They are in SME category and hence there is minimum purchase size

Hey everyone! I had purchased 800 qty of Beta Drugs shares very early on when it was only 53 rupees. I was very deep into equity research back then and I had gotten hold of their annual reports by emailing the investor relations. I got a prompt reply back right the next day with very detailed info (I guess simple things like these was one of the reasons I made my decision to invest early on) It has definitely paid off!

I am out of touch in equity research now as I am fully invested into my own startup (time and money) and I have not kept up with recent updates.

I want to thank you all for sharing your perspective here, I will read them closely as I hold on to Beta Drugs and as their narrtive evolves. I still don not have all the information or find any negatives to make any sell decisions.

4 Likes

National Cancer Grid

The initiative to bulk-buy drugs is led by the country’s largest cancer centre, Tata Memorial Hospital (TMH) in Mumbai. The initial list had 40 common off-patent generic drugs, covering 80% of their pharmacy costs, saving the group $170m.

The success of the scheme has attracted interest from hospitals and state governments across the country.

The next round will expand to over 100 drugs, while broader cancer care purchases like supplies, diagnostics and equipment are also being considered. However, more expensive patented treatments are currently not part of the plan.

“I think what pharmaceutical companies need to understand is in a market like India, unless you bring costs down, you’re not going to get the volumes and it’s a chicken and the egg phenomenon,” according to Dr C S Pramesh, Director of TMH and the Convenor of National Cancer Grid.

Disc: invested

5 Likes

I had written an in-depth report on Beta Drugs a few days ago. As per research company remains strong fundamentally with immense growth opportunity.

Beta Drugs - Utkarsh Batra.pdf (1.7 MB)

Do take a look at it.

15 Likes

Hi Utkarsh,

Thanks for the report and it is very helpful.

Curious to know if you are anyways related to Promotors of the company. Asking this because your surname is same as the Promotors and most of the info is from Annual reports published by the company.

Thanks,

Suresh

Hello Suresh Ji,

I’m glad you liked the report.

Fortunately or Unfortunately, I am not related to the promoters or even part of the company in any way, not even as a shareholder because it is an SME stock, and each lot costs upwards of 1,20,000. I am just a student with a lot of passion for the market and trying to learn and perform my limited investment activities as a professional/corporate.

Yes, most of the information is taken from the Annual Report and past concalls, because it is a really small company, information and data are not very readily available for Beta Drugs like companies with Market cap >10,000 cr. I have tried my hardest to get data from various sources to make it comprehensive and detailed but at the same time very crisp.

11 Likes

Just looking at the metrics interms of ROCE (>25% over 7 years), NPM (10-12% over 7 years) and operating margins reaching 18-19%. It seems like there is something special that BDL is doing as these numbers are being sustained over a 7 year period are very above average. It seems to be very difficult to identify the moat in BDL. Is it purely the sales team’s expertise? or is it the distribution network with multipe hospitals thats creating a very sticky business for BDL?

Whatever BDL is doing is different from the pack.

Any thoughts?

Secondly a bit concerning is how much remuneration the directors are getting paid. In 2022 and 2023 the two directors Varun and Vinod batra have taken salaries of 1.7Cr and 2.4Cr respectively which amounts to close to 7% of the NPM. Doesn’t this seem a little too high?

There are Multiple things they are doing right.

- Choosing the right drug

- Backward integration into 70% API’s of their Formulations

- To some extent R&D

- Focus on NDDS

- Rightly said Hospital network and their sales team / MRs

4 Likes

great job.

Adding a point, it’s expecting 290cr+ revenue for FY24.

1 Like

And paying pennies to Rohit Parti and Manmohan Khanna. Just the sitting fees. Not sure why they are working for them and what other arrangements they have with them.

Great report. Can you try to find something on Beta UBK

International Pvt. Because its not operational and not much info about the same in annual report. I had seen 2 videos on youtube about the same but nothing more than that.

I have recently started tracking this stock, all the parameters looks great, however, even with these great set of numbers consistently for 7 years, why has Beta Drugs not migrated to main board? Shouldn’t it have been migrated within 3 years itself?

