Bew engineering – founded in 2011 and is involved in design and manufacturing of pharmaceutical plant equipment. The company manufacters – filtering, drying and mixing equipment. Some of the products are as follows:

- ANFD Agitated Nutsche Filter Dryer

- Rotocone Vacuum Filter Dryer

- Rotocone Vacuum Dryer

- Cantilever Rotocone Vacuum Dryer

Market cap- 305 cr, P/E- 41.1

ROE- 26% , ROCE- 40%

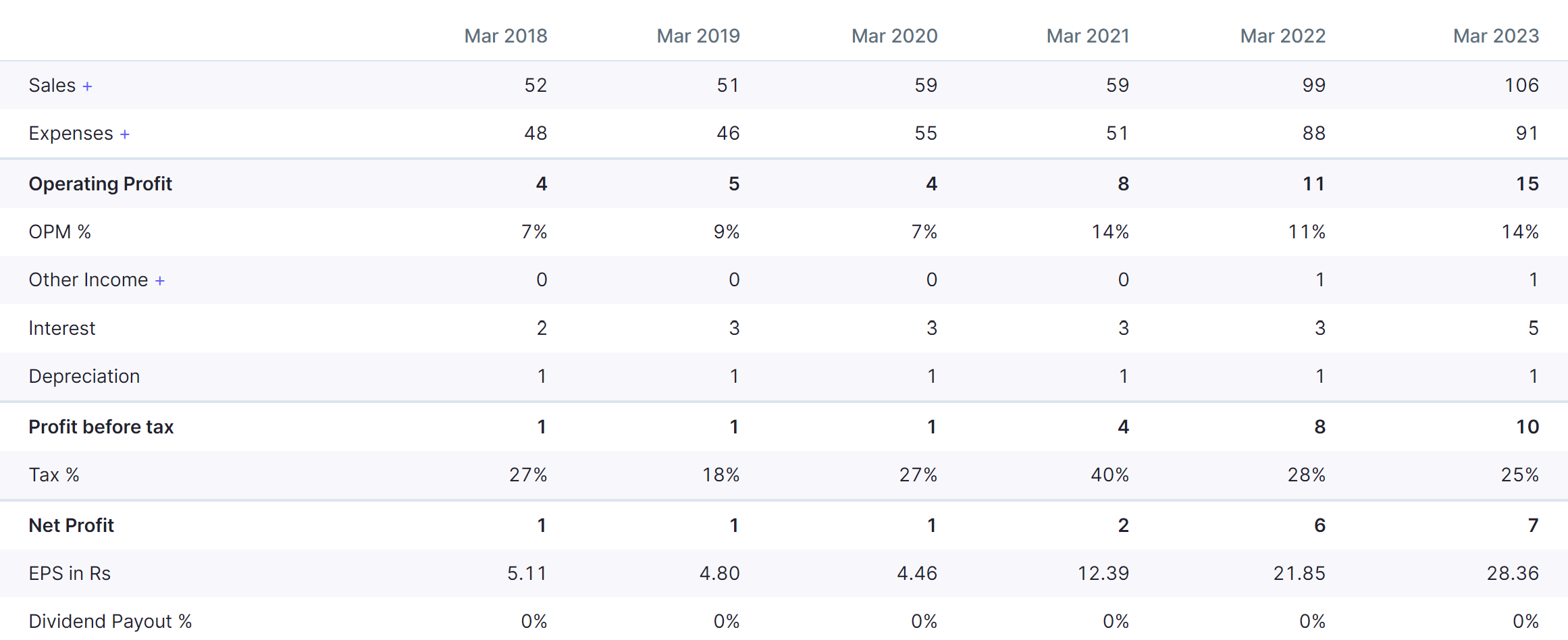

above is a snapshot of last 6 years of P&L of company

we can see the sales have scaled up from 52 cr to 106cr, while the OPM margins have increased from 7% to 14%.

