Bengal and Assam (B&A) is the holding company of JK group (JK Lakshmi cement and JK

Tyres). The key share holders of B&A are Mr. Hari Shankar Singhania (31.04%

stake) and Dr Raghupati Singhania (10.63% stake) and promoter owns 73.96%

stake.

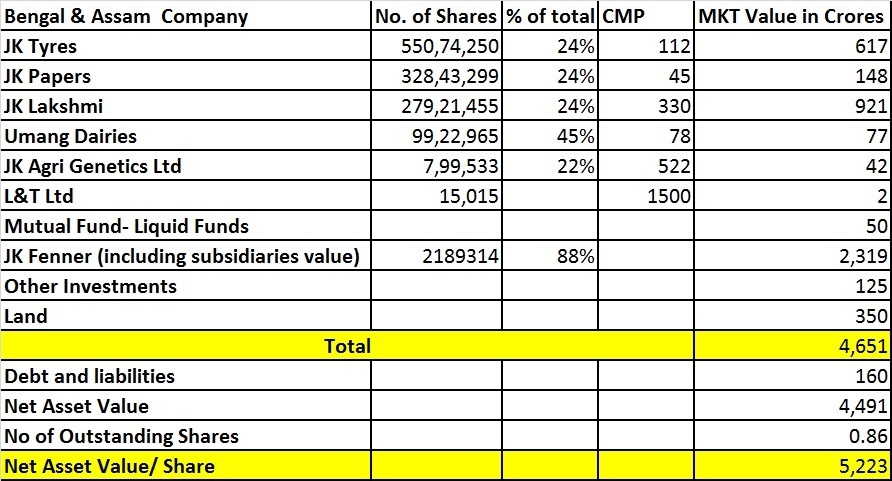

B&A is the biggest promoter share holder of JK lakshmi (24% holding), JK tyres (24%

holding), JK Papers (24% holding),Umang diary (45% holding), JK Agri Genetics

(22% holding) and JK Fenner (88% holding). B&A only listed in the Bombay stock

exchange.

Also B&A owns (either directly or through subsidiaries) in JK Lakshmi cements (40%

stake), JK tyres (44% stake) and JK papers (50% stake) and B&A also have

large parcel of real estates in urban areas which worth thousands of million

rupees.

Across the JK group, companies are witnessing big expansions are the JK Tyres (increase in radial tyre business and also leader in domestic radial CV tyres market- Market Cap is Rs 25 bn) and JK Lakshmi cement expansion in eastern and western region. With thecommissioning of new facilities at Durg, Odisha and Gujarat, the company is expected to have a standalone cement capacity of over 10.3 MT by the end of June’16. Considering capacity in place and economic recovery will boost the performance of the company, going forward. JK Lakshmi’s market CAP is Rs 38 bn.

Hidden gem company- JK Fenner (Auto ancillary company) is unlisted company in Rubber 2 Wheeler transmission used in scooters in domestic market. JK Fenner has business of ~ Rs 6 bn and has leading EBITDA margins of ~ 22%. In future, company has plans to enter in to the Industrial segment, Which is relatively high margin business. The consolidated book value of the JK fenner is Rs 1,740/share as on Mar’15. JK Fenner pays Rs 35/Share as dividend in FY15.

JK Agri Genetics, is a leading hybrid seed company engaged in R&D, production, processing and marketing of vegetables, cotton, Rice,Maize and Pearl Millets among others. Company has 10% Market share in the hybrid Rice. Company aims to double the revenue in next three years.

Umang Dairies is a dairy product of JK organisation. Key brands are White Magik, dairy top and Umang Ghee. In January, 2014, it launched its liquid milk in lucknow under the brand name JK Milk. Over the past 5 quarters, the average sales growth of Umang is over 30% and RoCE is well above 25%.

Considering current valuations of all the subsidiaries and holding company,

the net asset value of Bengal and Assam (B&A) is works out to be Rs 5,223/share.

At the current market price of Rs 540, Bengal &Assam currently trades at

big discount of 90% of its investment value. 52 weeks low/ high is Rs 450/ Rs 650.

Interestingly, consolidated P/E of B&A is just 2 times at current market

price. It is very interesting and unbelievable a holding company is available at

much discount.

Summary and Valuations: