They are continuously breaking into new products. They are also making sure that retail investors participate. They have reduced lot size from 400 to 200. On charts it is making Cup and handle pattern as well. Has respected 60EMA always. Their products have good ratings as well.

3 Likes

What is Beta drugs doing different that Natco, Shilpa and all are unable to achieve this growth? Being a small company, Beta would face more challenges than the larger ones. While announcing new product launch on Feb 2nd 2022, the note sent to the exchange contains the following:

:Considering the current growth rate cornpany expects to be among top five players in its covered market and among the top 10 Indianan oncology companies in FY’23’

Internationally, BDL is expanding its wings in non-regulated, and semi regulated markets.

Recently, the company has signed agreements with thirteen countries and shared the

dossiers. These countries will start contributing significantly to growth from 3’dQtr’ of FY’23". These statements are made during earning calls or in annual report. Is company trying to be transparent with investor community or is Beta drugs wooing investors by giving these +ve intermittent messages

Disc: Invested

2 Likes

To me, the first sentence of the note appears to be aspirational goal. The second part of the note (about launching new products and agreement with 13 countries) appears to be a new update, because, I could not find the same in their last annual report, last investor ppt and last investor call transcript.

Could you please copy here if you have found something same which confirms that, what they updated yesterday has already been there on record?

I was referring to this link BETA_02022022153644_NSE.PDF (nseindia.com) What they mentioned here were discussed in the earnings call, looks like they are dot on timelines.

My question was more focused on how are they able to grow at this pace (in a very positive tone, hope you can understand)

Disc: Invested

1 Like

Ratings upgraded to CRISIL BBB/Stable (Upgraded from ‘CRISIL BBB-/Stable’)

More interestingly, they have provided undisclosed price sensitive info on Q3 performance. “In first nine months of current fiscal, group has achieved around Rs.135 crore of sales”

The company has done 88 cr revenue in H1FY22 as per published half yearly results which means they have done 47cr in Q3FY22. Given the growth momentum, it would be fair to expect the company to deliver 185+cr revenue in FY22 which would be a fabulous 60% topline growth YoY. This is much ahead of the management guidance of 30% growth, which also tells us about the management. They confidently promised 30% and should deliver double of that, living up to the under promise and over deliver style of management which people love. And if they can sustain H1 EBITDA margins, we are looking at doubling of PAT in FY22 to around 25 crore and current market cap of 500 odd cr seems fair valuation for a micro cap with rapid growth.

Disc: Invested (first purchase at 60)

9 Likes

Outstanding results by the company, wherein improvement in each and every area. The company is now debt free. More growth in FY 23 due to new products and expansion initiatives. Debtor days also have reduced.

1 Like

Certainly great results, with good cash flows, reduction in debt and reduced debtor days. The guidance of 30% revenue growth with ebitda margin of 25 % (current quarter was 23)seems in line with what they said before. They are eyeing exports sales of 70-75 cr for Fy 25 which will certainly help achieve doubling of turnover in 3 years.

Tomorrows con call will be interesting.

1 Like

Certainly great results, with good cash flows, reduction in debt and reduced debtor days. The guidance of 30% revenue growth with ebitda margin of 25 % (current quarter was 23)seems in line with what they said before. They are eyeing exports sales of 70-75 cr for Fy 25 which will certainly help achieve doubling of turnover in 3 years.

3 Likes

Very impressive ppt. and disclosures in spite of SME listed company. My eyes are particularly drawing attention to their slides of presentation that talks about FY 23 and FY25 growth plans.

Discl: Invested at lower levels.

1 Like

Just started to follow Beta Drugs here.

Thanks for sharing. Yes, and absolutely great to see the results yesterday. Hope these growth continue for the near to mid term and the disclosures to only get better.

Disc: Invested at 53, still holding and has become my largest position now.

3 Likes

Anyone attended the concall yesterday can share some pointers here. This would help as no script is uploaded till now.

Thanks in advance!

1 Like

Beta drugs investor presentation

BETA_27042022193008_Investorpresentation.pdf (2.7 MB)

Important points

-BDL has got an allotment of 14 Acres of land on 95

years lease in a special area allocated for API &

intermediates, where there is a single-window

approval from the pollution department.

The company has a plan to expand its API business

along with new formulations in the coming years

-Capacity expansion:

• Lypholizer capacity increased to 3 folds in Beta drugs plant

• Separate lypholized injectable manufacturing facility for general injectable in Adley formulations plant

(Cardiovascular, Antifungal, immunosuppressant)

Disc…invested

5 Likes

4 Likes

I found this Twitter thread on new products R&D going on at Beta Drugs. It says company has potential to become very big. I checked thier website to verify. These future products are mentioned in About Us page. Also there is a brief mention in page 4 of the investor presentation. If anyone has more information on this from company, please share.

Results

- FY22 revenues +58% to Rs 184 crores v/s Rs 116 crores in FY21 driven by higher own brand sales, followed by CRAMs and API sales to third parties. Improvement in EBITDA margins due to higher sales of branded products, exports, and cost rationalization.

- Revenue breakup: 40% from Domestic market, 30-35% from exports and rest from CRAM.

- EBITDA margins: 18-19% in CRAMS. 30-31% in own brands. 27-30% in Exports. 24-26% in APIs

Guidance

- Revenues in FY23 to grow 30%. EBITDA margins expected to be 24%-24.5%.

- Should grow at 30% for next 3-4 years. Margins to also increase as presence would increase in domestic markets. Expect EBITDA margins to head towards 26-27%.

Other details

- Bringing FTLs, NDDS, PARP inhibitors, and TKls to drive growth. Expanding API capabilities by developing new products

- Backward intergration ensure high-quality anti-cancer drugs will lead to expand presence and margins.

- Expansion in lypholizer capacity 3x by installing 1 new lypholizer.

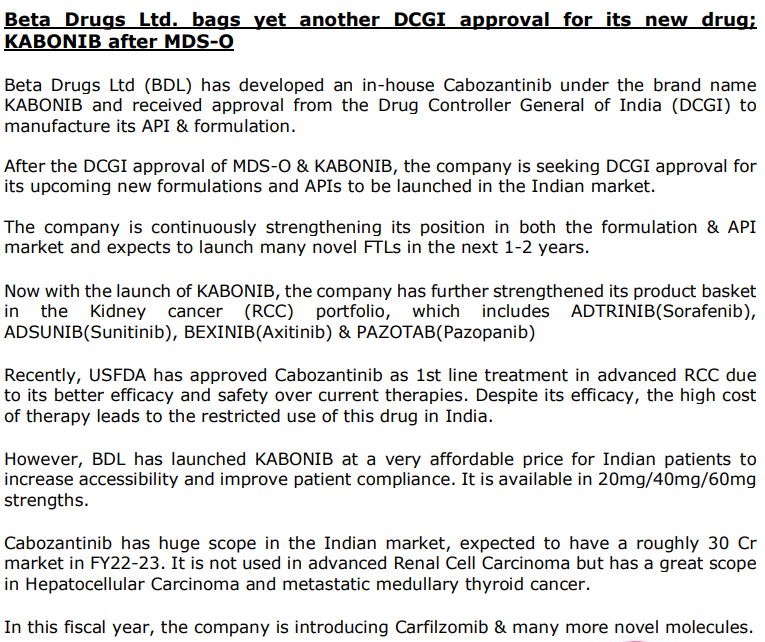

- DCGI approval of Cabozantinib in both API and formulations.

- Achieved WHO accredition last year. Also adding up one more line with 3 reactors and 2 glass lines assemblies. This line will only be for CEP filing and EUGMP approval. Will be commenced by July end.

- Adley formulations plant: One more separate manufacturing unit for general lypholized injectables. Installed 2 new lypholizers and on OEM part and non regulated markets. Plant is almost complete and plan to commence by June end. Will be focusing on Anti fungals and immunosuppresants to start with.

- Launched 15 new molecules in FY22. Stepped towards DCGI Approvals. DCGI approval for azacitidine oral tablets in FY22.

- Clear pre audit from INVIMA (Columbia). Final audit on 15th May. Expecting approval by August. Paid inspection fees for ANVISA (Brazil). First dossier in Thailand and expects an audit soon.

