Every company posts in websites about research and researchers. Hardly will there be any research going on in most companies.

Hi Good Morning folks,

As per my knowledge this trades in NSE-SM & has a minimum lot size of 200 stocks.

How to know when it comes out of this fixed shares lot?

Through NSE announcements ?

Thanks in advance

dr.vikas

Yes Indeed. Whenever there is a change in lot size, you would come to know in advance though NSE website. https://www1.nseindia.com/emerge/circulars.htm

1 Like

Unrelated question. How do you find out when a SME stock will get listed on the main board?

1 Like

Companies will announce such plans time to time so you will have to keep a tab.

1 Like

Beta Drugs - Annual Report excerpt

-

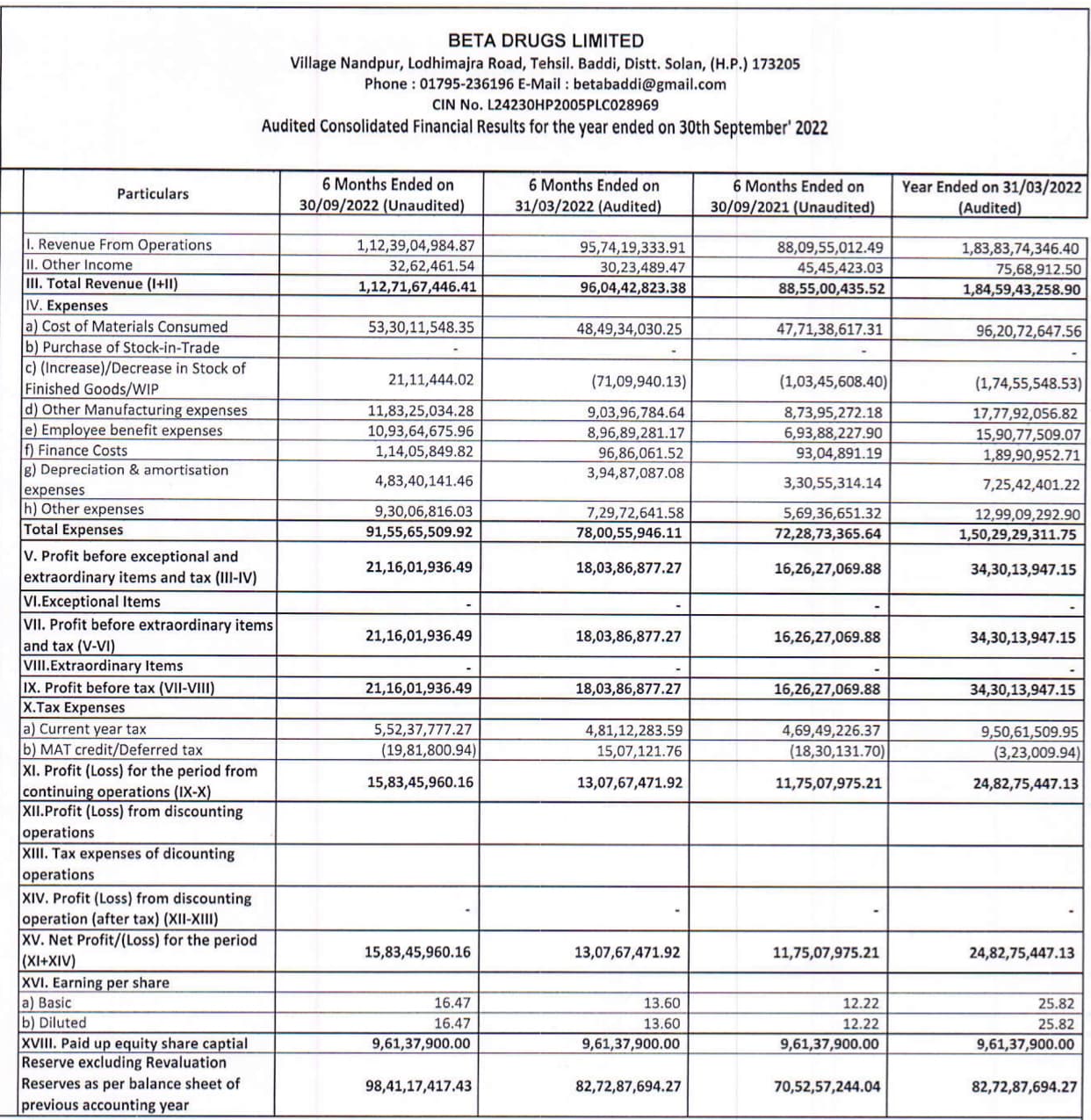

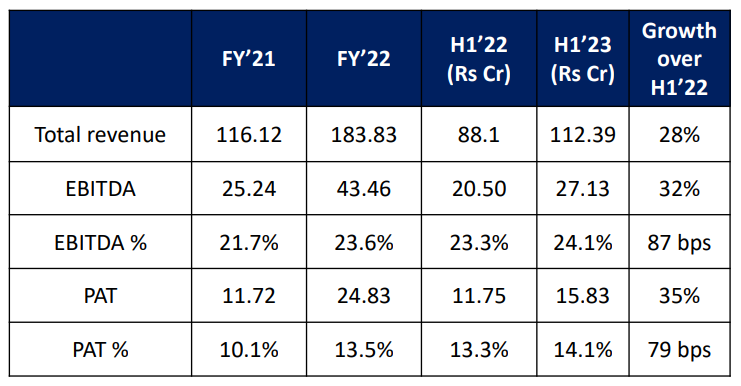

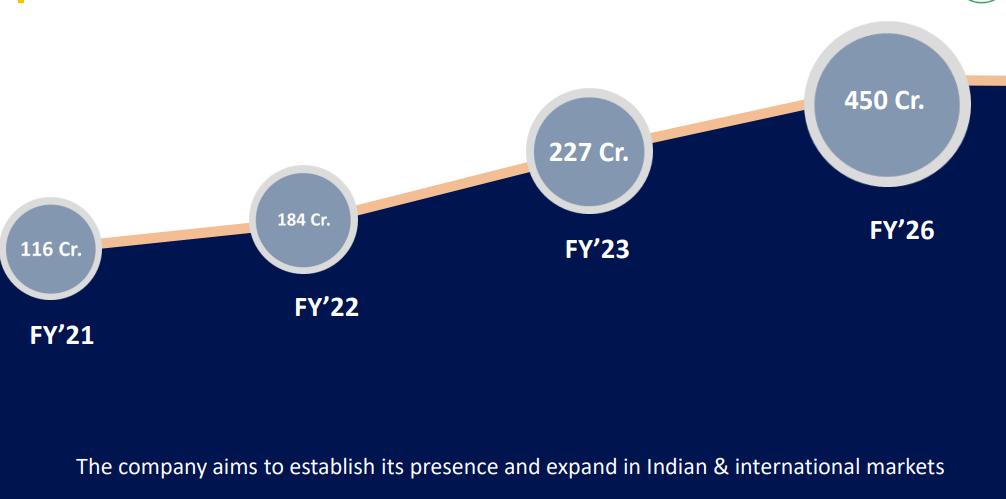

