Overview

Belrise Industries Ltd (BIL) incorporated in 1996 by Mr. Shrikant Badve, specializes in Automotive Systems for the Two-wheeler, Three-wheeler and Four-wheeler Passenger and Commercial vehicle niche.

The BIL group manufactures chassis and frame assemblies, sheet metal, exhaust systems (silencers), plastic molded and painted parts and assemblies for auto and consumer durables segments.

Recently, BIL has brought IPO on 21 May 2025. The entire IPO was a fresh issue and raised ₹2150cr. From ₹2150cr, BIL is going to use ₹1618.3cr for prepayment of its existing debt.

Currently BIL has net debt of ₹2964cr. After prepayment it reduces to ₹1345.7cr. Even we assume if BIL takes ₹500cr as new debt for their new ₹800cr capex plan for next 2 years. Still the net debt will stand at ₹1845.7cr.

The issuance of IPO has happened in Q1 of FY26. Therefore, the effect of debt reduction will be seen in the Q2 of FY26 as guided by the management.

Product Profile

BIL has a well diversified auto component portfolio with 1000+ products. BIL also has 18

manufacturing facilities in 10 cities in 9 states. And 30+ OEMs as it’s marquee clients.

In 2W metal components market, BIL has 24% market shares making it one of the top 3 players in that segment.

BIL also has global presence and represents 5.4% of exports. Some key market includes Austria, Slovakia, United Kingdom, Japan and Thailand.

73% of products made by BIL are powertrain-agnostic. Which simply means that, these products can be used both in EV and ICE vehicle without any modifications.

| Segment (As of Q1 FY2026) | Revenue Contribution by % | Revenue Contribution by value( in Cr) | Products |

|---|---|---|---|

| 2W+3W | 82.8% | 15,164 | Steering Column, Shock Absorber, Exhaust System, 2W+3W Chassis, Hub Motors, etc |

| 4W Passenger | 4.5% | 832 | Cross Car Beam, Seating system parts, BIW parts, etc |