- Launched 30 new APIs from Adley LAB in FY23 and is among very few companies to develop API of Carfilzomib, Cabozantinib, Afatinib, Pazopanib & Rucaparib.

- Expect to add 5-7 customers in CRAM business.

- Current size of Oncology market is ~4750Cr and market share is 3.75%. Intend to have 14-15% market share. Manufacturing for 10 Indian MNCs. 60-70% of their portfolio is manufactured by Beta.

- WC days down to 72 from 90 a year ago, will continue to improve continuosly.

- Will reduce total dependency on China after 3-4 years.

- Have list ready for 35 new molecules operational by FY25.

- Can do 300-350Cr sales from current capacity (FY22 at 184Cr).

- Expect entry into 30-35 private hospitals this year.

6 Likes

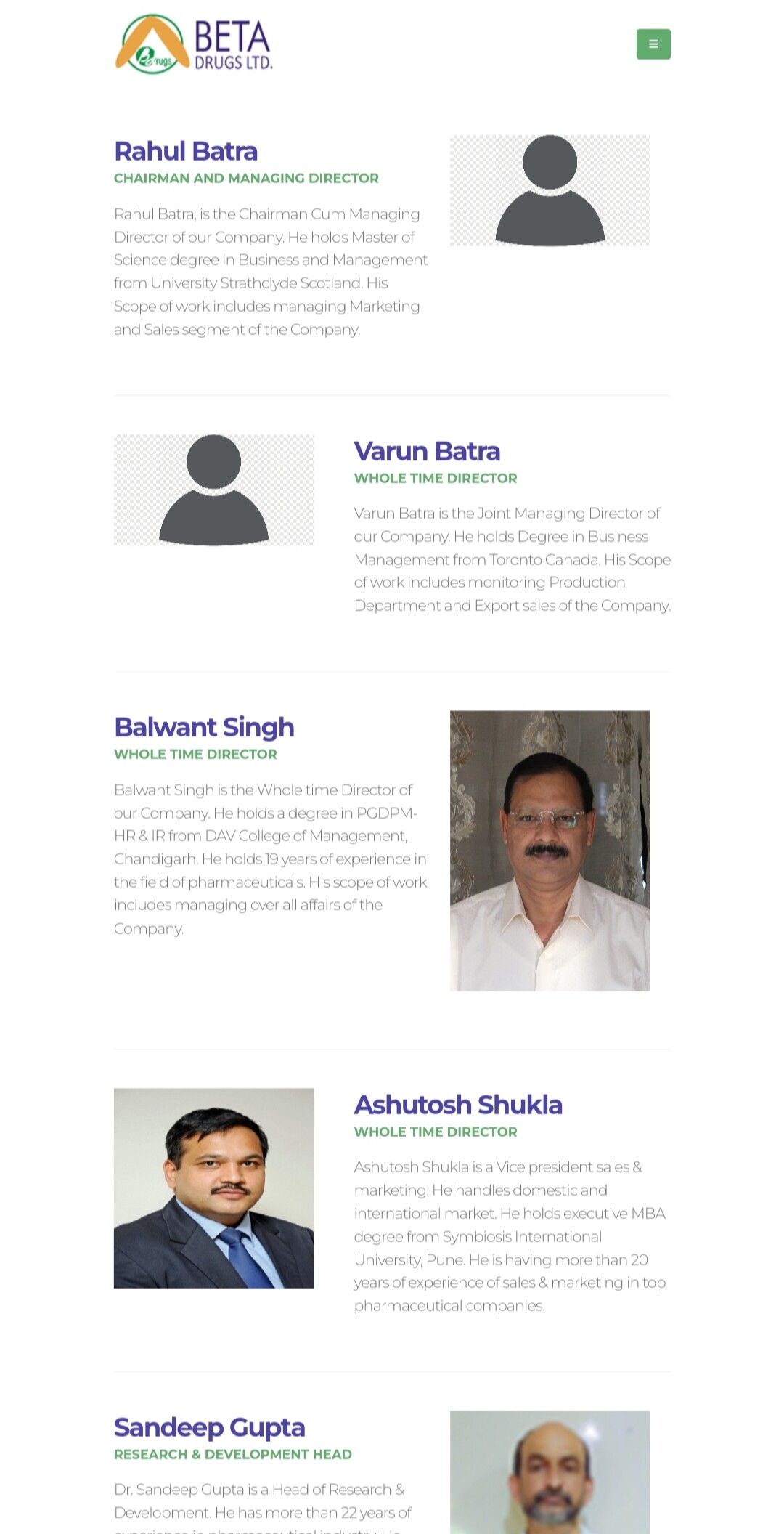

Everything is fine. But why promoters are hesitant to show their face… even company secretary photograph has been uploaded whose salary is 6 lakh (meant to be low key member, don’t take it offensive).