We delivered our highest annual growth ever. The company’s FY22 revenues grew by 58% to Rs 183.84crores while consolidated EBITDA grew by 72% to Rs 43.5 crores from 25.24 crores compared with the year-ago period. EBITDA margins expanded to 23.6% from 21.7. Net profit too increased by 112% to Rs 24.8crores from Rs 11.7 crores compared with the same period a year ago.

-

The company is poised for strong growth for the next few years on the back of its strong R&D efforts to develop complex generics in the oncology space and continued expansion into new geographies. Beta is focused on getting plant approvals and has many inspections/ audits lined up for this year. It is continuing to file new product registrations across the ROW countries and is poised to enter regulated markets soon.

-

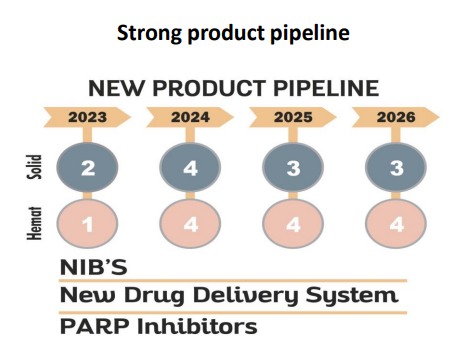

Beta Drugs’ strong product pipeline of twenty-three products which are going off-patent in next five years includes NIBs, NDDS & PARP inhibitors which will continue to support top line and margin expansion.