| 4W Commercial | 8.8% | 1614 | Chassis, Air tank, Bumper |

| Other | 3.9% | 713 | Other |

Industrial Overlook

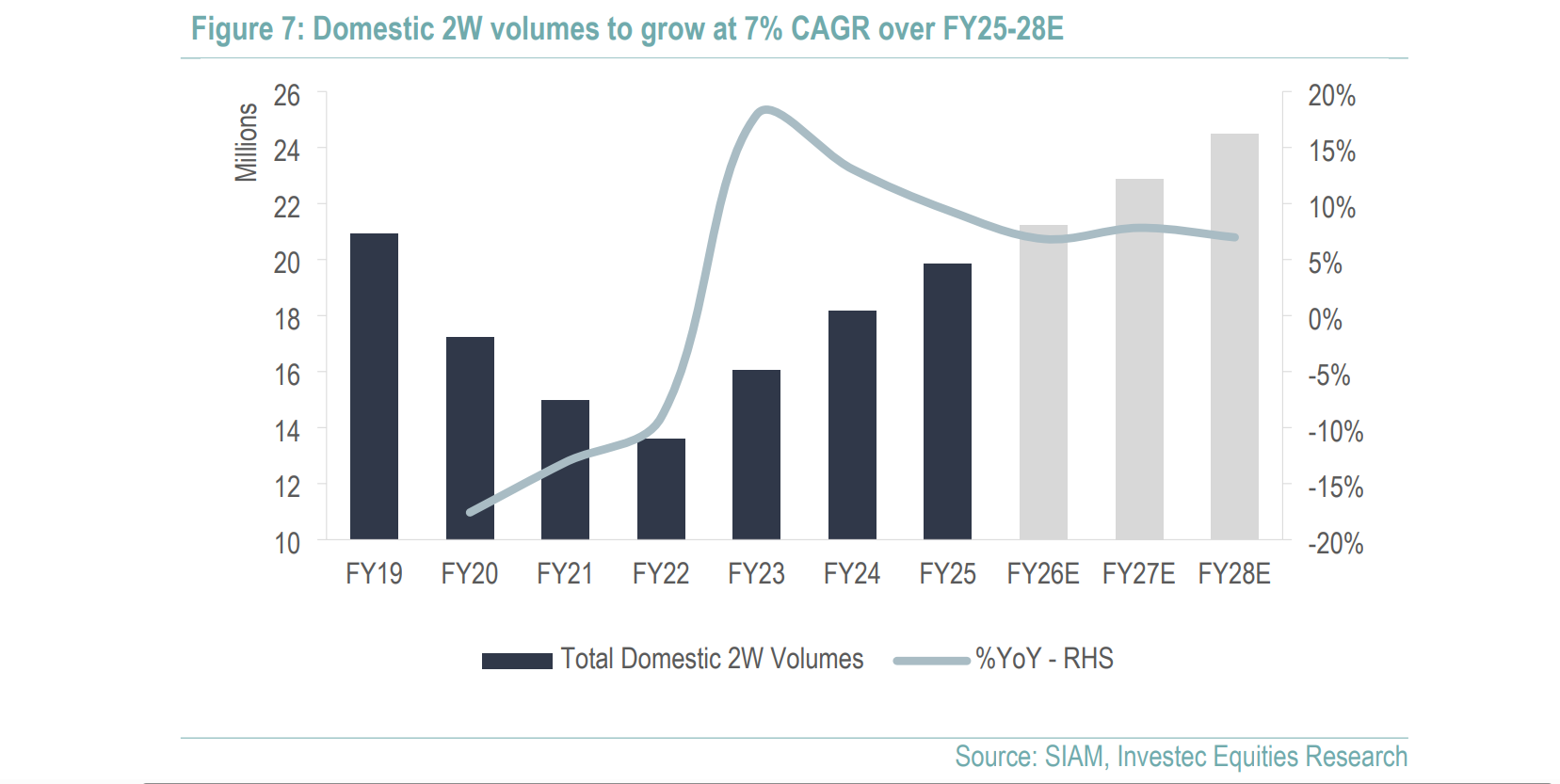

2W Domestic demand has seen a steady growth of 13% CAGR from FY22-25. It is estimated that the 2W domestic industry can grow at 7% CAGR for the next FY25-28E.

2W Export has seen double digit growth in longer time frame. Thanks to Indian 2W OEMs like Bajaj auto, Hero moto, Tvs motors etc, gaining market share from Chinese OEMs in markets like Africa, South Americas, etc. Belrise is a key component supplier for 2W Indian OEMs, especially Bajaj auto. It is estimated that 2W exports to grow at 12% CAGR over FY25-28E led by recovery in African markets and strong volume offtake in newer geographies like South Americas.

