I said “mere” because JAIN is targeting an upwards of 200 to 400 Bps gain from its value addition being commissioned from this Quarter onwards.

So overall in profitability terms since JAIN has already a margin accretive business in form of Lead & lead alloy ingots, if they walk the talk, theirs consolidated profile looks to do better only, from here.

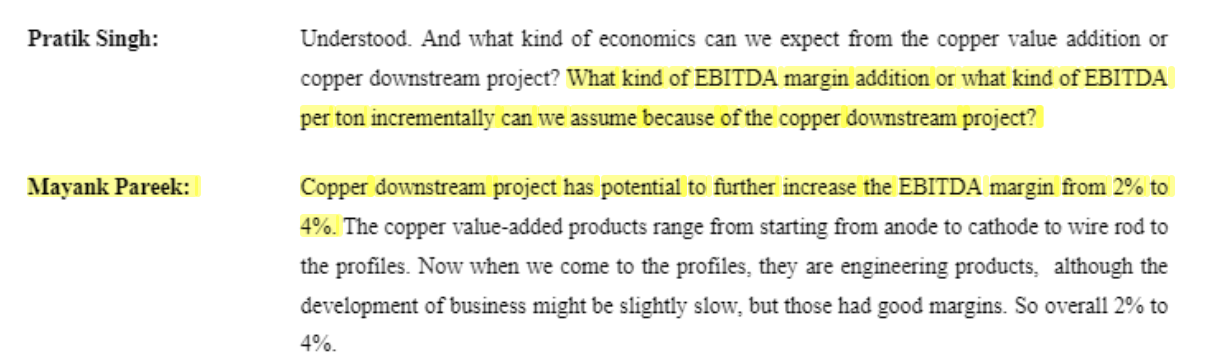

And their guidance of ₹32,000–₹33,000 per ton is without value added products considered.

Disc: I am invested in Bhagyanagar & not in Jain.

I am digging, if there’s a case to invest in JAIN or not.

2 Likes

They also guided huge numbers and reported 14,000 in Q4.

I don’t trust Jain’s guidance.

Will discuss when they achieve as guided.

1 Like

So typically all the forecasting model for bhagyanar were hovering around 62,000 Ebitda/ ton, assuming either steady state copper prices or increase in copper prices further for FY27.

But after 13th may 2026 hitting all time high of ₹1414/KG, it is constant in declining to as much as 10% down to ₹1275 on 23rd june 2026, that’s yesterday.

Has anyone modeled what the scenario would look like if it falls further 10-20% from here or the average realisation per Kg declines 20% from FY26 levels and what would that mean for company’s P&L , Inventory (I guess the promoter hedges some part of it on MCX) & cash flows ?

2 Likes

One way to model this: roughly 3% of copper’s price is recycling EBITDA, and 25,000/ton is fixed value-added EBITDA.

So at a copper price of 1,260/kg (Q4 realization):

-

Recycling EBITDA/ton = 0.03 × 1,260 = 38/kg

-

Value-added processing EBITDA/ton = 25/kg (Can increase with more value addition)

-

Net = 63/kg

This calculation was explained in the interview.

6 Likes