-

The company is also expanding its API capabilities by developing new products. It plans to file CEP by Oct 2022. This backward integration helps the company to continuously expand its margins. The company has further got an allotment of 12 acres of land on 95years lease in a special area allocated for API & intermediates, where there is a single-window. This will help the company to take care of its future API capacity expansion

-

Beta has also entered into long term partnerships with three multinational pharma companies for its CMO business.

-

We believe that all our segments are slated to clock healthy growth with EBITDA margins in the range of 24% to 25%.

-

The company is in the midst of developing new drug delivery systems, new dosage formulations and applying the latest technology for better processes.

12 Likes

#BETA DRUGS

ANNUAL REPORT FY21-22

MY TWO CENT

Second wave of COVID 19 impacted lives ,bussiness across the board.

We have also started to see inflation across economic in the world, interest rate increase and with ukrarian war conflict,supply chain constraints.

Even th world experienced chaos and disruption, we delivered our highest growth .

FY22 revenues grew by 58% to 183.84 crores while consolidated EBITDA grew by 72% to Rs 43.5 crore from 25.24 compared with the year ago period. EBITDA margins expanded to 23.6 % from 21.7%

Net profit too increased by 112% to Rs 24.8crores from Rs 11.7 crores compared with the same period a year ago.

Beta Drugs’ commands a strong position in the Indian market with more than 112 SKUs and its products are available across all major Corporate & Govt hospitals. The company continues to onboard new hospitals every month and is focused on expanding its branded product portfolio in the existing hospitals too. The company aims to become one of the top ten branded generic players in the oncology market in the near future.

The company is poised for strong growth for the next few years on the back of its strong R&D efforts to develop complex generics in the oncology space and continued expansion into new geographies.

Beta is focused on getting plant approvals and has many inspection/audits lined up for this year. It is continuing to file new product registrations across the ROW ( rest of world)countries and is poised to enter regulated markets soon.

Beta Drugs’ strong product pipeline of twenty-three products which are going off-patent in next five years includes NIBs, NDDS & PARP inhibitors. ( Chemotherapy) which will continue to support top line and margin expansion.

The company is also expanding its API capabilities by developing new products. It plans to file CEP( certificate of suitability) by Oct 2022. This backward integration helps the company to continuously expand its margins. The company has further got an allotment of 12 acres of land on 95years lease in a special area allocated for API & intermediates, where there is a single-window. This will help the company to take care of its future API capacity expansion.

The company is consolidating its institutional business and is continuously adding new logos every year. Beta has also entered into long term partnerships with three multinational pharma( very good sign) companies for its CMO business.

We believe that all our segments are slated to clock healthy growth with EBITDA margins in the range of 24% to 25%.

On behalf of the Board and management, I would like to thank our shareholders, customers

Subsidiary

#Beta UBK international ( Uzbekistan) 60 % shareholding

2.adley formulation 100% shareholding.

3. Adley lab 100% shareholding

Performance

Beta Uzbekistan

Engaged primarily in mfg oncology product approval were obtained on the lat quarter FY22 SALES couldn’t happen in 21-22 ( probably turn around story)

Adley formulation is primarily engaged in manufacturing & trading of oncology product turnover rs 5115 laks with profit rs 501 lakhs

Adley lab in mfg in oncology API ( very few companies had own api) turnover rs 3400 lakh with profitability rs 555.45 lakh

30 % salary hike ( imo negative)

Csr activities is done

Cashflows from operating activity almost double YOY ,( VERY GOOD SIGN) galle me bhi paisa a raha hai…

Disc

top 5 holding

Not sebi register.

3 Likes

I am planning to attend their AGM on Sep 29 at Baddi. Please let me know if the forum members have any questions for the management and I will try to ask them.

Also, if any fellow members are also attending, please DM me and we can collaborate.

5 Likes

@manpritaurora

With only 2- 3 people in R&D, how are they having somany number 1 one brands and also able to make NDS like oral azacitidine and difficult to make products like albumin bound paclitaxel ? Doesnt add up.

But on the other hand, doing CRO for other oncology companies like Intaas, shilpa, Natco etc do give some comfort regarding their capablities and stated numbers.

Would be helpful if you can summarize any new insights gained post AGM.

5 Likes

why they are coming in dermatology segment , which drug they are try to launching , why they not more focused in oncology space, thanks in advance

When are they planning to migrate from SME to main board? Thanks.

Thanks Manprit. Few questions from my side.

- Are they seeing competition from Sakar Healthcare?

- What will drive growth - domestic formulations, export - formulations, b2b API - domestic,b2b API - exports?

- What’s the current utilization?

Notes from the AGM:

Strategy

- Will remain focused on oncology API and formulations

- Cost leadership through backward integration

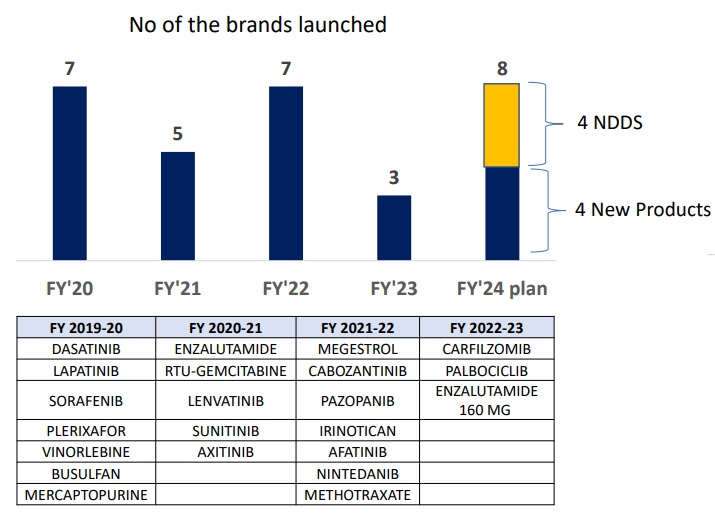

- Pipeline of 25 new molecules to be developed over next 5 years.

- Lung/Breast cancer and Haematology will be focus areas as these cancers affect the largest number of people

- Focus will be on molecules where they can do backward integration

Regulatory approval

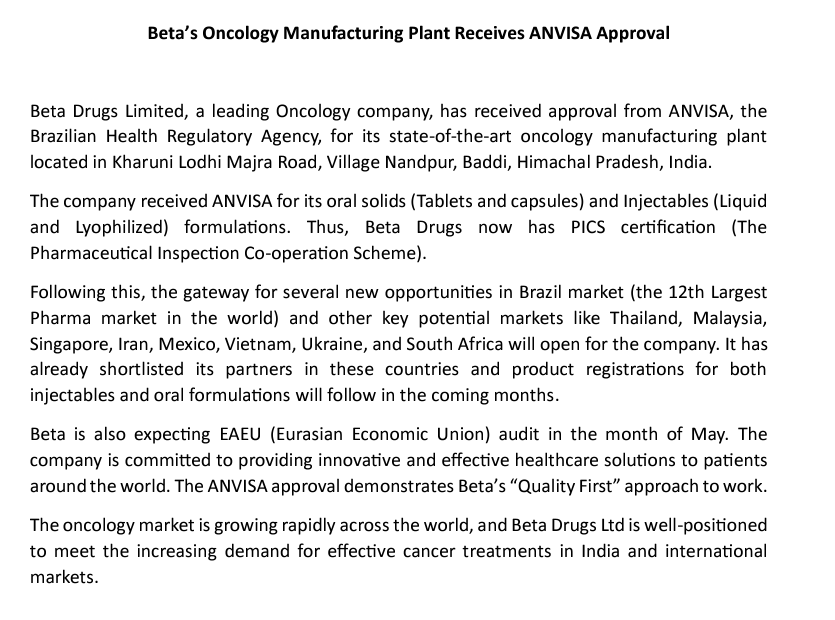

- Some of the major achievements this year, as per management, were the regulatory approval from Columbia and the DCGI approval for their product. Expecting an approval from Mexico soon.

- Targeting EUGMP approval by Q2 2023.

Growth levers

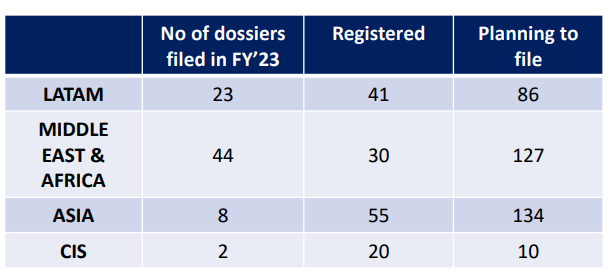

- Export markets, especially LatAm, for formulations. This will be done through partners that have been identified. The Columbia approval has opened the way for LatAm markets.

- Launch 4-5 new products every year and offer a complete Onco basket

- Looking at API exports trying to replicate Shilpa’s model. They will start filing CEPs once their new API plant is ready.

Entry into Derma segment

- The selling channel and strategy in derma has similarities and they want to use that to their advantage.

- Derma and cosmetology are high margin products. They pointed to the recent Curatio acquisition by Torrent at ~9x sales.

- Currently, they are buying from 3rd parties and selling under their brand.

- If the business does well, they will look at making it themselves

Competition from Sakar

- Sakar is buying APIs from them. They don’t see any competition.

Uzbekistan

- The Uzbekistan partnership is not going as planned. They are looking at restructuring the partnership.

R&D

- Have 5 scientists

- Innovator molecules are given to them and these are then developed by them over an average 6-8 months.

Plant visit

- I visited the Quality control and Microbiology block. I could not visit the OSD section as I had to return.

- From my limted knowledge, the QC block looked modern and CFR21 compliant i.e. no manual data entry along with digitization and security controls

Other notes

- No plans to migrate to NSE main board anytime soon

- Hiring talent in Baddi is not a problem as Baddi is a big pharma cluster and people rotate between companies present there.

35 Likes

Management expects to better its 1H performance in 2H. lt expects revenues for FY23 to be at Rs 230 crores aided by strong momentum across all its four segmenrs; own Brands, Exports, OEMs & Apr. while EBITDA margins are expected to improve further.

Beta’s strong pipeline, enhanced capacity, Apl expansion and entering new export

markets will continue to support growth in the coming years.

Rs230crs implies 25% revenues growth. Assuming same PAT margin same as 1H for full year (actually it should be higher given management expects margins to expand). PAT for full year will Rs32.4crs which implies at current market cap of Rs700crs stock trades at 21.6x P/E for FY23E

7 Likes

Promoter Rahul Batra purchased 2400 shares recently. Although the quantity is small, it seems to indicate that the current price is right.

Disclosure: Invested

3 Likes

Beta consolidated revenues from operations for FY23 jumpe d by 24% to Rs. 227.tL crores from

Rs. 183’84 crores compared with the same period a year ago. This increase was mainly due to

31% growth in Exports and 24% growth in Own Brand sales. While Apl sales to third parties

grew by 65%.EBITDA excluding Derma impact increased by 28% to Rs.55.92 crores from Rs. 43.7 crores

compared with the year-ago period. While EBITDA margin expanded to 25.04% from 23.g%.

lmprovement in EBITDA was on account of higher sales of branded products and exports along

with the positive impact of backward integration. However, considering the impact on Derma,s

business the consolidated EBITA stood at Rs 53.gg crores.

1 Like

Stock trades at 22.6x P/E trailing. Management guiding for doublin revenues in 3 years. While EBITDA margins are expected to improve further to be in the range of 25%-26% (from 23% in FY23).

Company continues to be net cash with 33% RoE

PPT https://archives.nseindia.com/corporate/BETA_08052023215830_Investorpresentation.pdf

1 Like

Hello… I have some questions… hope someone will help me

- What is the moat of this business? Till what I could understand, its moat was its backward integration, thus it was able to offer lower pricing and had less risk of raw material price hikes. But if there is such high market opportunity (upwards of 200cr as indicated when the management guided for doubling revenues in 3y) then why don’t other players eg. Natco perform backward integration? (Natco has 938cr in cash and investments as compared to Beta’s 20cr)

- The company’s model for APIs seems fairly copy-able; what is the moat for that and how is the company able to sustain such high growth in API? What am I missing?

Forgive me if my questions aren’t valid… this is my first post ![]()

3 Likes