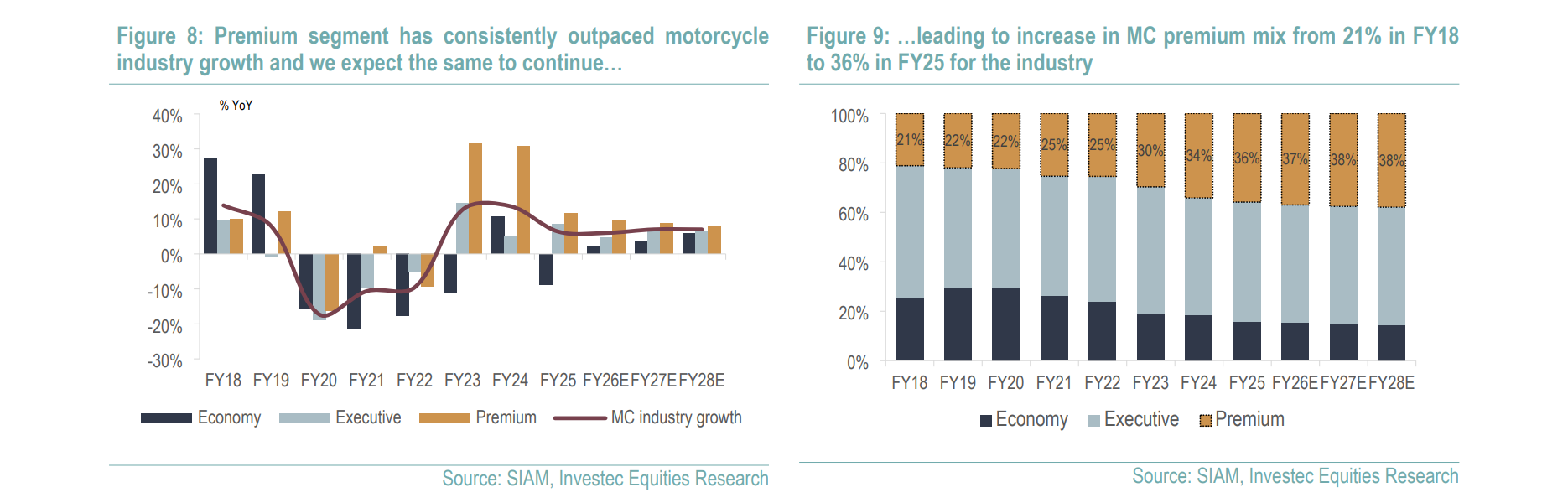

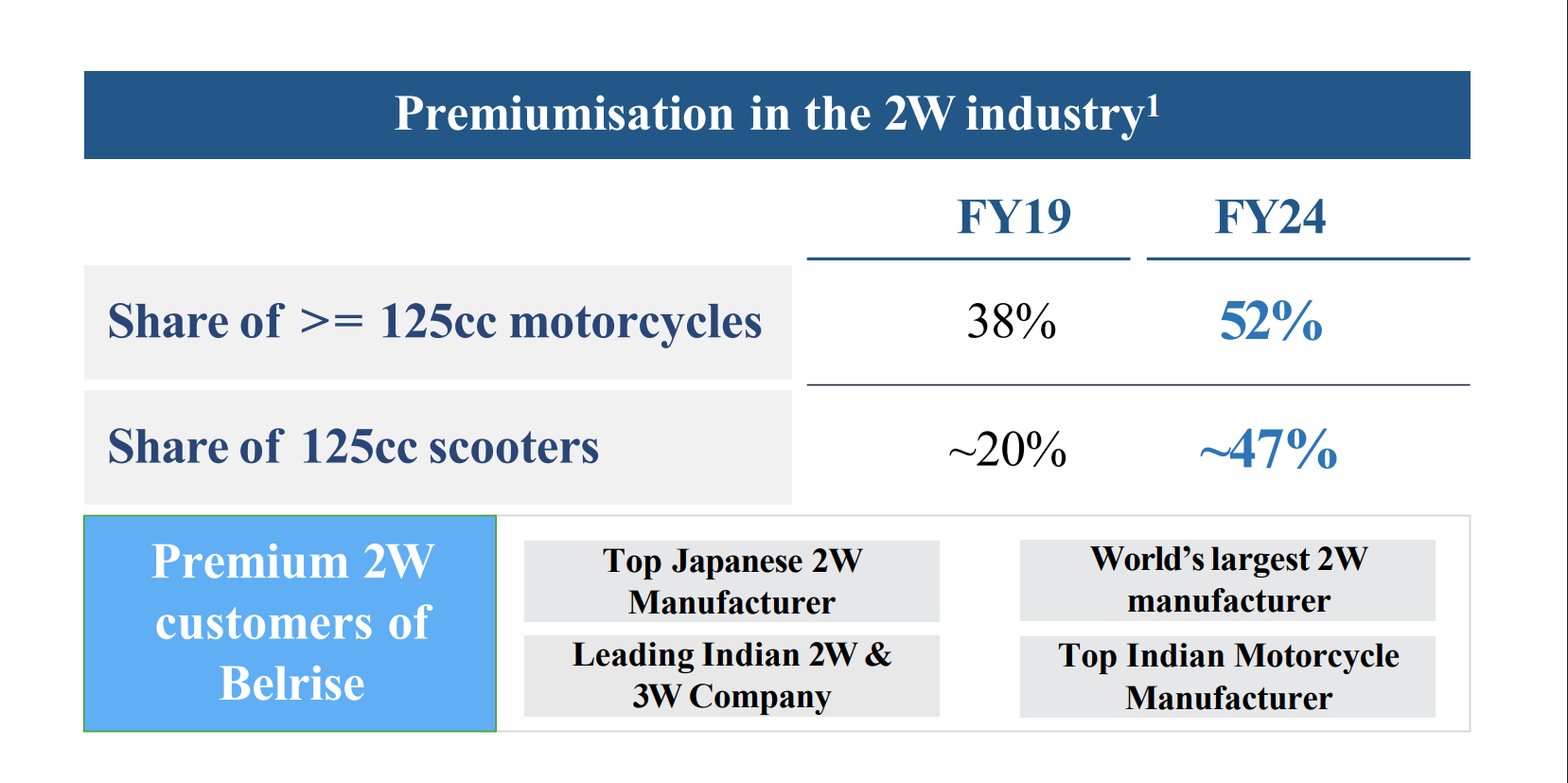

Premiumization is a tailwind for auto ancillaries as there is a steady rise in demand for higher-end variants. Similarly, in scooters, the demand for 125cc+ has increased substantially. The premium auto component were 22% of a motorbike. In FY25, that has substantially increased to 36%. It is estimated that till FY28E, most motorbike will contain 38% of premium components.

GST Rate Cut could give boost to consumption theme. Government has reduced GST rate on 2W of 350cc from 28% to 18%. Therefore increasing domestic demand. The scope of rate cut might be limited as high end 2W above 350cc are still charged at 28% GST.

RBI Rate Cut has also boosted domestic demand. After interest rate cut from 6.5% to 5.5% and further rate cut on the horizon. Vehicle financing could become cheaper.

