Bhagyanagar.

-

Management aspires to build 5000 cr topline by FY 29 (FY 25 revenue 1600 Cr) with 5 % EBITDA margin and 3% PAT margin.

Risks and Challenges :

• The debt to equity is on the higher side. Current Longterm debt is 90Cr and short term debt is 270 cr and Interest paid is 30 Cr /annum.Management is not planning to reduce debt , instead their aim is to keep it constant while increasing the rate of revenue

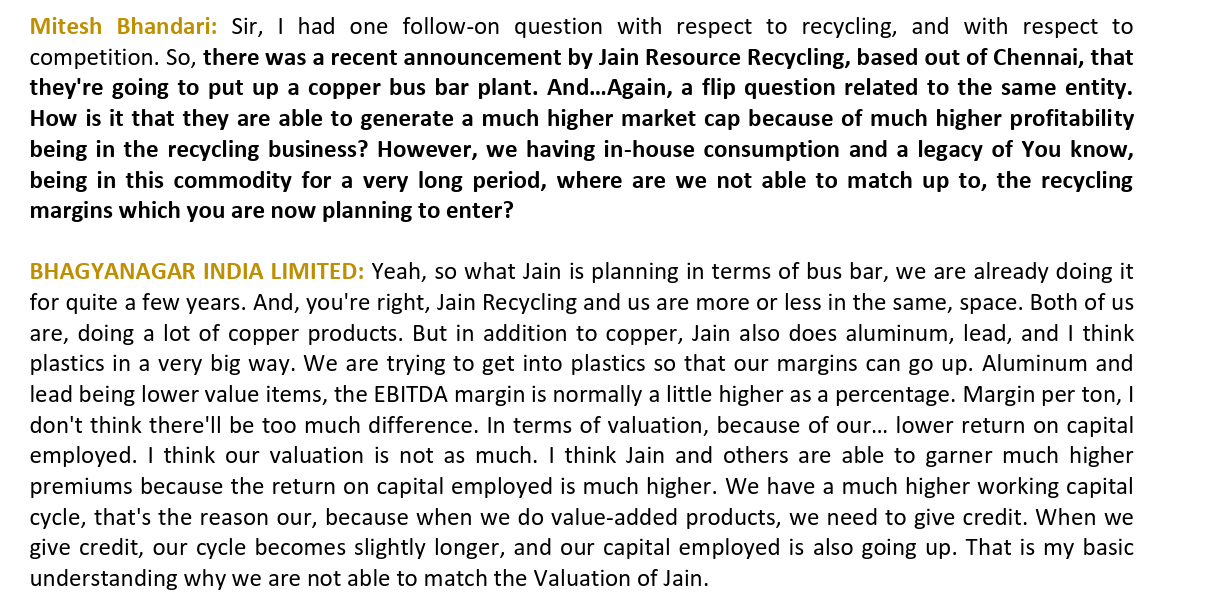

• The ROE and ROCE is very low . Their competitor JAIN Resource Recycling is commanding 14500 Cr market cap and 42 P/E . They are into Recycling of copper , Lead and Aluminium recycling and is also getting into Copper Busbars. The management was candid enough to admit that Jain commands a higher premium due to their higher ROCE . Management attributed the lower ROCE to the higher credit terms for value added products which depresses their WC cycle.

• BIL’s margins are thin (4-5% EBITDA). A sudden copper price fall reduces inventory valuations and customer pull-forward buying. Conversely, sharp price spikes may squeeze realizations if customers delay purchases. Scrap recycling partially hedges this but doesn’t eliminate it.

• The data center bus bar opportunity is nascent. BIL has technical capability but has not disclosed confirmed large DC customer wins publicly. Delays in DC order book ramp could mean the premium story takes longer to materialize than assumed in our base case model.

- International bus bar manufacturers (Siemens, Schneider Electric, Eaton, ABB) and larger Indian cable companies (Polycab, Havells) could aggressively enter the silver-plated DC bus bar market as demand grows. BIL’s advantage is dimensional specialization and cost, but lacks global brand recognition with hyperscale DC procurement teams.

Valuation- Back of the Envelope

FY 29 Revenue (E) = 5000 cr

EBITDA @ 5% = 250 cr

PAT @ 3 % = 150 cr

At 20 P/E = 3000 cr market cap v/s current market cap of 500 cr

= 6x in 3 yrs ![]()

In addition to this the market value of the land parcel is worth Rs 200 Cr which should be unlocked once the demerger happens.

Disclosures:

Not invested presently. Building conviction and looking for disconfirming evidence to the thesis. Not SEBI registered. Please do your due diligence.