1 Like

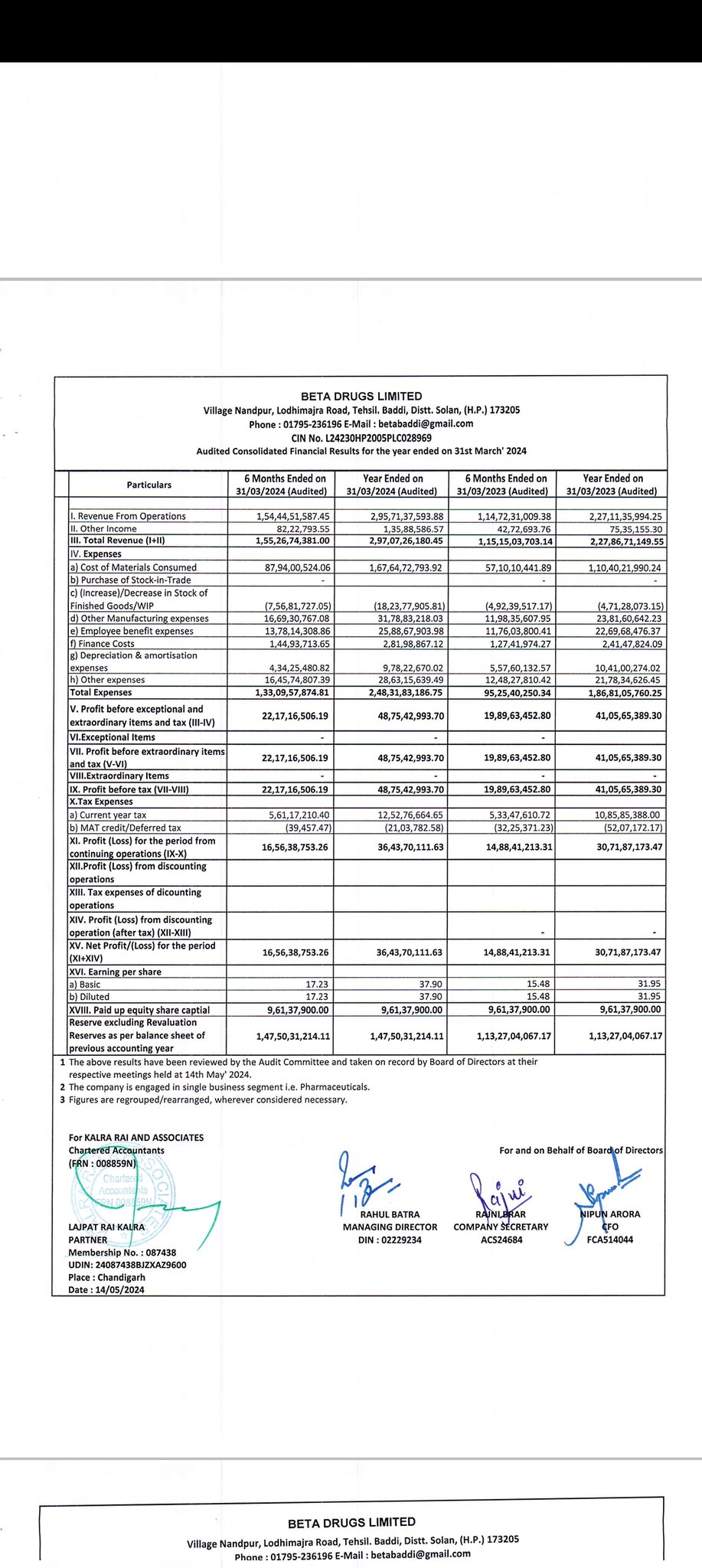

Revenue was on point as per the guidance, however there was a temporary decrease in margins as mentioned by the management below.

FY25 should be a good year for this stock, as the revenue will continue to grow at 25-30% and the EBITDA margins will return back to 24% - 26%

5 Likes

Q4FY24 Concall highlights:

- Ebidta declined due to high RM cost (platin which is a gold n platinum derivative)

- Platin cost comprises 14-15% sales

- Platin can’t be manufactured in house.

- Yearly sales breakup:

- Branded: 89 Cr (margin 33-36%)

- CDMO: 140 Cr (margin 15-17%)

- Exports: 46 Cr (margin 28-32%)

- API : 21 Cr (margin 22-23%)

- Derma: 6.83 Cr - halfyearly sales breakup:

- Branded: 41.5 Cr

- CDMO: 68 Cr

- Export: 30 Cr

- API: 11 Cr

- Derma: 3.3 Cr - Ebidta will try to bring to 26% in FY25

- Cosmotology:

- division posted net loss

- guidance FY25 min sales 14-15 Cr

- gross margin is 65%

- plant setup initiate by Fy25-26 ( 30 - 35 Cr)

- recently launched 5 products (haircare, sunscreen, moisturizer)

- Will focus on hair product segment

- Future target 35% of business

- Dr prescribed medicine after Dr approves. - Cleared audit n received registration cert from Urasia

- Cytotoxic syrup facility started

- Own brand, injectable: Oral = 43 : 57

- FY25 guidance 25-30% sales.

- 70% Api in house manufactured.

- 2-3 months will migrate to main board, process already initiated.

- export business target 35% business in future.