1 Like

BETA_16062022114147_nse.PDF (57.8 KB)

very good going,

disc invested

not sebi register

1 Like

Here are my recent notes on the company:

Overview

- Listed on NSE SME platform. May move to the main board within a year or so; although the company has not yet made application for the move.

- Small debt and net-debt free.

- Capex is complete and sufficient for Rs 300 cr revenue.

- Fast pace of execution. Every 3-4 weeks there is an exchange update about a drug approval or a capex completion and so on.

- Promoter holding is 66.71% in March 2022. Slight increase since June 2020 holding of 66.08%. Vijay Kumar Batra has 65.69% of the shares. He passed away in 2021.

- No FII, DII holding. Ashish Kacholia has more than 5% of the holding. Suryavanshi Commotrade has 8% holding (6.94% from prefential issue in 2019).

- Company has 0.96cr shares. Has not paid any dividend nor issued any bonus shares. Product registrations cost tens of thousands of dollar per product registration; cash preservation is important.

- Website

- Photos of Rahul Batra and Varun Batra are not present on the website even

though photos of others in the management are present.

- Photos of Rahul Batra and Varun Batra are not present on the website even

Subsidiaries & Facilities

- Adley Formulations: WHO-GMP facility for tablets, capsules, Injection & Pre-Filled Syringes in Solan, HP.

- Adley Lab: WHO- GMP, API manufacturing facility in SAS Nagar, Mohali, Punjab.

- Beta Research Private Ltd: Board approved setting up this subsidiary on 4 June 2022.

- Beta UBK International(P) Ltd.: First Indian Oncology plant in Uzbekistan, non-operational as per 2020-21 Annual Report. I did not find any mention of Beta UBK in March 2022 consolidated results. Not sure why it is not operational.

- Beta Drugs: WHO- GMP plant & other international accreditations. Triggered for ANVISA, INVIMA & PICS.

Business

-

Diversified Portfolio in Oncology

-

Working on

- NDDS: 1 NDDS has been launched. Extensively working on NDDS like Liposomes, Nanoparticles, or Micro-particulate systems. As mentioned by @Santosh_pise earlier in the thread, the author of this Twitter thread is quite bullish on NDDS.

- TKIs: TKs are enzymes which promote cell growth and division. In certain tumorous cancers, it would be necessary to control these enzymes to prevent them from helping cancer cells grow. TKIs does the precise function of inhibiting their activity

- Proteasome inhibitors

- PARP inhibitors: PARP (poly adenosine diphosphate-ribose polymerase) is a type of enzyme in human body which repairs damages to DNA in cells. PARP inhibitors stops the enzyme from repairing damage caused to cancer cells by drugs, resulting in their death.

- FTL: Currently adding 4 FTL products. In simple terms, a protein named RAs has been found to be abnormally active in cancer cells. It is found that by inhibiting protein Farnesyltransferase, the abnormality of RAs can be controlled. FTIs does the inhibition work.

We are one of the few Indian companies who have successfully developed & commercialized Nanoparticle –Albumin–Bound Paclitaxel, Ready to use Docetaxel & Gemcitabine.

-

28 April 2022 concall: In CRAMS, we make an EBITDA margin of somewhere around 18% to 19%. In own brands, we make a margin of somewhere around 30%-31%. In exports, we make a margin of 27% to 30%. In API, we make a margin of 24% to 26%.

Raw Materials

-

28 April 2022: 70% of our API sourcing is backwardly integrated. So, if we talk about the top three raw materials which we are manufacturing at Adley Lab facility and supplying to Beta, our Fosaprepitantis one, then Enzalutamide is one, and third one is Methotrexate. So, these three APIs contribute a lot to the volumes.

-

28 April 2022: We used to source around 40%, 50% of our KSMs from China only for our API plant, but now we have reduced that also, and we brought it down to 30%-35%.

Outlook

-

Guidance of 30% revenue growth per year for the next 5 years.

-

EBITDA margin will most certainly increase from the current levels due to

higher contribution from exports. -

We can do a turnover of Rs.300-350 crores from the recently expanded capacity. Taking it forward, we have acquired a land, there we got the approval, not only to make intermediate, we can have as many blocks as we want, we can have a new formulation plant there, we can have a new API plant there, we can have two separate blocks for intermediates.

Verticals: Own Brand

Beta’s own brand has grown 67% as compared to last year.

Domestic

- 28 April 2022: This year, as per IPSOS Data which we got in December, two brands have occupied #1 position in India. There are six brands which have achieved top five positions in the respective markets. Beta has strong positions with 110 different SKUs for all the therapeutics which includes lungs, hematology, liver, breast, etc.

Approvals

-

27 May 2022: Received Drug Controller General of India (DCGI) approval to manufacture API of Rucaparib, a PARP inhibitor. Rucaparib is a targeted therapy for the treatment of Ovarian Cancer and Prostate Cancer. lt significantly improves progression-free survival & has a tolerable safety profile. Rucaparibis less than a year old molecule in Indian market and is expected to have a market size of 30-35 Cr in FY 22-23.

-

28 April 2022: Launched 15 new molecules in last one year. This last year, we got first DCGI approval of Azacitidine Oral Tablet. Just now in April, we have recently got one more approval of Cabozantinib capsules in both API and formulation. Beta has diversified oncology portfolio and with a very strong future pipeline for next five years.

Exports

-

28 April 2022: We have cleared the pre-audit for INVIMA, that is from Colombia and now the final audit is in next 15 days that is on 15th May. We will get our approval by August and simultaneously we will be putting our dossiers for Colombia. We have already filed many dossiers in Latin American countries. We expect the business to start early 2023.

-

28 April 2022: Working on approvals from Brazil, Thailand. By 2023-24 we will achieve our presence in many of the regulated countries.

Capex

-

4 June 2022: Board approved setting up subsidiary named Beta Research Private Ltd.

-

28 Apr 2022: At Beta Drugs, increased the lyophilizer injectable capacity by 3x by installing one new lyophilizer.

-

28 Apr 2022: Already commenced the state-of-the-art Micro and QC laboratory. This will help us in filing EU GMP. We are also adding up one more line with C-reactors and two glass-lined assemblies. This line will only be for CEP filing and EU GMP approvals. The new lines will be commenced and operational by July-end.

-

28 Apr 2022: At Adley formulations, we have installed one more separate manufacturing unit for general lyophilized injectables. We have installed two new lyophilizers and initially we’ll be only focusing on the OEM part and non-regulated markets. This plant is almost complete and plan to commence by June-end.

Verticals: API Business

-

28 April 2022: Received WHOGMP certificate for the facility.

-

28 April 2022: In Adley Labs, launched 30 new APIs last year. Adley Lab is among very few companies who are manufacturing molecules like Carfilzomib, Cabozantinib and many more. Last year, Adley Lab has commenced, its state-of-the-art facility to facilitate our quality precision. This facility is only the micro and the QC lab. We are also adding up one more line with three more reactors and two blast assembly lines, only to cater Europe market and regulated market. The production from this line will start by July end and we have taken a target to file our first CEP for Europe by October end. The products have already been identified. We are going to start filing from October end. We also plan to file many CEPs by the year 2024-25.

Verticals: CRAMS

- Beta has partnership with almost 50 plus companies and we expect to add five to seven more this year. Last year, we added around seven new companies in our portfolio. There is a lot of leverage in terms of production capacity.

- We are manufacturing for 10 Indian MNCs. 60-70% of their portfolio is manufactured by us.

- Rs 21 crore revenue in CRAMS came from exports and Rs 55 crore from domestic business.

Disclosure: Invested from lower levels.

17 Likes

All numbers look good. All Data looks good but when you go to their website, one glaring thing is where are all the scientist and researchers

1 Like