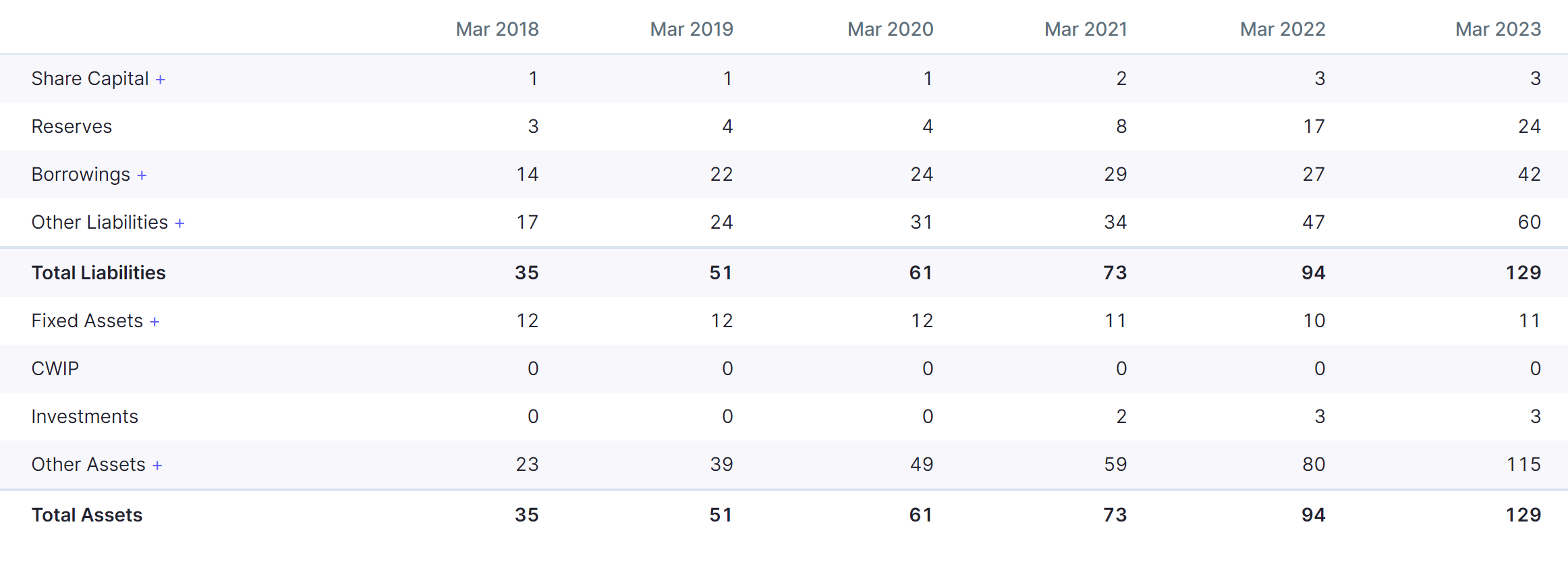

above is a snapshot of the balance sheet of the company over the last 6 years.

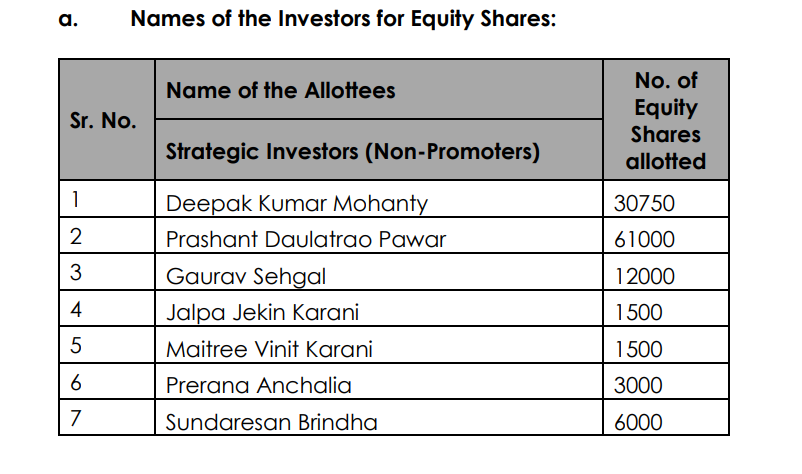

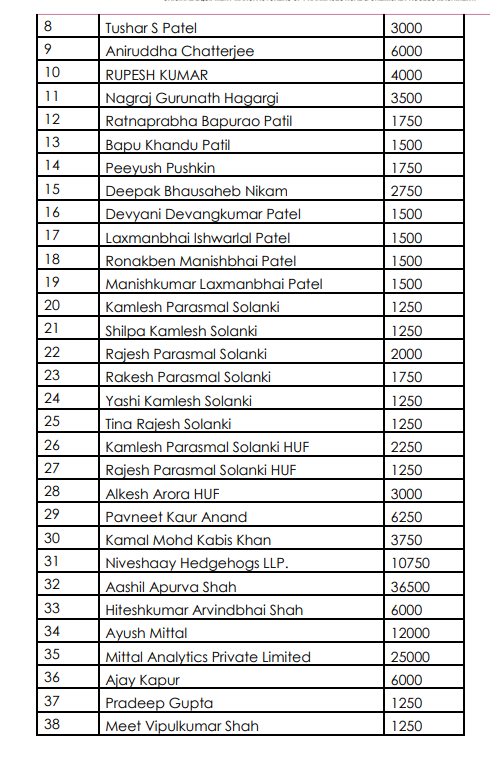

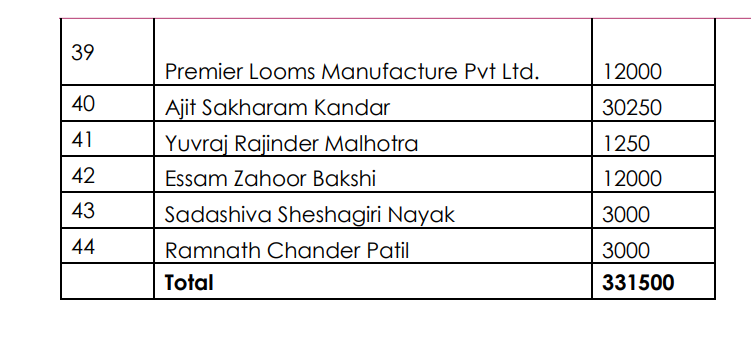

Company has recently done preferential allotment of shares – 3,31,000. At Rs.820. Approx 27 cr will be used for increasing its capacity

Company has an order book of 95 cr- to be executed in 7 months. FY23 whole year turnover was of 106 cr. Company seems on track to achieve 40-50% turnover growth this year. They have carried out debottlenecking and can achieve a turnover of 150 cr with the existing plant.

Exports were 2 cr in FY22. They have jumped to 23 cr in FY23.

Company has exported its equipment to countries like Turkey, Nigeria, Indonesia, Thailand, Saudi Arabia, Nepal, Bangladesh,etc.

Company has a strong client base- the marquee companies of the pharma and chemical sector.

Some of the clients of the company are – Aarti Industries, SRF, Intas Pharma, Lupin, Shilpa Medicare, Heranba Industries,Cipla, NGL finechem,Biocon, IPCA,etc. Most of these customers are coming up with huge capex plans. This provides a good opportunity for the company to grow.

Demand for companies products is directly related to the capex happening in the pharma and chemical sector.

Margins

Although the gross margins of the company are low, its OPM margins have risen from 7-9 % in the past to 13-14%. Seems like company is enjoying operating leverage with scale.

Competition

HLE glasscoat is one of the key competitors of the company- HLE has 23% of its revenues from ANFD- which is around 140 cr. HLE is also present in glass lined reactors where BEW has no presence as of now. Valuations of HLE are all together in a different range of 70-80 PE. Does not make sense to compare the valuations directly.

New equipments

Company has developed 2 new equipments in FY23- they are the sole suppliers of this equipment and will earn higher margins in them. Will be interesting to see which are these equipments and how fast they can scale up in this segment.

Working capital

The company has very less trade receviables- It was 12.68 cr as on 31st March 2023. 8.5 cr out of this were backed by LC- export orders. The amount has been received by the company as on 5th May 2023.

The company has maximum investments in inventory, as it is a capital intensive business. The average time taken to complete an equipment is 6-7 months.

Company has 88 cr of inventory as on 31st March 23 as against 67 cr FY22. This rise in inventory is to execute order for FY24 and is a leading indicator of growth in revenues.

Key risks

- Slowdown in capex cycle of pharma and chemical sectors can pose a threat to the growth of the company

- Rise in RM costs of raw materials- stainless steel, alloy steel, Hastelloy, titanium, rubber lining, etc are some of the raw materials used by the company. Company may or may not have the ability to pass on the increase in RM prices to the customer

- Company faces competition from big players like HLE Glasscoat, and GMM Pfaudler. They operate at a bigger scale than them and cometing against them will not be easy. Company’s gross margin is around 23% , much lower than that of the other two players.

Overall the company looks to be on a strong growth trajectory. The industries to which the company caters to are undergoing major capacity expansion. Management also seems bullish about the growth prospects. The latest fund raise of 27 cr is also signifying growth plans by the company. However valuations also seem to be rich at over 40 PE( trailing earnings). It has to be seen whether the company can improve its gross margins with scale( as it might have greater bargaining power over suppliers).

Disc- Not invested