7 Likes

thank you for this write up. One big concern I have is with these companies that are engaged in branded formulations is that they are competing against their CDMO client who are using them to manufacture the same formulations. Wouldn’t clients prefer to have a pureplay CDMO vs a branded player?

Yes. Your concern is Genuine.

There are very few pure CDMOs which are not into formulations.

Divis’ , Suven are few of them. And they get higher valuations due to this.

dr.vikas

4 Likes

H2FY24:

• EBITDA margins stood at 21% - Primarily driven by two factors - one was a loss of Rs 4 crore in cosmeceutical division and second was due to higher raw material prices for Platins because of global price rise in gold and platinum prices.

• Beta has achieved a sale of Rs l crore in the month of April 24 for its Cosmeceutical division and has become marginally profitable.

• Also, the prices of Platins have gone down and moreover company is focussing more on the high margin products rather than platins for the next financial year.

• In addition, launch of 1st Suspension in February has given an edge to the company over its competitors and will impact margins positively going forward. (Caxfila OS 1st Indian brand of Megestrol Acetate Suspension)

• Beta has once again achieved a milestone by clearing Russian audit and hence received EUEA approval recently which will enhance its presence in Russia, Belarus, Armenia, Kazakhstan, Georgia and the company is well positioned for growth in regulated and emerging markets.

• GUIDANCE FOR FY 25: Revenues to increase by 25%to 30% while the EBITDA margins will be back in the range of 24%to 26%. Beta will do sales of Rs 15 crores in its Cosmeceutical division and thus adding profits to the company.

• In this financial year the company is expected to launch seven new products and NDDS.

• With approvals of EUEA, ANVISA, & INVIMA will drive exponential sales from exports in the next three years.

• Filed six syrups/suspensions as new product approval in DCGI: To be launch in FY 24- 25

• 53 new registrations in international market.

• 23 New products in the pipe-line

• Growth in FY ’24 –

Domestic Own Brand Business - 23%

CDMO Business - 28%

International Business - 65%

API Business - 15%

• COSMECEUTICAL-

Increased reach to 6000 customers

Increased prescriber base from 700 to 1100

Agreement with the European company for the First to launch products in Indian Cosmeceutical market

• CDMO Business - Capacity of lyophilized products has increased. It helped to reduce lead time for order execution.

• 450cr+ by FY26

CONCALL NOTES:

• First ever cytotoxic suspension facility. This is the first ever facility in Asia, Africa, Europe.

We have also introduced in this facility the first suspension that is megestrol acetate suspension in the domestic market. This product has got increased excitement in terms of doctors, and we have gained a respective market share in megestrol acetate. Not only this, bringing the NDDS to the market has increased the market size for this particular product.

In this particular year, we have also filed 6 more approvals in suspension and syrup segment. We hope to launch these products this year provided we get the approvals in time from DCGI.

• We have also strengthened our hematologic portfolio by adding 2 more products last year. This will continue building as a huge scope lies in the hematology segment. Out of both the segments, if we talk about the solid tumors and the hematology, the scope and the future lie in the hematology segment.

• EU GMP audit is going to happen in September, which will further add a lot of sales and international collaboration as we see that there are not many generic regulated approved cytotoxic plants available in the Indian market.

• In the CDMO business, last year we have shown a big growth as we have added 3 more new clients in our portfolio and some existing clients have added around 7 to 8 new products,

• The key highlights of API, we have developed and launched seven new products last year. We have also prepared 6 BMS which we are filing in the Brazil market in next month.

• COSMETOLOGY:

Our division name for cosmetology is Inspira.

We have already planned to come up with our own manufacturing unit by FY25-26. Today, the total number of SKUs are close to 14. We intend to increase the number of SKUs by 30 to 35 by the end of this FY24-25.

The total gross margins which we are getting in this division is close to 65%.

For cosmetology, the capex will be close to around Rs. 30 crores to Rs. 35 crores.

Actually, this is one segment which has been identical to oncology only because you are not making product available in the chemist. Every cosmetologist has their own chemist counters. So, it is one segment which has actually been replicated by the oncology side. So, that’s why we are focused on this segment only.

Migrating on to the Mainboard: we have already initiated the process. Maybe next 2 to 3 months, we will be migrating on to the Mainboard. Before our first quarter ended, we will try to be on the Mainboard before our first quarter ends.

• COMPETITION: So, the competition is there in the market, it’s for every business, right? But since we are the one only focused oncology company, we have certain special advantages. It is not only about the formulation, since we are backwardly integrated, that gives us an edge. And not only this, in certain products, we are the first one to launch in the Indian market. Last year, there was one product which became off patent, that was Olaparib. So, we have taken a huge market share once we launched that product, as we were the first one to launch that. So, this is the same strategy. The products which are becoming off patent, we have a list of products, we already developed that, there are certain products we will be launching this year also, and we will be taking that advantage.