Growth Drivers

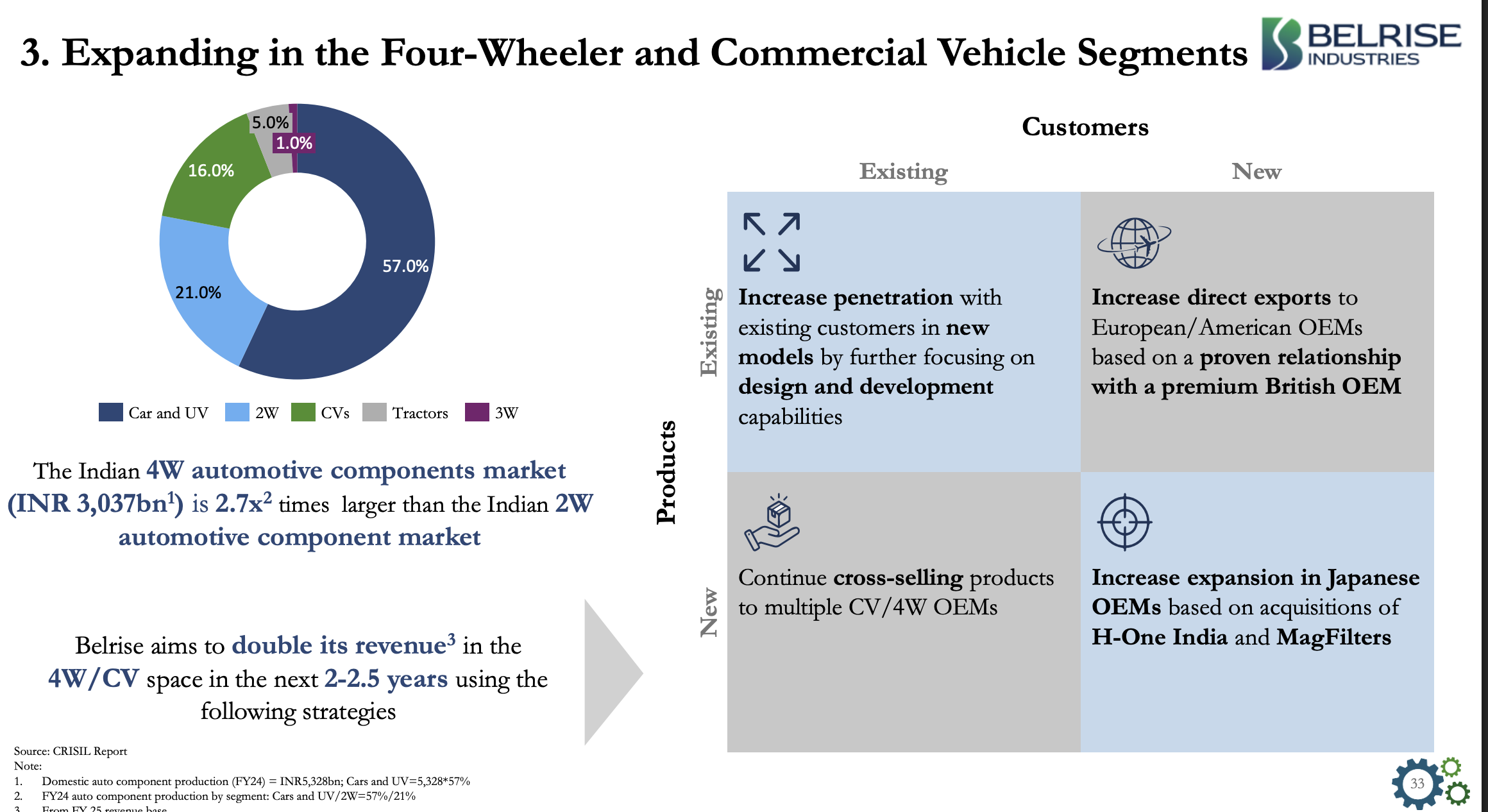

Acquisitions of two companies H-One India and MagFilters gives BIL access to proprietary technology, thereby imporving there product mix as well as margins.

-

H-One Indian gives BIL access to high-tensile steel manufacturing up to 1,100 MPa

as compared to industry average of 600 MPa. Therefore, reducing thickness of steel while almost doubling the tensile strength. -

H-One gives access of manufacturing plant which is already running at 40% capacity utilization. With complete R&D set-up. Will bring 1 new Japanese 4W OEM and 2 new Japanese 2W OEMs.

-

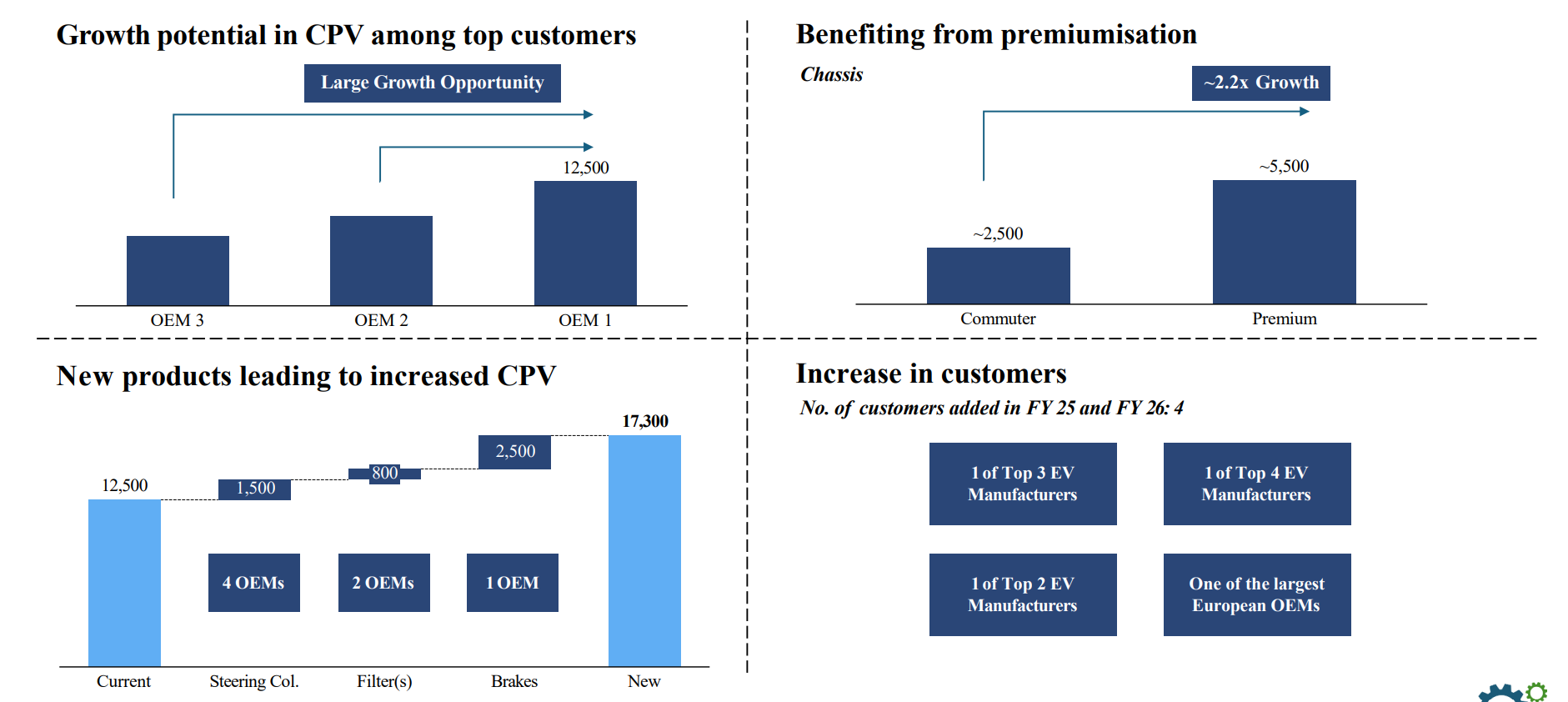

H-One’s new manufacturing plant at 40% can generate 250-300cr of sales. In 4W segment, management is guiding of Content Per Vehicle (CPV) will increase by 60% to ₹15000.

-

Whereas, MagFilters will give design of proprietary filtration systems and plastic moulding components, with R&D set-up in-house. Will again bring 1 new Japanese 4W OEM and 2 new Japanese 2W OEMs. And Content Per Vehicle will increase by ₹1000 for 4W.

Capex of 800cr is planned for next 2 years with 2 tranches of 400cr. A portion of the said capex will be toward H-One India’s capacity expansion. BIL is planning to fund this capex through internal accrual. They have already generated CFO of 704cr in FY25. Average 4year CFO is 638cr.

Premiumization in 2W and 4W has been a sticky trend. One of the main product is chassis for 2W. The content per vehicle for lower end 2W is ₹2500 whereas for high end 2W it is ₹5500. With new products from acquisition and new proprietary product from their own R&D, BIL is guiding for ₹17300 CPV which currently at ₹12500.