• ACQUIRING MAs: The only investment we will be doing in acquiring the MAs once we are through with our EU GMP audit. So, we will not be following up the process of registering the product, rather we will be buying the MA and launching the same product in a lesser time as we go all out for the dosage registration

And regarding the CAPEX of around Rs. 7 crores to Rs. 8 crores or Rs. 10 crores, that’s an asset purchase that is called marketing authorization, product wise marketing authorization. Once we are through with the Europe approval, so we will be immediately going towards an acquisition of MA approvals. So, this is the main CAPEX required. It is not in terms of machinery, rather it is in terms of those bought from the market, particularly available in that market, so that we can immediately go and start the sales, which is a process of 3 to 4 years for registration.

• Platin is basically one product line which we cannot manufacture in-house. Today, 70% of our APIs are being produced by ourselves only, which we are backwardly integrated. And there are only two companies in India right now who are manufacturing this. One is Hetero Healthcare, one is Fresenius Kabi. So, we are procuring from them. And see, it’s not like we have seen that because if we go for a chemotherapy treatment, carboplatin and cisplatin is the basic treatment. And tomorrow we are joining, we are becoming a partner with any good CDMO player. So, the first product they will ask for is carboplatin only. But last 3 months, fortunately last 3 months, we have seen the prices have declined and we will be more focusing ourselves towards on the other product line rather on the platin side. Other products, there has been no cost increase. Rather, we have negotiated well from our KSM suppliers, and the API costs have decreased.

• So, this is one turning point and we, as a company, have laid down a strategy to focus more on the oral side. So, that’s why on my initial talk, I discussed shifting our focus from injectable to oral side because prescription business is always a long-term business.

• So, the top line would be, for the second half you want to know. The branded sales would be Rs. 41.5 crores, CMO business is Rs. 68 crores, export business is Rs. 30 crores, API is Rs. 11.7 crores and the Derma is Rs. 3.3 crores, so total comes to Rs. 154.44 crores.

• All capex will be from internal accruals.

• BIOSIMILARS JV: If we get an opportunity to get into the biosimilar in a JV with someone where they want to launch the product in India or anyone is developing those or they want some investment on the part of that, so we will be going ahead with that decision as well.

• In Colombia, we’ve already filed around 10 to 12 dossiers. In Mexico also, we have started filing dossiers. We have given around 24 dossiers. And this month only, we are traveling to this part of the continent, and we are taking an update from all our partners. In Brazil also, we have filed around 6 dossiers, and again, we are traveling there, so we will be having feedback from them when we are getting the registrations. Apart from these, we’ve already got 5 registrations in Peru. We have done business last year and we’ve got business this year as well, business estimate this year as well. We have also got some few registrations in Guatemala, in Ecuador, and in Nicaragua as well.

• US MARKETS: Recently, we have got the Beta plant audited by a US FDA regulator. So, he was in opinion that you can go for a US FDA audit immediately, but we are not in a hurry as we first want to establish ourselves towards in the Asian market, like specifically Southeast Asian market, Latin America market, and then there on move towards the Europe market. After that, definitely, we do have plans to enter US market in 3 years down the line.

• Whatever new developments or new product which we are going to launch in the Indian market, especially the PARP inhibitors. So, those products will be developed in our API plant and will be delivered to our formulations plant so that we can be the first one to launch those products in the Indian market.

• Yes, because this particular year will be having 6 new NDDS launched. We are expecting the approvals between October and March. So, those 6 new NDDS, new drug delivery system, will be the first time in India. This will definitely increase the margins.

• So, we have put our focus on these markets, and definitely you’ll see a huge upside in the next 2 to 3 years down the line, where export revenue will increase, and the margins will substantially increase. And the target, what we aim in the future, is that exports should contribute around 35% of the total business volume.

• Across all the segments in India, as per April is concerned, the highest CAGR is neoplastic, of course, the oncology, and the second highest CAGR, the growth is in the derma segment

• FY24 the breakup is branded sales Rs. 82 crores, CMO Rs. 140 crores, exports Rs. 46 crores. API Rs. 21 crores, derma Rs. 6.83 crores.

• See, branded sales always have more margin. It is somewhere around 33% to 36%, which branded has. 28% to 32% is exports margin. 15% to 17% is CMO margin. API, we have a standalone balance sheet. So, it shows me the correct margin automatically. So, that is somewhere around 22% to 23%. And Derma, we have already told you that 65% is the gross profit

(As branded sales and exports will gain momentum, margins are going to improve and thus guidance of 24-26% margin is justified)

• We try to make a GC in our own brands around close to 80%-85%

12 Likes