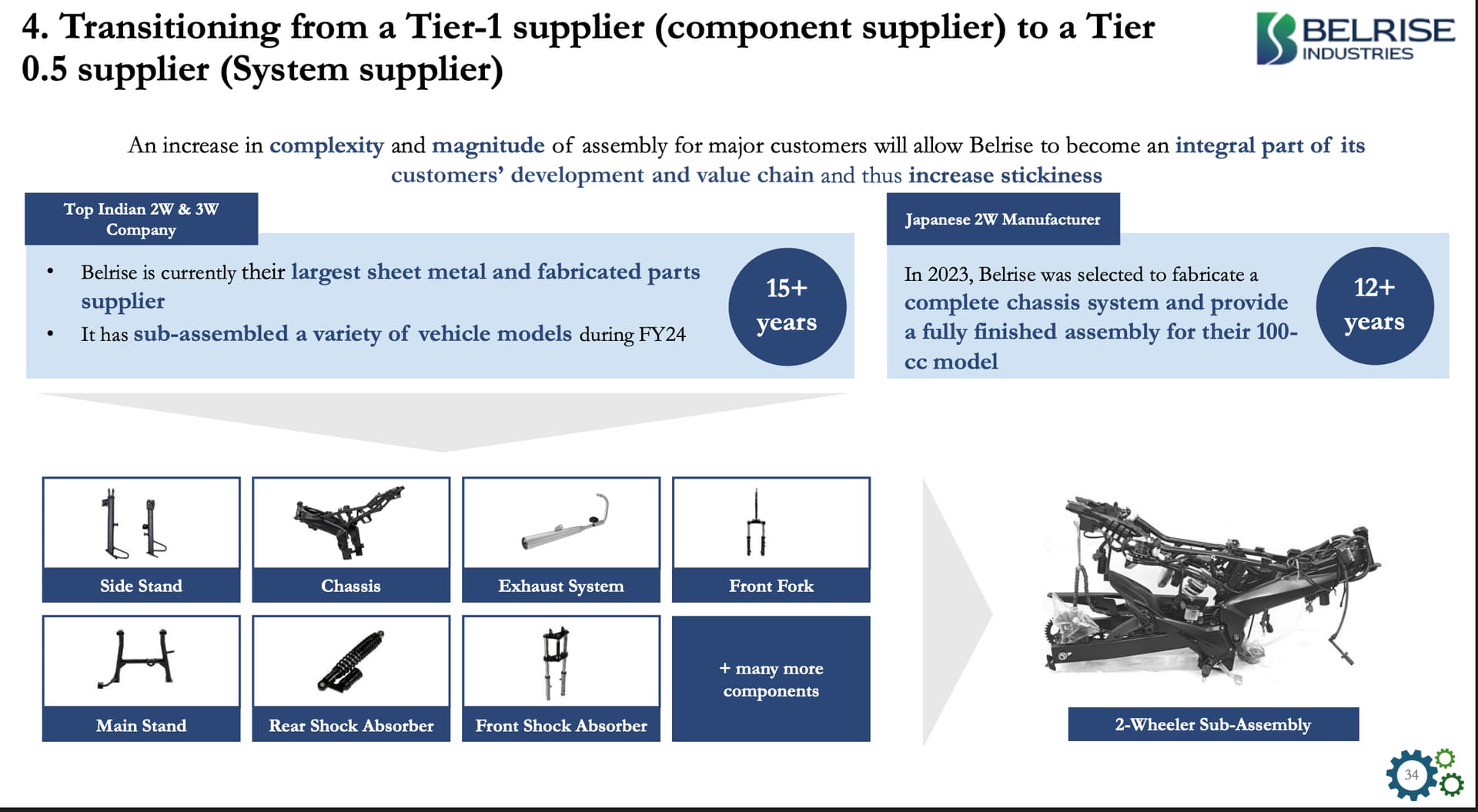

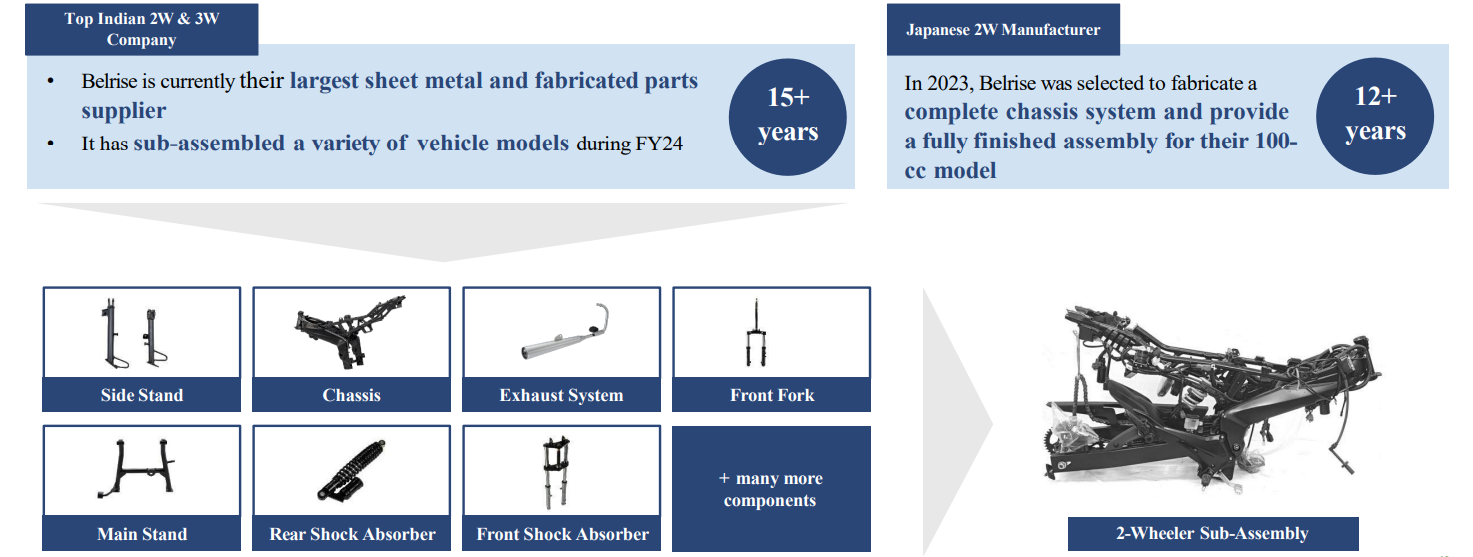

From Tier-1 supplier (component supplier) to a Tier 0.5 supplier (System supplier). BIL is moving up the value chain by taking multiple auto components and assembling them to create a complex system. A pre-assembled system for OEMs.

Clients

Financial Highlight

| As of Q1 FY2026 | Q1 FY26 | FY25 | FY24 | FY23 | FY22 |

|---|---|---|---|---|---|

| Revenue | 2262 | 8291 | 7484 | 6583 | 5397 |

| PAT | 112 | 355 | 314 | 314 | 262 |

| NPM % | 4.9 | 4.3 | 4.2 | 4.8 | 4.8 |

| Debt/Equity | - | 1.1 | 1.1 | 1.1 | 1.5 |

| ROE % | 14.1 | 13.2 | 13.4 | 15.3 | 15.1 |

| CFO | - | 704 | 582 | 789 | 474 |

| CFO/PAT % | - | 198.2 | 185.6 | 251.7 | 181.2 |

After prepayment of debt of 1618.3cr. Current debt of 2964cr will reduce to 1345.7cr @ 9.5% according to management. Therefore debt/equity could reduce to 0.49.

Or if we assume BIL takes new debt of 500cr for their new capex, then the debt/equity will be 0.68.

In both cases BIL will see a big jump in PAT, due reduction interest cost.

Strength

-

BIL is a well established player in Auto Ancillary market. With longstanding relationship with major Indian and Japanese OEMs, especially with Bajaj Auto. And also adding new Japanese OEMs as their customers.

-

With 1000+ product mix. BIL has a well diversified product portfolio and 73% of products are powertrain-agnostic. Therefore, are future ready for EV adoption.

-

Increasing focus on R&D and moving toward more in-house developed proprietary product.

-

BIL has geographically diverse capacities and presence. The group has 18 manufacturing facilities across 10 cities in India, which enables it to cater to geographically diverse customers.

-

With recent IPO the debt will be reduce significantly. Thereby improving balance sheet health.

-

BIL has average CFO to PAT% at 160+ for last 4 years. Has enough CFO to fund capex from internal accrual without taking any major debt.

Weakness

-

BIL exists in a cyclical sector. Any downward trend in Auto sector can affect BIL’s revenue adversely.

-

Top 10 OEMs clients contribute 50-60% of the revenue, leading to client concentration risk.

-

If BIL’s new acquisition or capex plan fail in the future. It could adversely affect PAT due to elevated depreciation.

Disc - Have small tracking position, biased, not a SEBI registered, not a buy/sell recommendation, posted only for educational purposes.